SMM5 11: non-ferrous metals rose, Shanghai aluminum Shanghai tin rose more than 1%. In the past, China took the lead in the recovery of domestic production, and the construction industry, represented by infrastructure investment, accelerated its recovery and demand improved. Since May, market confidence has been boosted as economies restart. In terms of copper, SMM data show that the tax price difference between bright copper and copper electrolytic copper is 619 yuan / ton, an increase of 251yuan compared with the previous month. In particular, the tax price difference between bright copper supply and electrolytic copper in Jiangxi is close to 1000 yuan, which makes the price difference between scrap copper rod and refined copper rod open quickly. Although the advantage of scrap copper rods instead of electrolytic copper rods will expand, which will lead to an increase in demand, it will not allow the supply of scrap copper rods to recover quickly. "it mainly depends on the problem of scrap copper raw materials." in view of the obvious improvement in the domestic epidemic compared with the beginning of the year, terminal consumption has also picked up in the near future. The Association said that the recent downturn in international oil prices has also subverted consumers' expectations of rising oil prices, and that the low price of domestic refined oil products has also reduced the use costs of users, which is conducive to promoting consumption in the car market. Wholesale sales of new energy passenger vehicles in April were 64000, down 30 per cent from a year earlier and up 14.8 per cent from March. Retail sales in the passenger car market reached 1.429 million in April, down 5.6 per cent from a year earlier, the strongest monthly trend this year. The year-on-year growth rates in March and April both reached nearly 40 percentage points, reflecting a good trend of V-shaped recovery at the bottom since the epidemic.

The black series rose slightly at midday, the thread heat rose 0.03%, and the iron ore was flat. According to the latest SMM tracking, the 35 mainstream hot rolled coil mills surveyed totaled 9.3429 million tons of hot rolled commercial materials in May, an increase of 3.1 percent over the actual output of 9.0624 million tons in April. This is mainly due to the resumption of maintenance and production in steel mills and the increase in cold and heat transfer. As for the relevant sectors, according to statistics, the total sales of excavators in April were 45400, up 59.9 percent from the same period last year. At present, the actual demand of excavator terminal is good, which leads to the growth of steel demand. Iron ore port inventories continue to decline, short-term supply is tight to boost ore prices, but there is a risk of a pullback in the medium to long term.

Crude oil fell 1.66% in the previous period. International oil prices fell on Monday as fears of oversupply continued and the economic downturn caused by the new crown epidemic offset support from production cuts in some oil-producing countries around the world. Us crude oil futures for July fell 65 cents, or 2.5 percent, to $25.51 a barrel. Brent July crude oil futures fell 41 cents, or 1.32 percent, to $30.56 a barrel. While more countries are turning to loosening restrictions to prevent and control the epidemic, which could support a rebound in oil demand, signs of a second wave of new crown virus outbreaks are worrying investors.

The trading was suspended at noon.

Today's spot

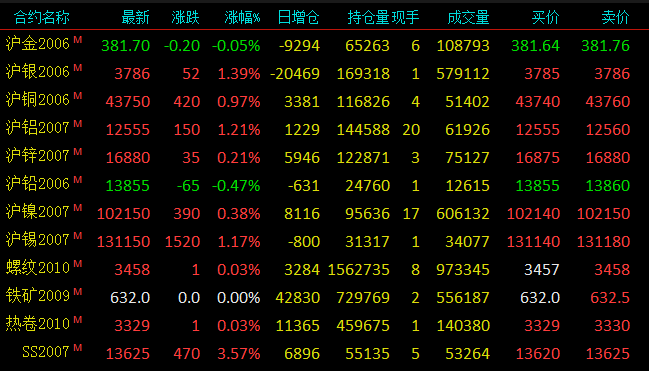

Lead: South China lead in Guangdong market is 14100 yuan / ton, the average price of SMM1# lead is 50 yuan / ton. Henan Yuguang, Wanyang and other smelters are mainly Jiaochang single, Jinli, Wanyang 14000 yuan / ton, the average price of SMM1# lead discount 30 yuan / ton (traders); Hunan Shuikoushan 14100 yuan / ton, the average price of SMM1# lead rose 50 yuan / ton; Hunan Jingui 13950 yuan / ton, the average price of SMM1# lead discount 100 yuan / ton. Jiangzhong 14150 yuan / ton, the average price of SMM1# lead flat water quotation. Yunnan small factory 13800 yuan 13850 yuan / ton, the average price of SMM1# lead discount 20000250 yuan / ton quotation. Today, the market bulk quotation continues to fall, the primary lead market trading is light, the market is mainly recycled lead trading.

