SMM7 March 17:

The epidemic that occurred at the beginning of this year has had a great impact on the global economy and industrial development. For the cobalt lithium new energy industry, the market supply and demand structure has also undergone significant changes. However, since March, China and Europe have issued optimistic policies for the new energy vehicle industry, which undoubtedly releases a positive signal for the future development of "electrification". In this way, the SMM new energy analysis team investigates and integrates the production data of China's core battery materials, summarizes the trend characteristics combined with the price trend, and makes a judgment and forecast of the price trend in the second half of 2020.

This is the first of a series of analysis reports, which describes the core data conclusions and forecasts of the cobalt industry.

From January to June 2020, China's total output of cobalt sulfate was 16900 tons of metal tons, down 24% from the same period last year. SMM expects production of 21800 tons of cobalt sulfate in the second half of 2020, down 11.7% from the same period last year.

From January to June 2020, China's total output of cobalt chloride was 17000 tons of metal tons, up 12.3% from the same period last year. Dome SMM expects the output of cobalt chloride in the second half of 2020 to be 22600 tons of metal tons, an increase of 12.3% year on year.

From January to June 2020, China's total output of cobalt tetroxide was 28800 tons, an increase of 11.7 percent over the same period last year. Dome SMM expects to produce 32500 tons of cobalt tetroxide in the second half of 2020, an increase of 8.9 percent over the same period last year.

From January to June 2020, the total output of ternary precursors in China was 114000 tons, a decrease of 24% compared with the same period last year. SMM expects the output of ternary precursors in the second half of 2020 to be 135000 tons, down 3.4 per cent from the same period last year.

In the first half of 2020, the average price of SMM metal cobalt was 258400 yuan / ton, down 9.5% from the same period last year; the average price of cobalt sulfate was 49000 yuan / ton, down 9.7%; the average price of cobalt chloride was 59000 yuan / ton, down 6% from the same period last year; and the average price of cobalt tetroxide was 187000 yuan / ton, down 7.2% from the same period last year. SMM expects that the price gap between cobalt and cobalt salts will narrow in the third quarter, the terminal demand for batteries will gradually recover in the third quarter, and cobalt salt prices may rebound, but overseas epidemic control is not optimistic and the expected increase is limited. The possibility that the outbreak in Africa will affect the supply of cobalt raw materials and the price of cobalt may fluctuate sharply.

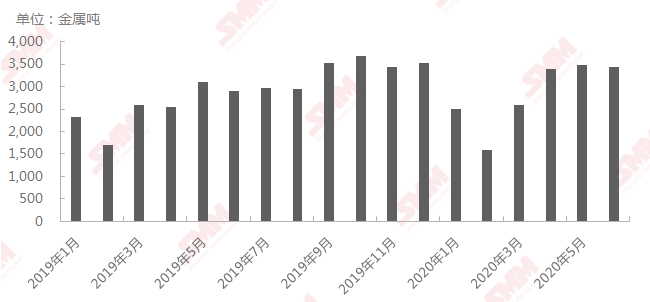

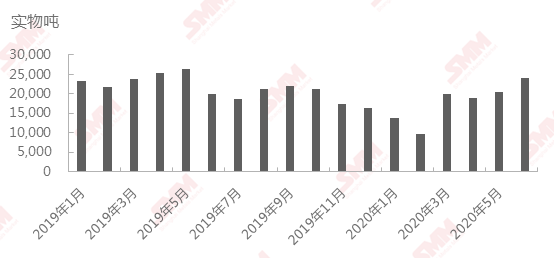

Output of Cobalt Sulfate in China from January 2019 to June 2020

Source: SMM

From January to June 2020, China's total output of cobalt sulfate was 16900 tons of metal tons, down 24% from the same period last year. The decline in cobalt sulfate production is mainly due to the impact of the new crown epidemic, the downstream demand for ternary precursors and materials has been greatly reduced, the price of cobalt sulfate is seriously upside down, some manufacturers switch production lines to cobalt chloride, or carry out technical transformation and maintenance, and the supply of cobalt sulfate is reduced. In February 2020, the domestic epidemic broke out, logistics was blocked, workers were reworked and isolated, and the operating rate of cobalt sulfate manufacturers declined seriously. From March to April, the supply of cobalt sulfate manufacturers gradually recovered, but the price was upside down, the downstream demand was reduced, some manufacturers switched production lines to cobalt chloride, and the output of cobalt sulfate was gradually reduced. The epidemic situation in Africa from May to June was serious, which affected the import of cobalt raw materials. The operating rate of some cobalt salt plants was reduced and the output decreased from May to June. In the second half of the year, it is expected that the ternary demand for downstream power will gradually recover, the procurement demand for cobalt sulfate will increase, the scheduling plan for cobalt sulfate will gradually increase, some cobalt sulfate manufacturers will gradually climb the slope, and the supply of cobalt sulfate will increase in the second half of the year. SMM expects cobalt sulfate production to be 21800 tons of metal tons in the second half of 2020, down 11.7% from the same period last year.

