SMM7 March 14: at the "2020 (Fifth) China International Nickel-Cobalt-Lithium Summit Forum" and China International Nickel-Cobalt Industry chain Summit held by SMM, Liu Yuqiao, senior analyst of Shanghai Nonferrous net Nickel Industry, made a price review and market forecast for the 2019-Mill 2022 Chinese nickel market.

Nickel supply side: great changes have taken place in the stable structure of China's total primary nickel supply

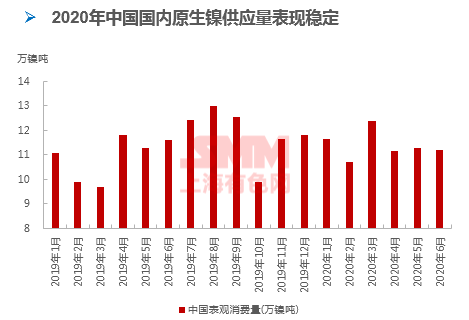

In 2020, China's primary nickel supply fluctuated between 10 and 120000 tons per month, a stable performance compared with last year's data. Although the quantity has not changed much, its structure has changed obviously. As can be seen from the figure on the right, the changing trend of domestic primary nickel supply structure:

1. Increasing trend: import Ferro-nickel. The increment of imported nickel iron mainly comes from Indonesian nickel pig iron, and with the further expansion of Indonesian nickel pig iron, it is still in an increasing trend.

2. Shrinking trend: domestic nickel pig iron and imported electrolytic nickel. Since the mineral ban in Indonesia, domestic nickel pig iron is facing strong cost pressure, and the phase-out and production reduction process of small and medium-sized enterprises will continue in the next few years, while the decrease of imported electrolytic nickel is mainly affected by the reduction of pure nickel consumption in Chinese stainless steel plants.

3. The proportion is basically stable: domestic electrolytic nickel, general nickel, nickel salt.

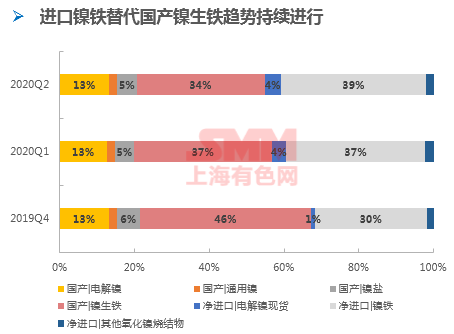

Nickel supply side: imports of pure nickel decreased compared with the same period last year.

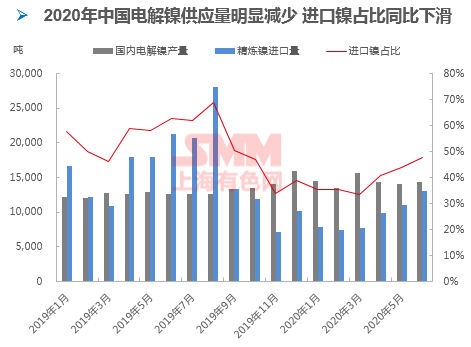

As can be seen from the chart, the supply of electrolytic nickel in China decreased significantly in 2020 compared with last year, mainly due to a reduction in the amount of imported electrolytic nickel, and the output level of domestic manufacturers was relatively stable.

The import of electrolytic nickel in China has dropped from 10-20 000 tons per month to only about 4000 tons per month, reflecting a significant decline in domestic demand, which is caused by more use of nickel pig iron instead of electrolytic nickel in 300 series stainless steel plants.

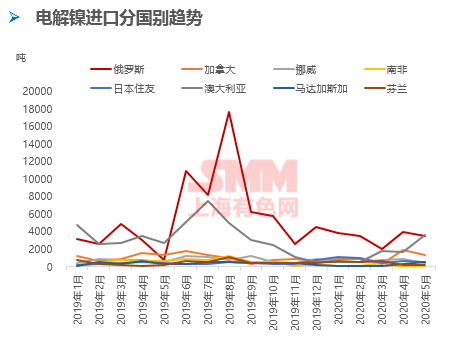

As can be seen from the chart, Russian nickel, which is mostly used in stainless steel, still occupies an important position in China's electrolytic nickel imports, but the quantity is much lower than before; pure nickel imported from Australia, mainly nickel beans, is used in stainless steel plants and nickel sulfate plants, and its demand is highly related to performance-to-price ratio, and monthly imports fluctuate greatly, with an average of 20003,000 tons per month.

