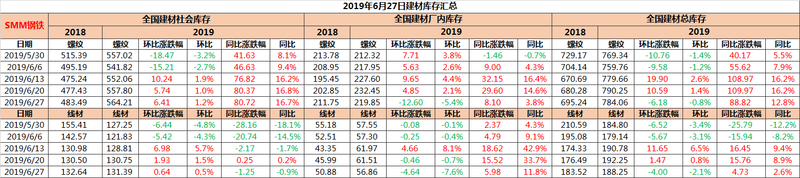

In terms of total inventory:

Total thread stocks this week were 7.8406 million tons, down 61800 tons from last week, down 0.8 per cent from the previous month and up 888200 tons from the same period last year, up 12.8 per cent from the same period last year.

In terms of social inventory:

This week, the screw thread stock was 5.6421 million tons, up 64100 tons from last week, up 1.2 percent from the previous month, and up 807200 tons from the same period last year, up 16.7 percent from the same period last year.

In terms of in-plant inventory:

Inventories at the plant this week were 2.1985 million tons, down 126000 tons from last week, down 5.4 percent from the previous month, and up 81000 tons from the same period last year, or 3.8 per cent from the same period last year.

This week, the general treasury returned to the downward trend, down 61800 tons, with the decline of the factory warehouse as the main factor. The reduction in the supply of steel mills is partly due to the decline in the output of some steel mills in Tangshan since June 24, which began to implement the production restriction policy, and the other is that the electric arc furnace plants, which have cut production due to losses, are still on the verge of profit and loss despite the rise in spot prices. As a result, the electric arc furnace plants, which had previously reduced production due to losses, still have no plans to resume production. On the market demand side, as soon as the production restriction news came out this week, spot prices soared by 50 to 100 yuan per ton on Monday, and the mentality of "whether to buy up or not to buy down" led to an upsurge of enthusiasm for taking goods in the market. Terminal demand returned to calmness in recent days after an explosion on Monday. Speculative trade contributed to most of the transactions this week, in the face of the rising trend of spot traders began to replenish a large number of hoarding goods, East China today appeared limited shipments. In the case of increased willingness to supply miniaturized procurement, inventory in the factory reversed the cumulative trend by 5.4% this week, resulting in a small increase in social inventory of 64100 tons, and the fundamentals have improved.

Spot market:

Spot prices rose 10 to 30 yuan per ton today, while the Hangzhou market rose 70 yuan per ton. The whole day transaction situation is better than yesterday, the local market takes the goods enthusiasm to increase in the morning, tends to calm down in the afternoon. The deal was obviously better in the morning than in the afternoon. As the main producing area of thread in Jiangsu, the issuance of environmental protection documents has enhanced the wait-and-see mentality of the market.

Hangzhou market: today's spot rose 70 yuan / ton, in the morning with futures rose 50 yuan / ton, Shagang quoted price of 4050 yuan / ton, the morning trading situation is better, the afternoon price continues to rise 20 yuan / ton, but the afternoon transaction is tired. On the whole, the deal is good.

Beijing market: today's spot rose 20 yuan / ton, the market transaction situation is OK.

Shanghai market: today a total of 30 yuan / ton, Shagang quoted price of 3980 yuan / ton. The whole day transaction is good, the market takes the goods actively, some traders limited shipment.

Guangzhou market: spot rose 30 yuan / ton today, cold steel quotation 4090 yuan / ton. With the rise of futures in the morning, the mentality of taking goods has increased compared with a few days ago, and tends to be dull in the afternoon. Throughout the day, the deal was mediocre.