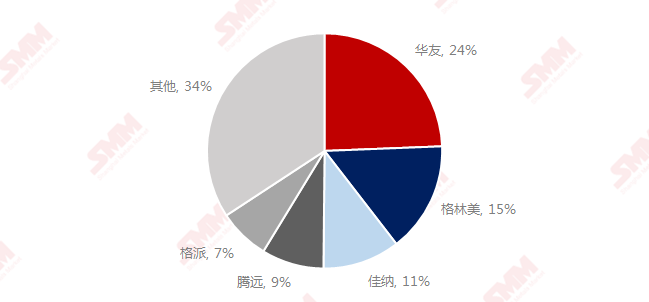

Market share of H1 Chinese Cobalt Sulfate TOP5 producer in 2020

Source: SMM

The market share of H1 Chinese cobalt sulfate TOP5 producers in 2020 is 66%, which is 5% higher than that of H1 TOP5 in 2019. The production of H1 cobalt sulfate TOP5 in 2020 is slightly different from that in 2019, and the market share of Tengyuan and Gepai is higher.

Output of Cobalt Chloride in China from January 2019 to June 2020

Source: SMM

From January to June 2020, China's total output of cobalt chloride was 17000 tons of metal tons, up 12.3% from the same period last year. The output of cobalt chloride increased, and under the influence of the epidemic, the demand of digital 3C was less affected than that of power ternary. The water of cobalt chloride is higher than that of cobalt sulfate, and some cobalt salt plants switch production lines to cobalt chloride, and the output of cobalt chloride increases. A supplier in central China began to produce crystal products from cobalt chloride from May to June, and the supply increased. Two new production lines of suppliers in East China have been put into production one after another, and the output has gradually increased. In the second half of the year, the demand for digital 3C side ushered in the procurement peak, the demand for cobalt chloride further increased, the superimposed new production capacity climbed, and the supply of cobalt chloride may further increase in the second half SMM expects cobalt chloride production to be 22600 tons of metal tons in the second half of 2020, up 12.3% from the same period last year.

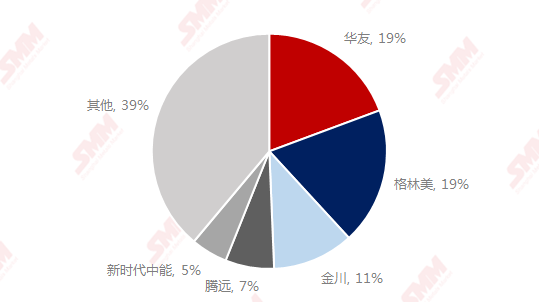

Market share of H1 Chinese Cobalt Chloride TOP5 producer in 2020

Source: SMM

The market share of H1 Chinese cobalt chloride TOP5 producers in 2020 is 61%, which is 22% lower than that of H1 TOP5 in 2019. The manufacturer of H1 cobalt chloride TOP5 in 2020 is slightly different from that in 2019, and the market share of Green Mei and Zhongneng in the new era is higher.

Output of cobalt tetroxide in China from January 2019 to June 2020

Source: SMM

From January to June 2020, China's total output of cobalt tetroxide was 28800 tons, an increase of 11.7 percent over the same period last year. The output of cobalt tetroxide increased, and under the influence of the epidemic, the demand of digital 3C was less affected than that of power ternary. The supply of cobalt tetroxide was only affected by the domestic epidemic in February, the rework of some factory workers was isolated, the output decreased, most of the factories did not stop work during the Spring Festival, and the output was less affected by the epidemic. Since March, the demand for cobalt tetroxide has accumulated, the demand for cobalt tetroxide has increased, and the supply has increased at the same time. From May to June, the epidemic in Africa is serious, which affects the import of cobalt raw materials, the inventory of cobalt raw materials is tight, and cobalt tetro In the second half of the year, the demand for digital 3C terminal ushered in a procurement peak, the demand for cobalt tetroxide further increased, and the supply will increase at the same time. SMM expects cobalt tetroxide production of 32500 tons in the second half of 2020, up 8.9% from the same period

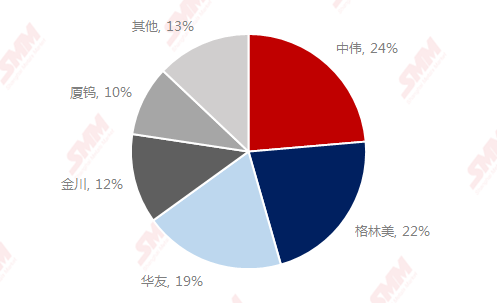

Market share of H1 Cobalt tetroxide TOP5 manufacturer in China in 2020

Source: SMM

The market share of H1 Chinese cobalt tetroxide TOP5 manufacturers in 2020 is 87%, which is 6% higher than that of H1 TOP5 in 2019. The manufacturer of H1 cobalt tetroxide TOP5 in 2020 has a slight change compared with H1 in 2019, and the market share of Zhongwei and Greenmei has increased.