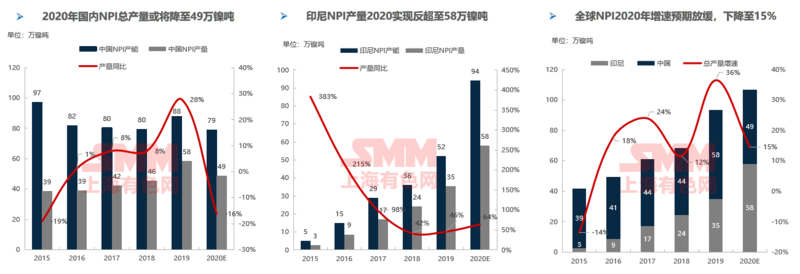

The substitution of Indonesian nickel pig iron to domestic nickel pig iron will further occur in 2020.

From the production capacity and production data and expectations of nickel pig iron, the replacement of Indonesian nickel pig iron with domestic nickel pig iron will further occur in 2020. After the increase in Indonesian nickel pig iron production makes up for the reduction in China, the total volume maintains growth, but the growth rate slows down to 15%.

SMM statistics show that from January to June 2020, the cumulative output of Ferro Nickel in Indonesia was 254200 nickel tons, while that in China was 249900 tons. Indonesia's output exceeded that of Ferro Nickel and became the largest producer of Ferro Nickel.

SMM predicts that China's Ferro Nickel will drop to 490000 Nickel tons in 2020 from 580000 Nickel tons in 19 years, while Indonesia Nickel Iron will increase from 350000 Nickel tons in 19 years to 580000 Nickel tons in 2020.

Indonesia's production lines for commissioning and reaching production are still relatively dense in the third quarter. It is estimated that by the end of the third quarter, Indonesia's cumulative annual output will reach 409200 nickel tons, while China's annual output will reach 372900 tons. The output gap will widen, and the nickel-iron supply pattern will change.

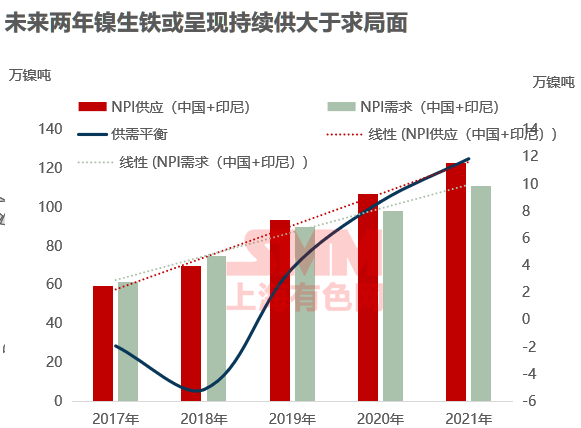

镍生铁供需平衡表:印尼快速投产 过剩幅度有所增加 三季度将较二季度过剩

镍生铁供需平衡表:印尼快速投产 过剩幅度有所增加 三季度将较二季度过剩

Although the epidemic in Indonesia is also severe, the progress of nickel pig iron production has not been significantly affected, and the logistics of Indonesian nickel pig iron to China has been normal, and the production progress is slightly faster than expected; according to current estimates, the start-up of the new project makes the growth rate of supply faster than the growth rate of demand, and nickel pig iron will be in abundant supply this year and next year.

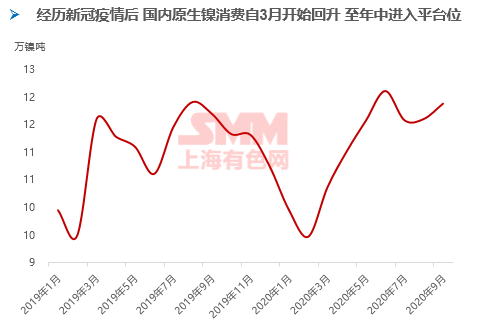

Overview of China's Primary Nickel consumption in 2020: domestic Primary Nickel consumption will gradually pick up after the first quarter

Except that the monthly consumption of primary nickel in China was affected by the Spring Festival and the epidemic in the first quarter, the normal level is about 11-120000 nickel tons per month. The biggest factor affecting the consumption of primary nickel is the production of stainless steel plants, which is huge and stable most of the time.

In 2020, since the middle of the year, the growth rate of domestic primary nickel consumption has entered the platform to show a fluctuating trend, and after recovering from the epidemic, the dividend of replenishment in the lower reaches has gradually faded, and the market in the second half of the year will be more in line with the actual consumption situation downstream.

