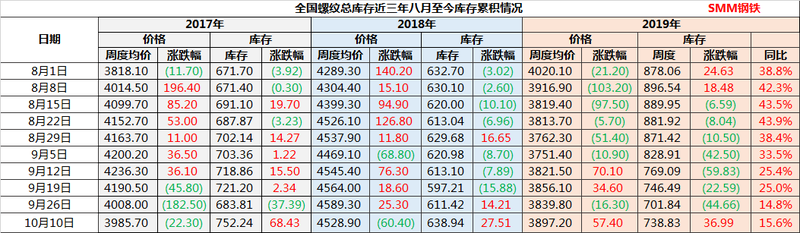

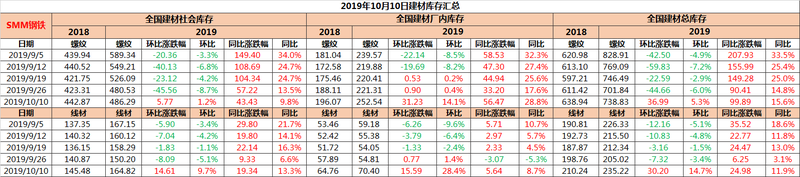

This week, the total thread warehouse of the whole country was 7.3883 million tons, an increase of 369900 tons (+ 5.3 percent) over the week before the festival, and + 15.6 percent from the same period last year. Among them, the factory inventory was 2.5254 million tons, an increase of 312300 tons (+ 14.1 percent) over the week before the festival, and + 28.8 percent compared with the week before the festival. Social inventory was 4.8629 million tons, an increase of 57700 tons (1.2 per cent) over the week before the festival, and + 9.8 per cent from the same period last year. At the end of the 70th anniversary of Daqing, the national thread inventory changed from decrease to increase. There are two reasons, first, the end of production restrictions, superimposed profits rebounded, some areas of steel enterprises re-hot start. Supply pressure could make a comeback. Second, Daqing, the market holiday, terminal access to goods is limited, the speed of demand release is greatly reduced. Combined with the above reasons, thread inventory is expected to increase by three.

Although the social treasury has returned to the trend of accumulation, the demand for the National Day holiday has been blocked, and two days after the festival, the terminal pickup mentality is more cautious because of the expected inventory deviation, and transportation has not yet fully recovered, the increase of 57700 tons is lower than the increase of 195600 tons in the same period last year, exceeding market expectations, showing the tenacity of the demand for building materials. Therefore, demand is still the support. On the supply side, although Daqing environmental protection production restrictions have come to an end, but the bugle of the autumn and winter heating season has slowly sounded, Tangshan yesterday issued an autumn and winter production restriction notice, in addition to three A and B grade steel enterprises, the rest of the steel production limits range from 20% to 55%. In the aspect of short process, the scrap resources are tight, the profit situation is still not ideal, and the power to resume production is insufficient. As a result, the supply side has not yet returned to the peak of full production.

To sum up, demand in the peak season, supply is still restrained, the next two weeks fundamentals may still be better, thread spot short-term or show a strong shock trend. It should be noted that China and the United States will hold consultations again today and tomorrow, and the concrete results will once again affect the market mentality.