Output of ternary precursors in China from January 2019 to June 2020

Source: SMM

From January to June 2019, China's total output of ternary precursors was 114000 tons, down 24 per cent from the same period last year and 8.8 per cent lower than in the second half of 2019. In 2020, the output of ternary precursors in China was average, with a monthly output of more than 20,000 tons in only three months. The domestic epidemic broke out from January to February, and most of the precursor enterprises were in Zhejiang, Guangdong and other areas with serious epidemic situation, and the situation of resuming work and production was poor. In March, the operating rate of precursor enterprises increased significantly, the output also increased, and the volume of overseas exports also increased significantly compared with the previous month. Affected by the overseas epidemic situation in the second quarter, the export of ternary precursors decreased, the demand of domestic small power market increased, the power market gradually warmed up, and the monthly output of ternary precursors exceeded 20,000 tons. In the first half of the year, there were five enterprises with an output of more than 5000, with a CR10 of 75.3%. CR5 is 58.4%. SMM expects China's production of ternary precursors in the second half of the year to be 135000 tons, up 15.3% from a year earlier.

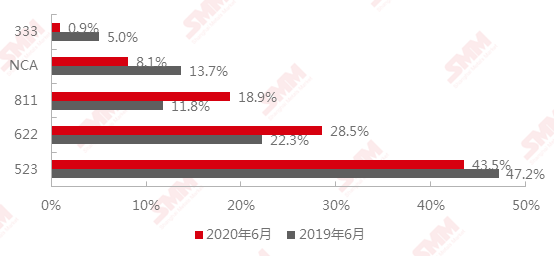

Comparison of product structure of ternary precursors in China in 2020 and June 2019

Source: SMM

In terms of production structure, the progress of high nickel production is stronger than that of the same period last year, but in the first half of this year, affected by the epidemic, the downstream is mainly cost reduction, the mainstream of the market is still dominated by 5muri 6 series, and the total proportion of 5muri 6 series is still as high as 72%. SMM expects that the ternary demand for high nickel will gradually recover in the second half of the year, and the 5-series will still account for a high share of the small power and power market. This year, some new models will be equipped with 6-series ternary batteries, and the proportion of 6-series may increase slightly.

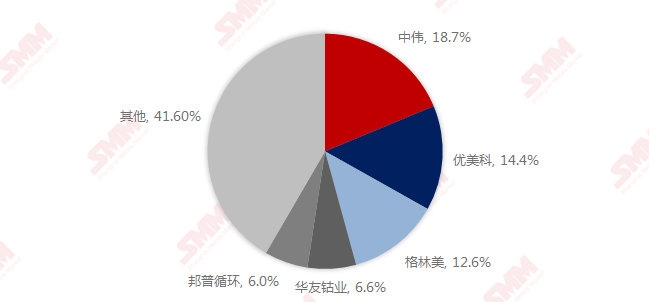

Market share of H1 ternary precursor TOP5 manufacturers in China in 2020

Source: SMM

Precursor Top 5 accounts for 58.4%, and the degree of industrial concentration remains basically unchanged. In 2020, large factories still have plans to expand production, such as Grimme to expand production of 50, 000 tons of ternary precursor materials, Huayou Group's Huajin New Energy to continue to expand production to 100000 tons, Jintong Reserve capacity to expand to 50, 000 tons by the end of the year, and Zhongwei to expand production to 23000 tons, and so on. At present, small and medium-sized factories compete for digital and small power market orders, although the small power market demand is strong, but the precursor enterprises have overcapacity, the electric two-wheeler market has low requirements for the quality of ternary batteries, the market competition is fierce, and the price continues to be under pressure.