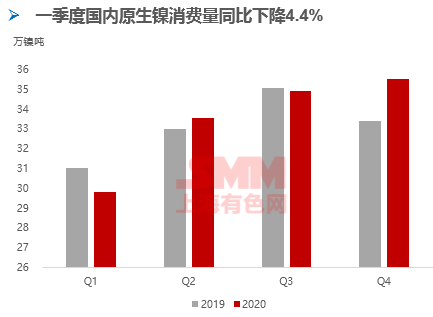

In terms of quarterly consumption, if the production of domestic stainless steel plants can remain normal, and considering the slow recovery of other nickel downstream, consumption in the fourth quarter of this year will increase slightly compared with the third quarter; the collapse in prices in the fourth quarter of last year is related to the strong intention of stainless steel to go to the warehouse and reduce production to seek to improve profits. This year, the consumption end of stainless steel is slightly weak, which is a major negative factor, but nickel prices are already in a low range, the raw material nickel pig iron is also in sufficient supply, and mainstream stainless steel manufacturers may not significantly reduce production, but while raw materials are still depressing prices, putting pressure on nickel prices.

Nickel downstream PMI interpretation: stainless steel and alloy have entered the off-season battery industry and entered the recovery track electroplating industry is still in a cold winter.

Stainless steel future outlook: the stainless steel industry PMI composite index in July was 49.45%, down 0.81% from the final value in June and below the rise and fall line. The researchers believe that after the domestic epidemic gradually got rid of the influence of the epidemic in the second quarter, the replenishment of the intermediate link and downstream enterprises was basically completed, and after that, there was no new positive appearance in the market for the time being, and the overall consumption form itself was relatively weak in the second half of the year. In July, as a traditional off-season, the overall supply exceeds demand pattern will be more obvious.

Battery outlook: the initial value of the battery industry PMI composite index in July was 60.11%, up 7.59% from the final value in June and higher than the rise and fall line. Due to the stimulation of consumption encouragement policies in Europe and the United States, there has been a certain pick-up in overseas terminal market consumption, resulting in an increase in orders for precursor high-nickel products, ternary material factories and the purchase of raw materials; while the performance of the Ni-MH battery industry is mediocre, except that the leading enterprises have gradually returned to normal, the orders of other peer enterprises have not recovered significantly. Some surveyed companies said that the order situation will continue to improve in July, while for poorer companies, it will only maintain the previous level and will not worsen further, so the battery industry is expected to improve in July compared with June.

Alloy casting post-outlook: the initial value of the PMI composite index of the alloy industry in July is 48.24%, which is expected to decrease by 0.52% compared with the final value in May, and is expected to be still lower than the rise and fall line. Among them, the production index dropped to 48.31%, mainly due to environmental protection factors in North China, and some special steel plants are expected to start overhauling one after another in July, which may have a greater impact on the alloy casting production line. The index of new orders fell to 46.02%, and more operators said that after entering the off-season of terminal consumption, the number of orders received in July may be lower than that in the previous period. The raw material index is 46.57%, and the purchasing volume index is 48.76%, which is also correspondingly lowered due to the manufacturer's production schedule.

Electroplating outlook: in July, the initial value of the PMI composite index of the electroplating industry is 45.60%, which will still be lower than the rise and fall line. Among them, the production index is 42.06%, and the new order index is 43.74%. After entering the traditional off-season of electroplating, in addition to local environmental protection requirements, it is also affected by high temperature power transfer, so the electroplating industry is more pessimistic about July. At the same time, procurement volume and raw material inventory also dropped to 45.59% and 46.36% due to low operating rate.

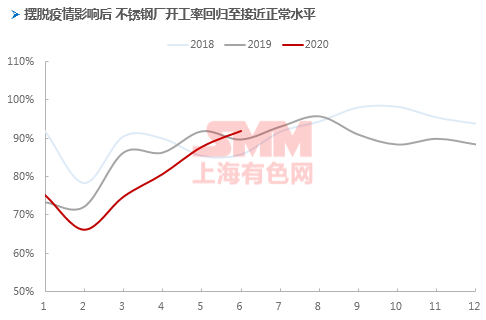

Stainless steel got rid of the influence of the epidemic earlier and returned to the normal operating rate level to provide bottom support for primary nickel demand.

The picture shows the operating rate of domestic stainless steel plants. It can be seen that during the epidemic period, the operating rate of the stainless steel industry decreased significantly compared with previous years, while the operating rate of the stainless steel industry from April to May has gradually returned to the normal level.

