Summary of key points:

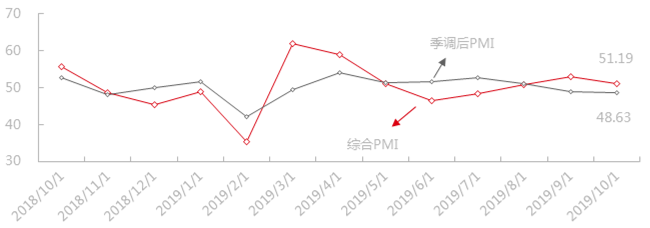

In October 2019, the PMI composite index was 51.19, down 1.69 from a month earlier and 4.57 from a year earlier. After the quarterly adjustment, the composite index was 48.63, down 0.26 from the previous month and 4.75 from the same period last year.

To sum up, this month's PMI composite index before the season before 50, after the season below the 50 withered line, seasonal factors have a significant impact on the downstream industry, in October continued the traditional peak season, to a certain extent to stimulate downstream demand. The overall production situation was better than last month, but the range was limited. This month, the composite production index was 51.68, up 0.19 from the previous month, down 13.35 from the same period last year. With the exception of the construction industry and shipbuilding industry, other industries have increased to varying degrees due to sustained strong demand. The index of new orders was 52.62, down 5.40 from the previous month and 5.06 from a year earlier. With the advent of the traditional peak season, in addition to shipbuilding, new orders in all industries have continued to improve. The shipbuilding industry is mainly focused on completing hand-held orders this year, and new ship orders have dropped significantly compared with the same period last year.

Purchasing Manager Index of downstream Iron and Steel Industry of SMM

PMI Index of Iron and Steel in October:

The PMI composite index for the construction industry was 49.80, down 2.64 from the previous month and 7.19 from a year earlier. After the quarterly adjustment, the composite index was 47.12, down 1.59 from the previous month, down 7.31 from the same period last year. Production and orders in the construction industry fell slightly this month, but remained relatively stable as a whole, maintaining the pace of production during the peak season. Affected by the Expo in Shanghai and the low temperature in the north, the construction progress of a small number of enterprises has slowed down or stagnated. In addition, the impact of financial constraints is particularly severe in the western region, with overall year-on-year tightening evident. The purchase decreases slightly with the construction rhythm, and the overall purchase price decreases month-on-month.

The PMI composite index of the machinery industry was 52.69, up 0.24 from the previous month and 0.09 from the same period last year. After the quarterly adjustment, the composite index rose 51.22, up 1.56 from the previous month and 0.04 from the same period last year. The machinery industry as a whole is slightly better this month than last month, with a small increase in production and new orders. The impact of the trade war tends to ease, and the export business of some enterprises has warmed up. The purchase price is on the low side this month, and the purchase volume is higher than last month.

The PMI composite index of the auto industry was 55.77, down 1.77 from the previous month and 5.74 from the same period last year. After the quarterly adjustment, the composite index was 46.84, up 0.76 from the previous month, down 5.05 from the same period last year. This month, the automobile industry production and marketing situation has improved, new orders increased month-on-month, affected by the peak season, the increase in production is obvious. The corresponding procurement of raw materials also increased month-on-month, superimposed on the low prices of raw materials, led to the growth of raw material stocks. Sales of the industrial chain are relatively smooth, and the inventory of finished products has dropped month-on-month this month. Some companies expect impulse plans by the end of the year, but have been on the sidelines on the rise in production and orders because of the overall malaise in the auto industry this year.

The PMI index of the shipping industry was 47.51, down 5.61 from the previous month and 4.56 from the same period last year. After the quarterly survey, the composite index was 46.93, down 3.81 from the previous month and 4.51 from the same period last year. This month, the shipbuilding industry is mainly based on the production of previous orders, the production rhythm remains unchanged, and the situation of new orders is poor. The business of repairing imported ships has decreased compared with the previous month. The purchasing volume of raw materials fluctuated little this month, and the purchasing price decreased slightly.

The PMI composite index of the home appliance industry was 55.44, down 1.88 from the previous month, up 0.78 from the same period last year. After the quarterly adjustment, the composite index was 52.18, up 1.13 from the previous month and 0.80 from the same period last year. This month, the home appliance industry continued the peak season, superimposed 11 and the end of the year impulse impact, production and new orders increased significantly. Raw material procurement has benefited from a stable and good production rhythm and a substantial increase, sales of finished products are smooth, raw material procurement prices have also pushed up enterprise profits, home appliance enterprises are more optimistic about the follow-up market.

The PMI composite index of transportation infrastructure industry was 53.23, up 1.22 from the previous month, up 1.44 from the same period last year. After the quarterly adjustment, the composite index was 52.93, up 2.47 from the previous month and 1.38 from the same period last year. This month, the transport infrastructure industry as a whole continued to improve, production and new orders continued to increase, some enterprises benefited from government policy support to continue to increase production enthusiasm. Raw material procurement this month was the same as last month, maintaining a high level. The purchase price of raw materials has been reduced.

For more information, please consult Li Tian, Iron and Steel Industry Research Department of SMM

Contact number: + 86-21-51666875