Zinc: Guangdong zinc mainstream transaction in 16870-16970 yuan / ton, the quotation focused on Shanghai zinc 2006 contract rose 0-40 yuan / ton, Guangdong market compared with Shanghai stock market discount 110 yuan / ton is flat compared with the previous trading day. The first trading period, futures prices are still strong, but Guangdong inventory changes little, the initial holder is still quoted higher, but heard that Guangdong bonded area has imported zinc inflow, the market active shipment, spot rising water has also been reduced. Kirin, Mengzi, Huize, Tiefeng quoted price for Shanghai zinc contract for 6 months, 10Lue 40 yuan / ton, Feilong water 100 yuan / ton. In the second trading session, prices are still high and volatility, downstream procurement volume is still limited, individual holders continue to lower prices for shipment, spot water pressure, but near delivery, the margin of discount to futures that month is limited, the holder continues to adjust the price is insufficient. Kirin, Mengzi, Huize and Tiefeng quoted 0-20 yuan / ton for the June contract. Kylin, Mengzi, Huize, Tiefeng mainstream transaction in 16870-16970 yuan / ton.

The mainstream transaction in Ningbo was 17000-17100 yuan / ton, the ordinary brand rose 110-130 yuan / ton to the 2005 contract, and the price difference between Ningbo and Shanghai ordinary brand remained near 30 yuan / ton on Friday. Today, zinc prices slightly revised back, Shanghai rising water gradually lower, Ningbo market slightly followed, but traders' willingness to ship has weakened. In the first trading session in the morning, the holdings quoted in Huize, Tiefeng, Hualian and West Mine rose 120 yuan / ton on the May contract, while Kirin reported a rise of about 150 yuan / ton on the May contract. Entering the second trading session, transactions remained weak, some shippers suspended shipments, most brand prices gradually reduced by 20 yuan / ton, Kirin reported in May to rise 130 yuan / ton, the rest of the brand reported at 100-110 yuan / ton. Overall, today's market transaction atmosphere compared with last Friday, the transaction situation is very light.

The mainstream trading of zinc in shanghai was 17030copyright 17060 yuan / ton, while that of Shuangyan and Chihong was 17050ly17070 yuan / ton. Shuangyan and Chihong quoted a quotation of 100 yuan per ton in May for rising water. Shuangyan and Chihong quoted a price of 100 yuan per ton in May, and the mainstream transaction of zinc in Shanghai was 16960 million yuan. 16990 yuan / ton. Shanghai zinc 2005 contract low rebounded, the morning market closed at 16765 yuan / ton. The zinc price is high in the day, the smelter shipments are normal, the traders are mainly shipping, the domestic price in the morning market is about 100-110 yuan / ton, or the average price / average price is-5, the transaction activity is higher on the basis of the net average price, and then some traders report that the water 80 shipment is better, other holders follow the adjustment, and the domestic quotation is lowered to 90-100 yuan / ton. And in the second trading session, it was further adjusted to about 100 yuan / ton of Shengshui 80, mainly trading by traders. And downstream continues to fear heights wait-and-see, even if passive purchase is only do just need to purchase, affected by the following tour as the main audience Shuangyan, import quotation continues to lower than last Friday, but the transaction is still mediocre. Overall trading during the day was broadly flat compared with last Friday.

"2020 (15th) lead and Zinc Summit

Updating.

SMM "current combination" training class

Registration contact: Lu Qingping, Iron and Steel Division of SMM

Tel: 021-51595781 / 187-1777-4590

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)