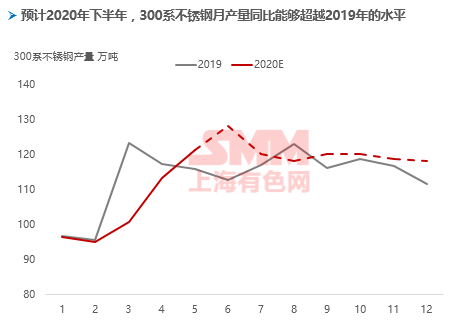

The picture shows the output of 300 series stainless steel plants in China, which directly affects the domestic consumption of primary nickel. It can be seen that from April to May, the output of 300 series has hit a new high again, and then stabilized at a high level, and it is expected that the year-on-year output in the second half of the year will be higher than that in the same period last year. This will provide some support to the demand for primary nickel. However, in the specific nickel raw material procurement decision, due to the obvious economy of nickel pig iron, the demand for nickel pig iron will be higher than in previous years, while the purchase of pure nickel has shrunk to the minimum compared with last year.

As mentioned earlier, due to the impact of the epidemic, the consumption of stainless steel is slightly weak this year, which is a major negative factor, but in the range where the nickel price is already low, the supply of raw material nickel pig iron is also sufficient, and mainstream stainless steel manufacturers may not significantly reduce production. However, the price of raw materials is still depressed, putting pressure on the price of nickel.

Stainless steel: the trend of going to the warehouse slows down the market and re-enters the situation of small surplus.

After the domestic epidemic, the downstream replenishment demand supports the high and downward inventory, while after the replenishment dividend, the supply continues to exceed demand under the existing domestic demand situation, and the subsequent stainless steel inventory or stop reducing the warehouse even appears the situation of base warehouse.

Under the pressure of high inventory and low profit, the stable production of steel mills in the second half of the year will depend on the sustained low price of raw materials. Under the condition that the raw materials of nickel pig iron are sufficient, the steel mill is more likely to maintain normal operation.

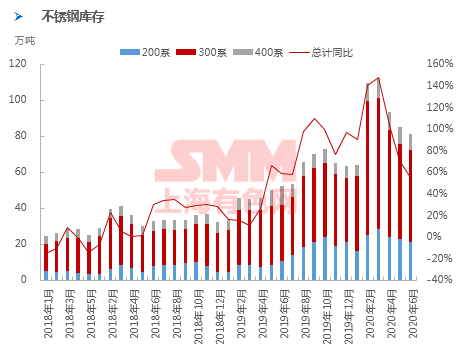

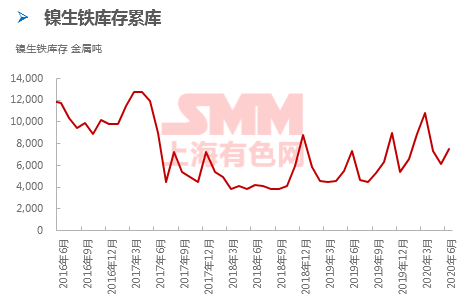

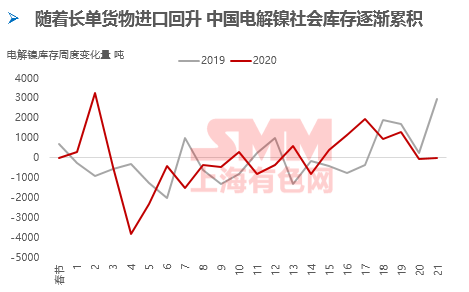

Inventory of Nickel: there is a small accumulation trend in China. Pure Nickel consumption is sluggish, while Nickel Pig Iron is mainly due to a greater increase in supply.

Most of the domestic primary nickel inventory is still concentrated in nickel pig iron, but for deliverables, attention should be paid to the inventory of electrolytic nickel.

With the increase of the import of nickel pig iron in Indonesia, the domestic supply of nickel pig iron is becoming more and more abundant, and the amount of domestic stainless steel factories using nickel pig iron instead of pure nickel has reached its peak since last year. The overall trend of nickel pig iron this year is mainly a small accumulation bank. In the future, more Indonesian nickel pig iron will enter, squeezing out the share of domestic nickel pig iron.

In terms of electrolytic nickel, the domestic demand has shrunk obviously, and even if the import volume has dropped sharply compared with the same period last year, there has been a trend of a small accumulation of electrolytic nickel since May to June. In the later stage, as nickel beans become deliverable in the previous period, more overseas sources may flow in, increasing the pressure on domestic nickel stocks.

