SMM4, April 3: from April 2 to 3, 2019, at the "2019 SMM small Metals Industry Summit" hosted by SMM, Hu Yan, senior analyst of SMM small metals, made a comprehensive interpretation of the theme of "2019 China indium germanium gallium market analysis and forecast".

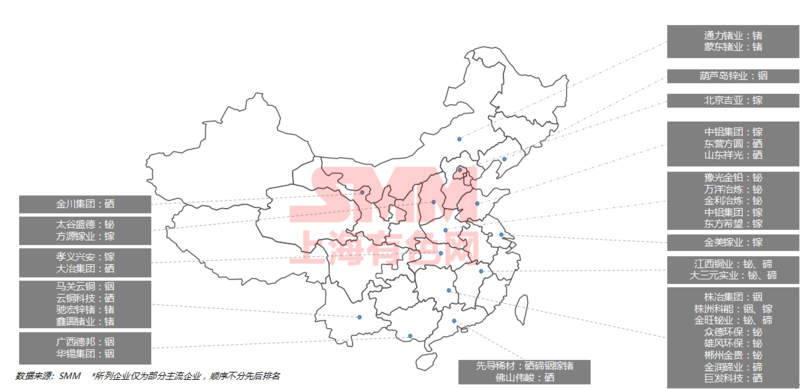

Through the investigation, SMM found that the latest situation of small metal production capacity distribution is as follows: at present, there are many small metal smelters in China, and because the market is saturated, there is little new production capacity specially designed for small metals; Because of the steady development of basic metal production, the overall supply of small metals, as associated metals, is still expanding.

Demand trend of main downstream Industries in small Metal Industry in 2019

In terms of downstream consumption, SMM gives a general outlook for several important downstream areas. The first is the electronics industry, many of which are fast-growing high-tech enterprises with consumer demand for indium gallium germanium.

Semiconductor: semiconductor industry is developing rapidly, which is good for MO source, and increases the consumption of indium and gallium, but the increment is limited.

Optical fiber: the consumption of germanium in optical fiber, driven by the rapid development of 5G, SMM expects optical cable production to grow steadily in 2019.

Solar energy: in all kinds of solar cells, crystal silicon cells still occupy a dominant position, compound thin film cells have not yet achieved mass production in China. For the copper indium gallium selenium battery, the following will do a special analysis.

Display: the screen size of TV and display is developing in the direction of larger area, and the demand for ITO target material is growing strongly. However, there are some technical bottlenecks in the domestic market, and the potential for increasing demand for gallium in 2019 mainly lies in the export market.

In addition, the rapid development of 5G has also opened up a new application field for our small metals. In September, Shanghai Hongqiao Railway Station will become the first 5G railway station in the world, with full coverage of the 5G network. In the 5G tuyere, it is bound to pull our indium gallium germanium small metal consumer demand. The future has come.

2019 Forecast of price trend of small metals

The prospect of indium market in 2019: the increase of refined indium supply is greater than that of consumption, and the future price is lack of support. Subject to the pressure of a large number of social inventories and the limited growth of downstream market demand, domestic indium prices all the way down in 2016. At the end of the year, prices rebounded sharply at the beginning of 2017, but then continued to weaken, hovering at the low level as a whole, after a sharp rise in prices at the beginning of 2017, thanks to the combined buying by stockholders, investment speculators and traders at the end of the year. From the end of 2017 to April 2018, due to the reduction of raw material supply, the role of short-term speculative hot money and the recovery of consumer demand, the price of refined indium in China reached a high of 2100 yuan / kg. Subsequently, the downstream of the high price of indium unintentionally received orders, hoarders high cash so that indium prices into the downward channel.

In early 2019, pan-Asian stocks of 30 tons of refined indium were auctioned publicly, making the indium market more sensitive and vulnerable. SMM believes that with the rise of 5G technology, intelligent manufacturing, digital economy and other emerging industries, the demand for indium will maintain steady growth. However, at present, how to release more than 3600 tons of social inventory is the biggest factor affecting the price of indium in China. SMM will also keep an eye on and report on this.

