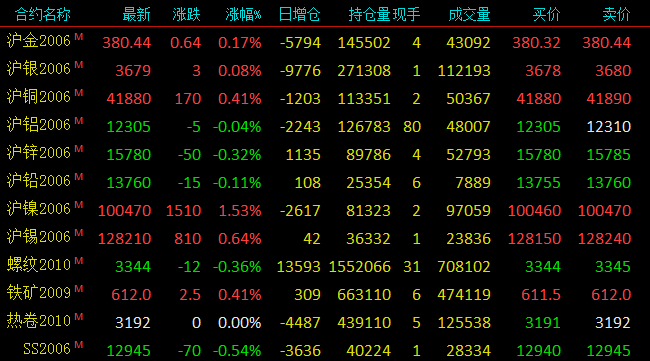

SMM4 24: a few days earlier this week due to the oil market turmoil affected the non-ferrous market, but the recent impact significantly reduced, market logic tends to fundamentals. Shanghai nickel rose 1.53% on news that the new quarantine in the Philippines would be extended until May 15. Zambales, one of the main mining areas in the Philippines, is dominated by Zhonggao nickel mine, but the volume of shipments in the area is relatively small, which is expected to affect the export volume of 2-3 ships. After the implementation of the ban, the Indonesian government's nickel mine trade revenue has been greatly reduced, and the interests of the miners have been damaged a lot. The recent official pricing may raise the cost of Indonesia's nickel pig iron smelter. Costs have risen more for some of China's biggest Indonesian companies to build nickel and iron. In addition, Peru has renewed its state of emergency. Since Peru declared a state of emergency, the, Las Bambas copper mine has reduced its operating ratio, the transport of copper concentrate has been interrupted, and force majeure has been issued to the Las Bambas copper concentrate sales contract. The production guidelines for the whole of 2020 have also been revoked, and the movement of people and goods has been severely restricted, further leading to a decline in the overall annual copper production of MMG2019.

Black steel is weak and volatile as demand slows and storage falls short of expectations. Total national stocks of building materials this week were 15.043 million tons, a month-on-month rate of-6.6%, down 1 percentage point, according to SMM data. This week, the total inventory of hot-rolled coils was 4.7695 million tons,-4.91% month-on-month, + 61.19% year-on-year. Building materials national inventory continued to decline this week, year-on-year growth narrowed for the second consecutive week, but the month-on-month slowdown for the first time, mainly due to steel mills inventory slowdown more. In the case of stable release of demand and a small increase in supply, the probability of inventory will continue to decline in the later period, and next week will usher in a small peak of site stock before May Day, and inventory is expected to continue to be stable.

Crude oil rose 7.6% in the previous period. Oil prices recovered further as oil-producing countries such as Kuwait said they would cut production quickly in response to the impact of the outbreak on plummeting global fuel demand. Brent crude oil futures are now up 2.91% to $21.95 a barrel, up 5% on Thursday. Us crude oil futures rose 4.97 per cent to $17.32 a barrel after jumping 20 per cent on Thursday. Unless oil prices rise more sharply in the last trading day of the week, it could be the eighth weekly decline in the past nine weeks.

Close at noon

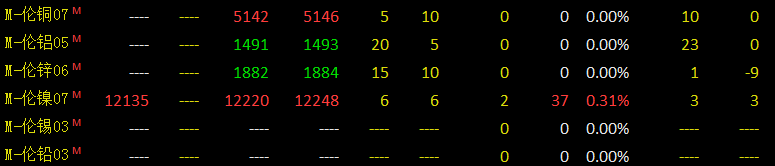

As of 11:30, HKEx had added US dollar-denominated small metal contracts:

Today's stock

Lead: South China lead in Guangdong market is 14130 yuan / ton, the average price of SMM1# lead is 80 yuan / ton. Henan Yuguang, Wanyang, Jinli and other smelters give priority to long orders: Jiang copper 14200 yuan / ton, the average price of SMM net rose 150 yuan / ton; Henan basic pre-sale ended, mainly long orders this week, refineries in other regions maintain high water quotation, the supply of goods in the primary market is still relatively tight, lead ingot inventory is expected to decline slightly this week compared with the previous month.

Zinc: Shanghai Zinc mainstream transaction in 15920-16000 yuan / ton, Shuangyan transaction in 15970-16020 yuan / ton; Shuangyan generally quoted 160-170 yuan / ton in May; Shuangyan reported 180-220 yuan / ton in May; Zinc mainstream transaction in 15850-15920 yuan / ton. Shanghai zinc 2005 contract shock upward, the morning market closed at 15835 yuan / ton. Smelter normal shipment, within the month long single entered the final stage, the market trading activity was lower than yesterday, the domestic market quoted water 170180 yuan / ton, high price transaction difficulty, Shuangyan due to tight circulation quotation is on the high side, reported to the rising water 210 yuan / ton also has the transaction. Enter the second trading period, the market quotation down about 10 yuan / ton, will Ze Xishui 180-190 yuan / ton, Shuangyan quotation to maintain a high level, heard quoted to the rising water 240 yuan / ton, near the weekend, downstream into the market slightly inquiry procurement for the weekend to prepare, the overall transaction within the day is generally flat compared with yesterday.

The mainstream transaction of zinc ingots in Tianjin market was 16080-17190 yuan / ton, and that of ordinary brands was 16080-16210 yuan / ton. The contract for 2005 rose by 300 yuan / ton to 400 yuan / ton. Compared with Shanghai market, Tianjin market rose from 130 yuan / ton to 190 yuan / ton. Today, Shanghai zinc low open rise, the spot market up discount quotation, the quotation is more unified, the ordinary brand lark newspaper in the 05 contract up 300 yuan / ton, red newspaper in the 05 contract rose 360 yuan / ton, Chihong did not quote today, the high price brand Zijin to the May contract reported 400 yuan / ton near. Today, zinc prices rose at a low level, the spot market rose slightly, and traders shipped fewer goods, indicating that the spot market spot liquidity is relatively tight. Next week, Guangdong zinc ingots will be shipped to Tianjin to superimpose imports of zinc, which will alleviate the pressure of spot shortage; downstream, we still need to buy goods today. On the whole, the transaction today is flat compared with yesterday. The transaction of zinc ingot is near 1603016160 yuan / ton.

"2020 (15th) lead and Zinc Summit

Updating.

SMM "current combination" training class

Registration contact: Lu Qingping, SMM Iron and Steel Division

Tel: 021-51595781 / 187-1777-4590

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)