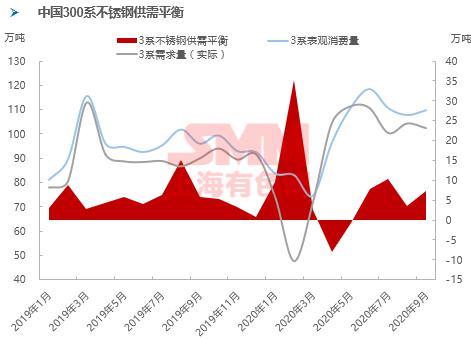

Nickel outlook: affected by the epidemic and the rapid commissioning of NPI in Indonesia, the excess supply of primary nickel in China in 2020 is significantly higher than that in previous years.

Quarterly balance sheet: with the increase in the amount of ferronickel returned to Indonesia, the balance sheet of domestic primary nickel supply and demand gradually tends to be loose, but it will not be worse than in the first quarter; in addition, most of the excess range is still dominated by nickel pig iron imports. the actual performance of nickel price also needs to consider the impact of macro factors on the environment of pure nickel consumption.

Annual balance sheet: affected by the epidemic and the rapid commissioning of NPI in Indonesia, the excess supply of primary nickel in China in 2020 is significantly higher than in previous years.

Review of Nickel Price trend: the rebound of Nickel Price after the epidemic is limited

Before the Spring Festival holiday, the price of nickel, which has been weak since the fourth quarter of last year, once stopped falling, mainly due to the reduction of stainless steel production. However, during the Spring Festival, the new crown epidemic broke out in China, and the prices of most metal varieties fell sharply. Nickel prices also fell.

When the supply side returns to the market after the second festival, the supply side recovers quickly from the epidemic, but both the logistics link and the consumer side recover slowly, the stainless steel stock is extremely high, and the price of stainless steel falls sharply; the price of crude oil also falls sharply, dragging down the trend of all metals, and the price of nickel is hit again, but there are signs of improvement in fundamentals, and prices are gradually bottoming out.

(3) the domestic stainless steel production returned to normal, which obviously supported the consumption of primary nickel, coupled with a large reduction in production in domestic nickel pig iron plants, the fundamentals of domestic primary nickel improved in the second quarter.

(4) the production of Indonesian nickel pig iron is accelerated at a high speed, and the follow-up consumption of the stainless steel industry is not good after consuming the replenishment dividend at the initial stage of the recovery of the epidemic, but European and American countries are committed to recovering from the epidemic, economic data are improved, and nickel prices show a volatile trend under the long-empty interweaving.

Although experienced a rebound and shock, nickel prices still failed to return to January's high, that is, Shanghai nickel 113320 yuan / ton, Lunni 14395 US dollars / ton. (spot settlement price)

Interpretation of Chinese Nickel Sulfate Market in 2019 / 2020

Analysis on the supply of Raw Materials in China's Nickel Sulfate Industry in 2020

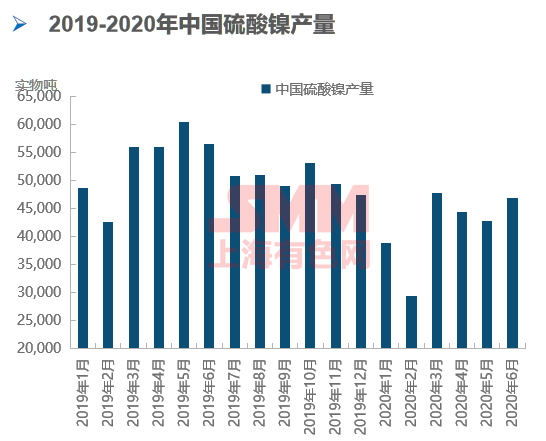

In 2019, China's total output of nickel sulfate was 621400 physical tons, of which battery-grade nickel sulfate accounted for about 89.5%; in the first half of 2019, China produced 320400 physical tons of nickel sulfate. In the first half of 2020, China's total output of nickel sulfate was about 250000 physical tons, of which battery-grade nickel sulfate accounted for about 87%, a decrease of 70400 physical tons compared with the same period last year. The demand for nickel sulfate decreased mainly because the epidemic affected terminal consumption.