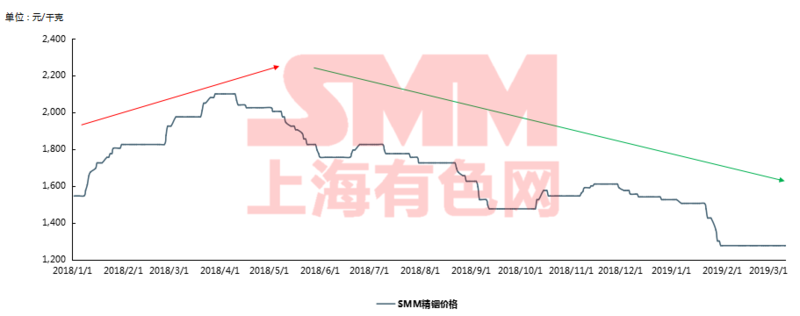

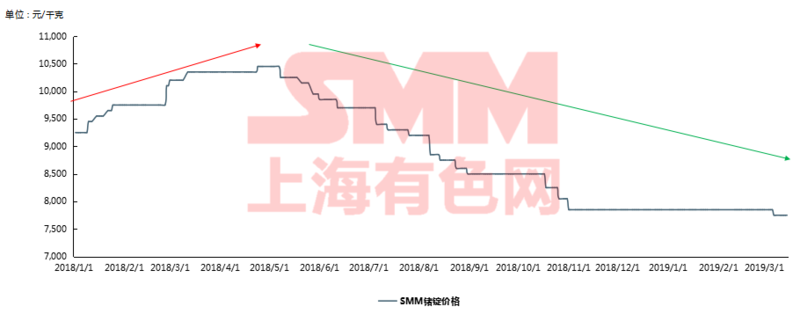

Germanium market outlook for 2019: mainstream enterprises to inventory is still under pressure, prices may continue to be under pressure to hold weak. In 2016, dragged down by demand, the price of domestic germanium ingots fell all the way, falling below the 6000 yuan / kg level in September. Subsequently, the price fell below the cost line to increase the intensity of production and sales reduction, and prices began to rebound at the bottom.

In 2017, with the increasingly stringent national environmental protection requirements and the continuous promotion of environmental protection policies, the supply and demand situation of the industry has been improved, and the price of germanium has gradually rebounded. Coupled with the increase in orders for overseas germanium ornaments in the fourth quarter, the active purchase and hoarding of goods downstream and the supply and sale of upstream supplies have pushed prices all the way up, hitting a high of 10500 yuan / kg in April 2018. Subsequently, due to the contraction of the export market, hoarders increased their willingness to ship, coupled with the successful restructuring of domestic mainstream enterprises to inventory operation, so that the market turned. SMM believes that the supply of germanium ingots will remain stable in 2019, the signs of a substantial increase in consumption are not obvious, and germanium prices are expected to fluctuate over a narrow range.

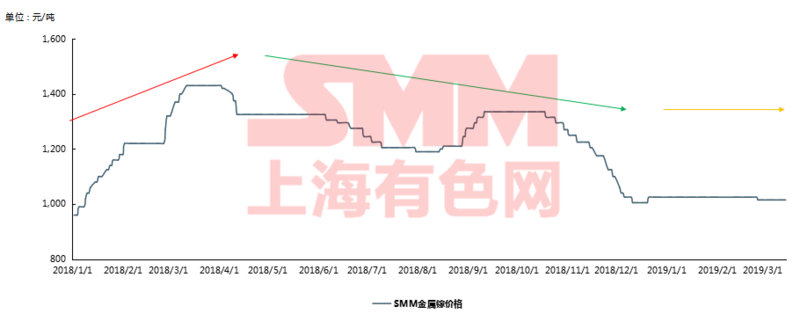

Gallium market outlook for 2019: downstream MO source consumption is strong, supply is not stable, market expected prices are strong. In 2016, the overcapacity gallium market has been depressed since the Fanya event in 2015, with prices fluctuating in a narrow range near the cost line. Under the joint production reduction of production enterprises to save themselves, it began to rebound in the fourth quarter. But with supply still exceeding demand, gallium prices bottomed out again in 2017 after speculators cashed in at a high level.