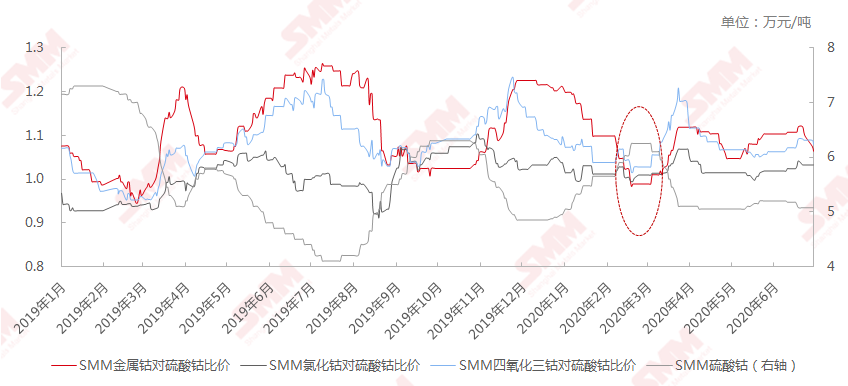

Price comparison of Chinese Cobalt products to Cobalt Sulfate in January 2019

Source: SMM

In the first half of 2020, the average price of SMM metal cobalt was 258400 yuan / ton, down 9.5% from the same period last year; the average price of cobalt sulfate was 49000 yuan / ton, down 9.7%; the average price of cobalt chloride was 59000 yuan / ton, down 6% from the same period last year; and the average price of cobalt tetroxide was 187000 yuan / ton, down 7.2% from the same period last year.

As the price of cobalt sulfate directly represents the pulse of cobalt's most eye-catching terminal consumption of new energy, SMM selects it as the core price comparison factor to compare the price of cobalt smelting products on behalf of other traditional consumers to measure and compare the pricing factors in different periods of time in the process of cobalt price fluctuations. Generally speaking, the specific price of metal cobalt and cobalt tetroxide to cobalt sulfate fluctuates between 1Mel 1.1, while the price of cobalt chloride and cobalt sulfate fluctuates around 1.

Affected by the epidemic, there was only a brief discount of other cobalt products to cobalt sulfate in February, mainly due to the outbreak of the new crown in China in February, logistics and workers' rework were blocked, large factories of ternary precursors did not stop work during the Spring Festival, cobalt sulfate was in short supply, and prices rose. However, the production and sales of new energy vehicles have been seriously affected by the epidemic, and overseas epidemics broke out one after another in March. Export orders for ternary precursors have been reduced, demand for cobalt sulfate remains low, prices are upside down, and other cobalt products continue to raise water for cobalt sulfate.

In terms of metal cobalt, the epidemic in Europe and the United States has affected the sharp reduction in demand for superalloys and magnetic materials, and reduced export orders for metal cobalt; domestic demand has recovered slightly, but the overall price of metal cobalt is more difficult to improve.

SMM expects that the price gap between cobalt and cobalt salts will narrow in the third quarter, the terminal demand for batteries will gradually recover in the third quarter, and cobalt salt prices may rebound, but overseas epidemic control is not optimistic and the expected increase is limited. The possibility that the outbreak in Africa will affect the supply of cobalt raw materials and the price of cobalt may fluctuate sharply.

We are pleased to provide the whole market with the newly launched SMM China Cobalt Lithium New Energy Weekly (click to view) to help you keep track of the weekly hot spots of China's cobalt lithium new energy industry chain and gain an in-depth understanding of market supply and demand changes and price trends.

SMM's newly launched Cobalt Lithium New Energy Industry Weekly mainly tracks the market trends and price changes of the whole industry chain in China, such as cobalt, lithium, precursors, battery materials, lithium batteries and new energy vehicles, while reviewing weekly hot events and topics, with lithium battery as the core series of the entire industry chain, by showing the most clear industry data, conduct panoramic in-depth analysis.

In SMM China Cobalt Lithium New Energy Weekly, you can learn about the price, output, capacity, operating rate and inventory changes of each product in the cobalt and lithium industry chain. We will also track the demand changes and national policies of the global lithium battery terminal market (including new energy vehicles, 3C consumer electronic products, etc.) to give a comprehensive overview of the cobalt lithium new energy industry chain.

If you want to know more about China's cobalt lithium new energy industry chain data, you are welcome to subscribe to our SMM China Cobalt Lithium New Energy monthly report and China Cobalt Lithium New Energy Database.

Welcome to contact SMM Cobalt Lithium New Energy Research team:

Qin Jingjing 021 Murray 51666828

Mei Wang Qin 021 Mui 51666759

Huo Yuan 021 Murray 51666898

Liu Xiaoxia sales Manager 13916447260

![[SMM Analysis] South Korea's Battery Industry Is Shifting from Product Competition to Supply Chain Competition](https://imgqn.smm.cn/usercenter/WBREf20251217171728.png)

![[SMM Anlalysis] Korea’s Battery Industry Enters a Phase of Utilization Adjustment](https://imgqn.smm.cn/usercenter/WgbTp20251217171727.jpg)