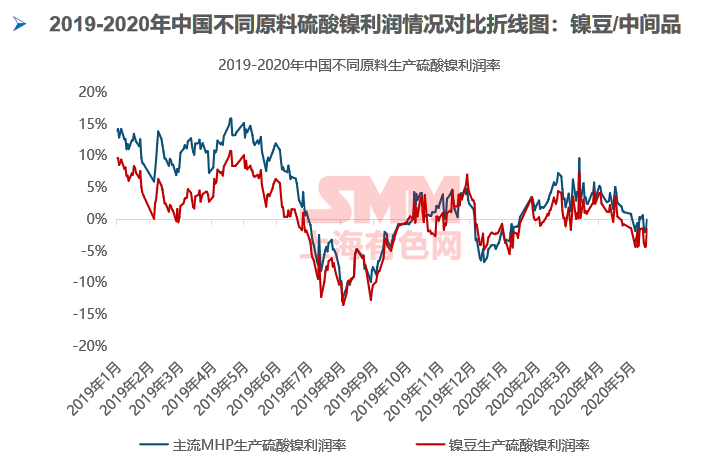

The picture on the right shows a comparison of the profits of raw materials for the production of nickel sulfate. We can see that the general trend in 2020 is much lower than that in 2019, maintaining near the profit and loss line. Mainly due to the weak demand in the lower reaches this year, the sales price of nickel sulfate products is difficult, and the cost of raw materials is relatively high.

Analysis on the supply of Raw Materials in China's Nickel Sulfate Industry in 2020

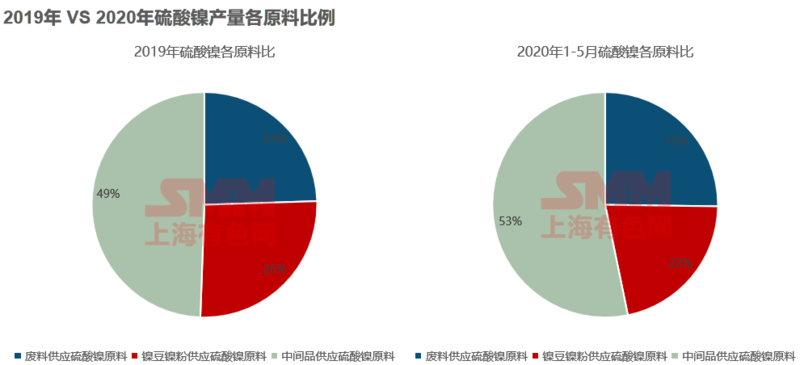

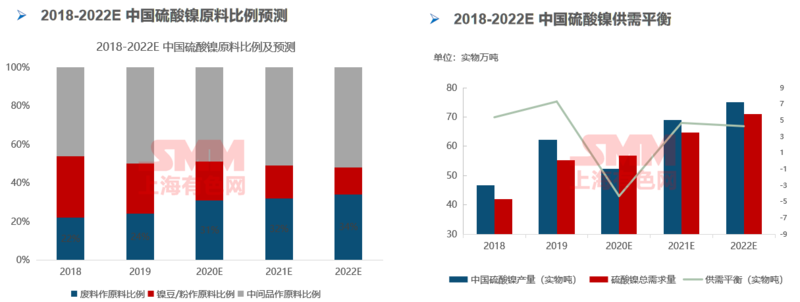

The proportion of raw materials for the supply of nickel sulfate from waste is relatively stable in 2020, and the economy of using nickel bean nickel powder and intermediate products in the first half of 2020 is poor, and the waste still has a stable advantage. The proportion of nickel sulfate raw materials supplied by intermediate products increased relatively significantly in the first half of 2020, mainly due to the decrease of downstream consumption, the amount of waste was reduced, and the waste raw materials were limited. In order to maintain production, nickel sulfate manufacturers choose intermediate products as raw materials according to the comparison of stability and economy. In addition, some nickel sulfate plants also have a long list of intermediate products, which need to be received according to the contract.

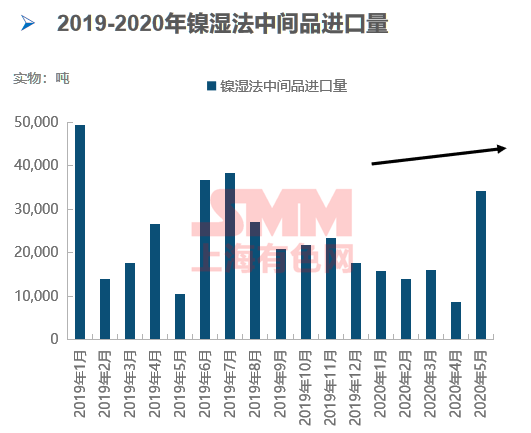

The increase in imports of nickel wet intermediates in May 2020 was mainly due to the postponement of import data to May in Papua New Guinea due to the epidemic in April. In addition, the import quantity of nickel wet intermediates in Finland was 0 in May. It is understood that Finnish nickel wet intermediates have been shipped normally, or due to delays in customs declaration, imports will return to normal from June to July.