In the second half of 2017, the market improved, prices rose all the way, and broke through the 1400 yuan / kg mark in April 2018. On the one hand, the growth of downstream MO sources has driven consumption to a large extent, on the other hand, the market in late August came the news that the production of mainstream gallium enterprises will decline, stimulating the market to rise; In addition, the raw material resin is affected by the pressure of environmental protection, and the production is reduced, which leads to the increase of the cost of metal gallium. According to SMM, the growth of domestic gallium market demand in 2019 is limited, but the growth of supply may be higher than the increase of consumption, and the production situation of large factories will directly affect the trend of gallium.

Development expectation of Copper, Indium, Gallium, selenium and cadmium Telluride Market in China from 2019 to 2020

Analysis on the Development potential of Copper, Indium, Gallium, selenium and cadmium Telluride thin Films from 2019 to 2020

The European Union has abolished the "double negative" of photovoltaic against China, and China's solar thin film cell industry has ushered in new opportunities. The 13th five-year Plan for Electric Power Development issued by the National Development and Reform Commission and the National Energy Administration clearly proposes that distributed photovoltaic power generation should reach an installed capacity of more than 60 million kilowatts during the 13th five-year Plan period. According to the data, by the end of 2015, the cumulative installed capacity of distributed generation in China is only 6.06 million kilowatts. This means that during the 13th five-year Plan period, the size of distributed photovoltaic capacity will increase by at least nine times.

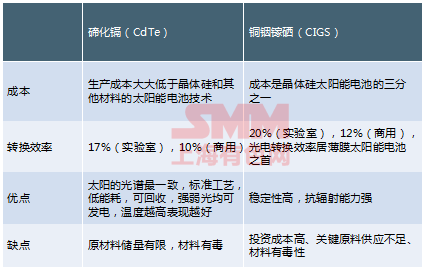

From the point of view of application, thin film solar cells are more suitable for distributed photovoltaic construction such as roof and photovoltaic building integration, and can be attached to the surface of buildings because of their advantages such as light, thin, flexible, variable color and so on. Among all kinds of thin film photovoltaic cells, the conversion efficiency of copper indium gallium selenium (CIGS) thin film cells is the highest, but its development is trapped by high production cost and unstandardized process. Because of its low production cost, stable performance and higher conversion efficiency than silicon-based thin film cells, cadmium telluride (CdTe) thin film photovoltaic cells have high performance-to-price ratio. On August 31, 2018, the European Commission announced that the EU's anti-dumping and countervailing measures against Chinese photovoltaic products would expire on September 3. With the end of the "double negative" sanctions by the European Union, the overseas demand of China's photovoltaic industry is expected to increase, and bring new growth points to the domestic industry.

Comparison of cadmium telluride and copper indium gallium selenium thin film batteries:

Potential new projects of copper, indium, gallium, selenium and cadmium telluride from 2019 to 2020 and prediction of small metal consumption

According to the environmental impact assessment information released on the Internet, a 300 MW copper indium gallium selenium project can consume 4 tons of indium flat targets, 10 tons of copper gallium rotating targets and 15 tons of selenium per year in terms of small metal related raw materials. The small metal content in the target can be calculated according to 75% of indium per ton of indium plane target and 25% of gallium in copper-gallium target. In the next few years, if all the major copper, indium, gallium and selenium projects listed in the table below are put into production, the total power generation will be close to 4GW, which will require 40 tons of indium, 33 tons of gallium and 200 tons of selenium. Taking into account the original volume of the small metal industry, it can be seen that the development of copper indium gallium selenium solar film indium and gallium boost is relatively obvious, can increase the annual domestic consumption by about 10 to 20%, gallium benefit is more obvious. However, the life of photovoltaic thin films is about 10 years, and there will not be additional consumption every year, so in recent years when the new projects are concentrated and put into production, the factors that solar thin films are good for the small metal market can be brought into play.

The sustained and rapid development of distributed generation under the guidance of policy:

Scan QR code, apply to join SMM metal exchange group, please indicate company + name + main business