SMM5, March 11: according to SMM research, the main blast furnace steel plant producing building materials in May produced 9.156 million tons of thread, an increase of 15.24 percent over April, and a month-on-month increase of 392000 tons (17.23 percent) over the previous month. Among them, affected by the epidemic, the international demand for iron and steel was depressed, and the export orders of domestic steel mills fell sharply, resulting in an increase of 15.97% in the supply of thread domestic trade and 25.27% in the supply of thread domestic trade.

The increment of production scheduling mainly comes from two aspects: maintenance and resumption of production and the turn of molten iron.

On the one hand, the maintenance of the steel mill is centralized and resumed production.

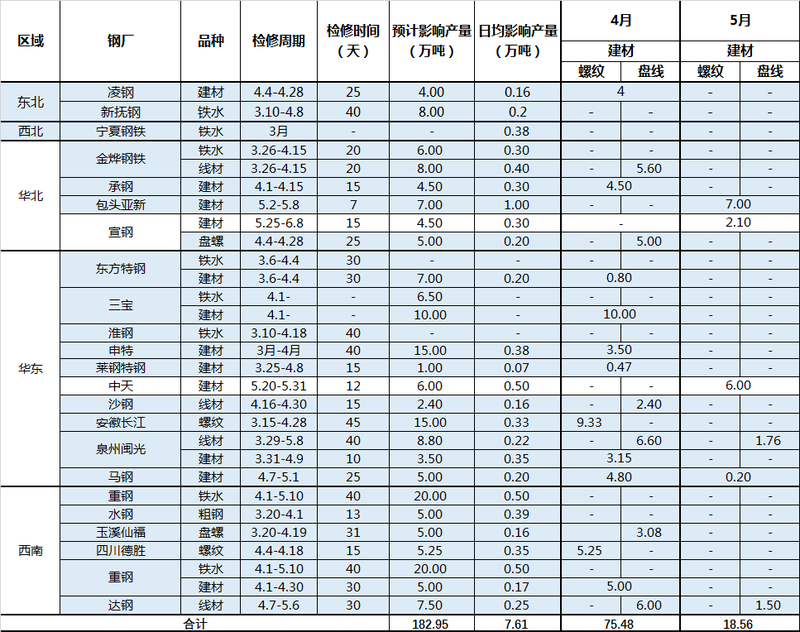

According to the SMM survey as of May 11, the reduction in building materials affected by the overhaul of steel mills in May was 185600 tons, down from 754800 tons in April.

Table 1: list of maintenance of building materials in steel mills from April to May (unit: 10,000 tons)

Source: SMM

On the other hand: hot metal steering thread

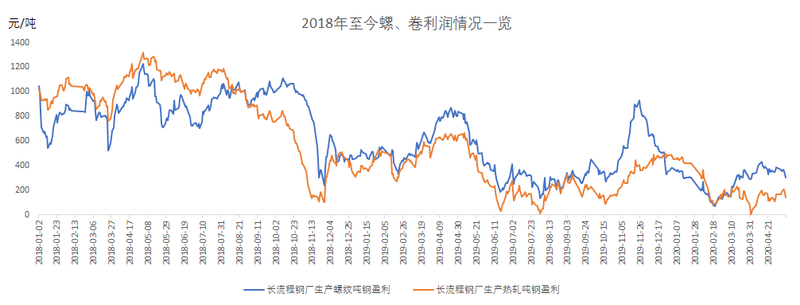

According to the calculation of SMM data model, as of May 11, the profit difference per ton of steel in the production of thread and hot coil was 161.7 yuan, and the profit of common steel varieties such as industrial wire rod was also inferior to that of thread, resulting in molten iron turning to thread production. According to the SMM survey sample, the thread increment caused by hot metal steering this month is about 217000 tons.

Figure 1: profit difference of coiled snail per ton steel

Source: SMM

[subregional]

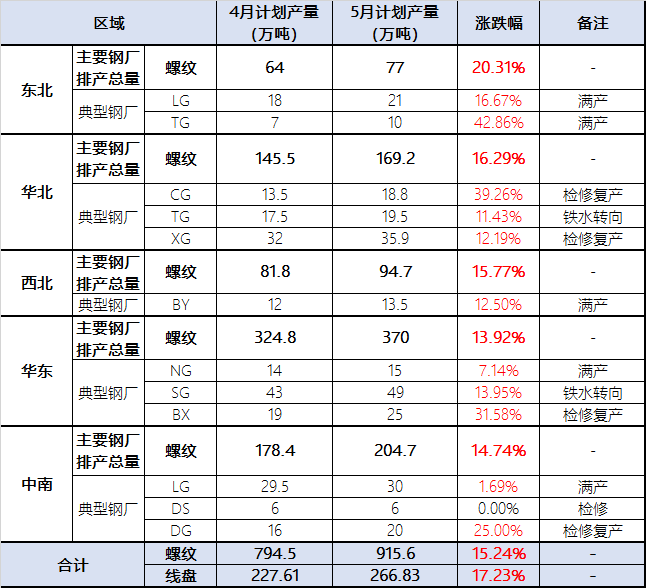

Northwest region: thread scheduling increased by 15.77% month-on-month this month. The completion of overhaul of local steel mills such as LG and NG has contributed to the main increment of production scheduling.

North China: thread scheduling increased by 16.29% this month compared with the previous month. Mainly due to: on the one hand, the hot metal shift is still going on, on the other hand, the recent demand recovery in the northern region is better, the market shipping situation is better, and the thread inventory pressure has been significantly alleviated, resulting in an increase in the willingness of steel mills to meet production.

Northeast: thread scheduling rose 20.31% this month compared with the previous month.

East China: thread scheduling increased 13.92% this month compared with the previous month. The overhaul of steel mills in East China was relatively concentrated in April, and the increase caused by overhaul and resumption of production in May was more obvious.

Central and southern regions: thread production increased by 14.74% month-on-month this month. The main increment comes from overhaul and resumption of production, and some steel mills increase production by increasing the scrap ratio.

Table 2: production schedule of building materials in regional steel mills from April to May 2020

Source: SMM

At present, in May, the steel mill has basically reached a state of full production, and the room for continued substantial growth is very limited. And according to the research situation, the vast majority of steel mills have entered the state of full production one after another since the middle and late April, so for the spot market, the incremental pressure reflected by the late supply side is gradually weakening, and the suppression effect on the spot market will also gradually decline. Under the strong support of demand, the spot price still has a fighting force.