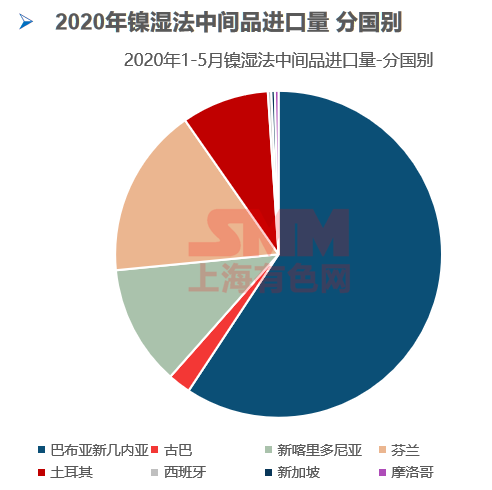

From January to May 2020, the main importers of nickel wet intermediates were Papua New Guinea, accounting for 59.28 per cent, and Papua New Guinea imported 28400 tons of nickel wet intermediates in May, accounting for 83 per cent of the total imports of nickel wet intermediates in May; Finland accounted for 16.86 per cent; New Caledonia accounted for 11.92 per cent.

Analysis on the downstream demand of China's Nickel Sulfate Industry in 2020

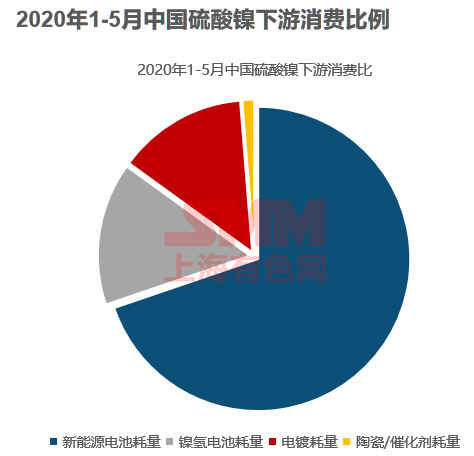

Downstream consumption of nickel sulfate in China from January to May 2020: new energy battery consumption accounts for 69.78%; Ni-MH battery accounts for about 15.18%; electroplating industry 13.77%. The consumption of nickel sulfate by new energy batteries has exceeded 2/3 of the total consumption of nickel sulfate, so the fluctuation of the new energy market is enough to affect the demand of nickel sulfate market.

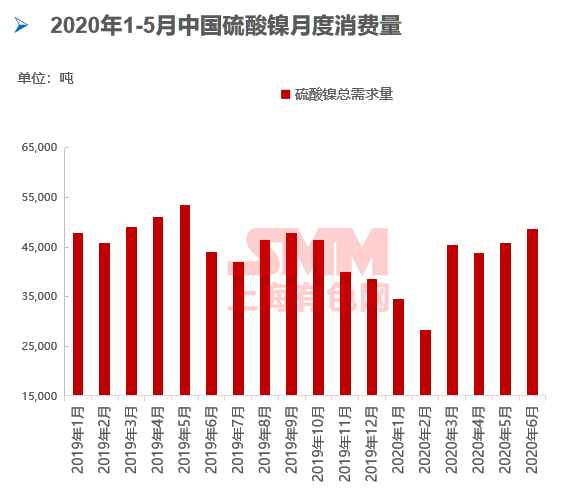

The figure on the right shows our monthly consumption trend, which shows a rebound after the epidemic, which is still relatively weak compared with the same period last year. In 2020, due to the outbreak of the domestic epidemic in January, more factories of nickel sulfate and downstream enterprises stopped production from January to February, and production gradually resumed in March, due to a certain pick-up in the backlog of downstream demand in the previous two months; with the outbreak of the foreign epidemic at the end of March, downstream orders were affected, and the demand for nickel sulfate weakened again in April and returned to a state of slow recovery from May.

