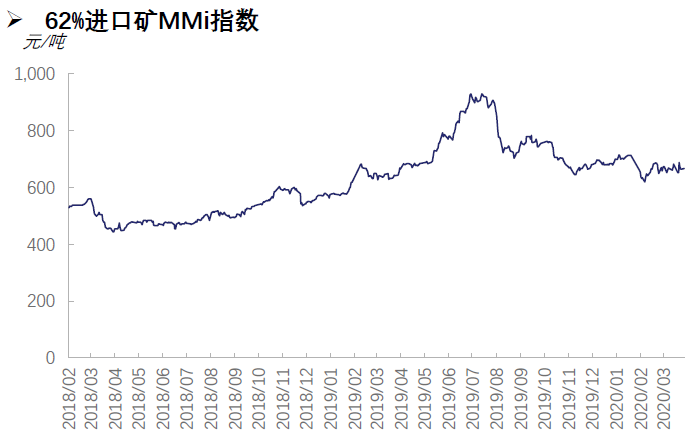

SMM4, March 13: foreign epidemic fermentation in March, economic downside risk increased, while domestic steel mills profit expansion, supply first recovery. But demand recovered less than expected, and inventories remained high. Iron ore in March due to the epidemic, domestic ore supply is still limited, so the overall rise in domestic mine prices; in late March, imported mine prices fell, affected by this, the price of domestic mines in late March is also weak operation.

Thread stocks may rise in April because of continued macro uncertainty, but inventories continue to fall as the marginal impact of peripheral market interference weakens and demand picks up. Hot coil, April supply side reduction and demand side recovery space are limited, fundamental pressure relief is not obvious. Superimposed on the current hot rolling inventory pressure is still large, the spot price is suppressed, so the overall spot price in April is expected to be in a volatile weak trend. On the iron ore side, lump ore and pellet premiums were under pressure in March. In April, with the increase of domestic mine production, the supply of domestic refined powder is expected to rise month-on-month, and the pellet premium is expected to continue to come under pressure.

Selected contents of monthly report

The impact of overseas demand is expected to increase, with imported iron ore prices falling in April

With the gradual improvement of the domestic epidemic situation and the superposition of a series of policies by the government to promote the resumption of work and resumption of production, the performance of the domestic commodity market is relatively strong; however, with the intensification of the overseas epidemic, the collapse of crude oil and the sharp decline in US stocks have a certain bearish impact on the domestic commodity market, and the commodity market in late March has fluctuated downwards. It is expected that the imported mining market may still be under pressure in April.

"Click to view the SMM iron ore database

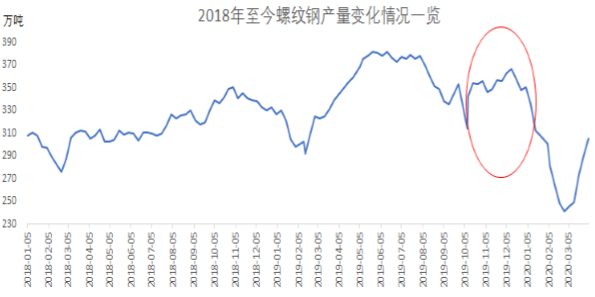

Continuous coding on the supply side-the output of long and short process steel mills has both rebounded

According to the calculation of SMM data model, the profit difference of spiral coil in long process steel plant has been expanding since March. As of April 3, the profit difference of spiral coil has been opened to nearly 300yuan / ton. According to the investigation, the hot coil production of some blast furnace plants has entered a state of small loss. Steel mills are increasingly willing to turn molten iron into thread production. Calculated on the basis of the poor profit of screw coil in 2019 and the similar profit level of EAF steel plant to the current situation (October-November 2019), there is still room for an increase in production of 2 million tons / month (actual increment or less, taking into account the current inventory and financial pressure of the steel mill).

"Click to view the SMM Iron and Steel Industry Database

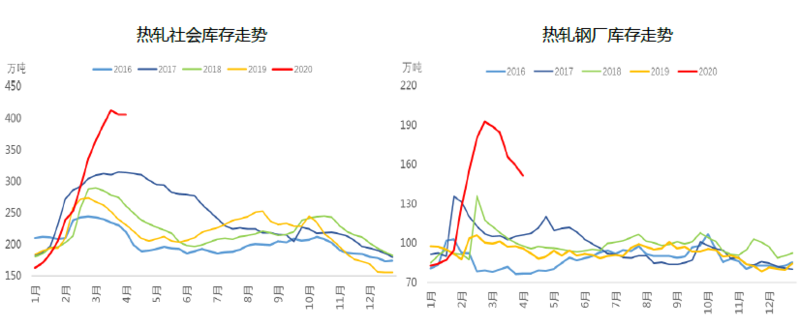

High hot rolling inventory and high market inventory pressure

According to SMM statistics, the current hot rolling inventory is still at a high level in history, the actual market inventory pressure has not been significantly alleviated.

More:

A list of the trend of average spot Price of Thread since 2017

A Survey of the current Price trend of Thread in March

Social inventory of Thread from 2016 to present

A Survey of the trend of Thread Factory Library since 2016

Production cost status of long and short process rebar

Profit status of long and short process rebar production

A list of the trend of profit difference of snail from 2018 to now

Operation rate of Electric Arc Furnace Steel Plant

A Survey of the trend of PMI in Construction Industry

Operating rate of mainstream hot rolling steel mill

Weekly output of hot rolling mainstream steel mill

Trend of profit in hot rolling production

Hot rolling inventory trend

Trend of iron ore MMI62% index

Key data-supply and demand balance sheet for February 2020

Domestic mine price index

Pellet premium and lump ore premium

High-medium-low price difference

Difference between internal and external mineral prices

Difference of mineral price between inside and outside different regions

Maritime BDI index

Public list of domestic Mine Environmental Assessment projects in March 2020

China's iron ore imports

Average daily port volume

Inventory proportion of high, medium and low grade iron ore in six major ports

Influence of blast furnace maintenance on the amount of iron

Cost and profit tracking of Steel Mill

Variation of iron ore base difference

SMM "current combination" training class

Registration contact: Lu Qingping, SMM Iron and Steel Division

Tel: 021-51595781 / 187-1777-4590