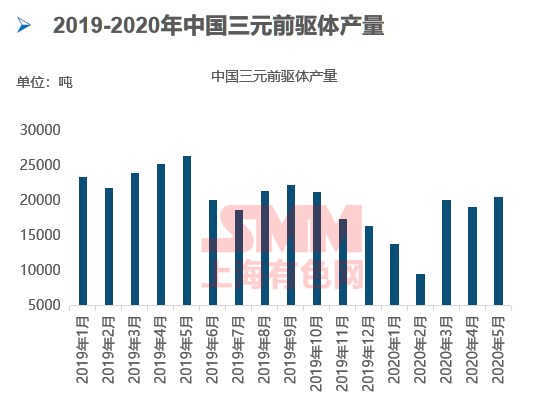

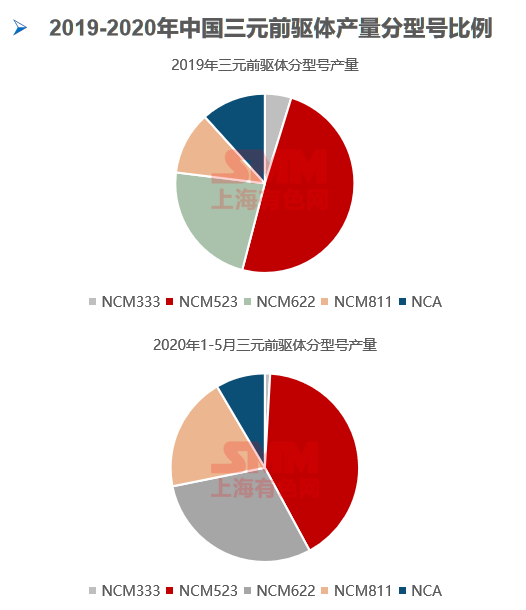

The total output of ternary precursors in China was about 257800 tons in 2019 and 82900 tons from January to May 2020, a decrease of 31 percent compared with the period from January to May in 2019. This year is supposed to be a year of rapid development of the ternary precursor, but the export of the ternary precursor accounts for a large proportion, while overseas car companies have been affected by the epidemic for a long time, and the epidemic has a great impact on the production and consumption downstream of the ternary precursor. The proportion of high nickel in 2019 is 23%, the proportion of 3 series is 5%, and from January to May 2020, 28% of high nickel is 28%. It is expected that the proportion of high nickel will be higher and higher in the future, and 3 series may be phased out.

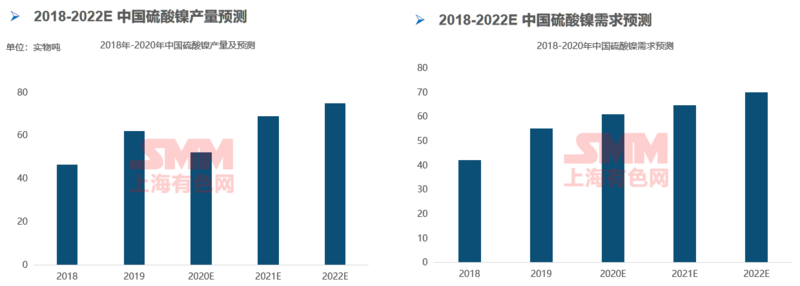

Forecast of supply and demand of Nickel Sulfate in China in 2020

It is estimated that the total output of nickel sulfate in 2020 will be 523100 physical tons, a decrease of 15.82% compared with the previous year. On the one hand, due to the large accumulative inventory of nickel sulfate in 2019, about 72500 physical tons; on the other hand, due to the reduction of terminal consumption and downstream demand of nickel sulfate affected by the epidemic this year, the price of nickel sulfate is close to the cost, and most nickel sulfate plants choose to reduce production or stop production. It is expected that with the improvement of the epidemic next year, the terminal consumption of nickel sulfate will pick up under the stimulus of the policy, and the production of nickel sulfate will also increase.

The proportion of waste increased to 31% in 2020, and the proportion of nickel bean powder decreased, mainly because the market price of battery-grade nickel sulfate was low, so it was difficult to cover the processing fee of nickel bean powder, so many manufacturers chose to increase the waste proportion of raw materials and reduce costs; precursor factories choose to buy nickel sulfate directly. It is expected that the proportion of waste will continue to increase in 2021, the Indonesian nickel wet intermediate project will gradually begin to increase, and the proportion of nickel bean nickel powder may decrease.

The total output of nickel sulfate is expected to decrease by 523000 physical tons in 2020, 98000 physical tons lower than last year, and the total demand for nickel sulfate is 569000 tons. Taken together, it is expected that 43200 physical tons of nickel sulfate will be eliminated this year in 2020 due to low profits and weak market demand for nickel sulfate. Most nickel sulfate plants choose to reduce production or stop production to eliminate inventory, so supply and demand in 2020 is relatively balanced.

"Click to view the SMM nickel industry chain database

2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum

Scan the QR code, apply for participation or join the SMM metal exchange group