On the treasury side: the total national inventory is currently 3.4972 million tons, down 4 per cent from last week and 7 per cent from the same period last year (six weeks after the Lunar New year holiday). It is worth noting that hot volume inventories have fallen by 3 per cent this week. Mainly due to the early arrival of resources in the early hot coil steel mill maintenance impact, significantly decreased. Coupled with the fact that demand has been affected by a 3 per cent drop in VAT, the release has been accelerated. Hot coil fundamentals continue to improve, supporting the smooth operation of steel prices.

Factory warehouse: steel plant inventory this week 97.63, down 4% from last week, down 3% from the same period last year (6 weeks after the Lunar New year festival). The factory warehouse is in a state of decline again, and will reach less than 1 million tons.

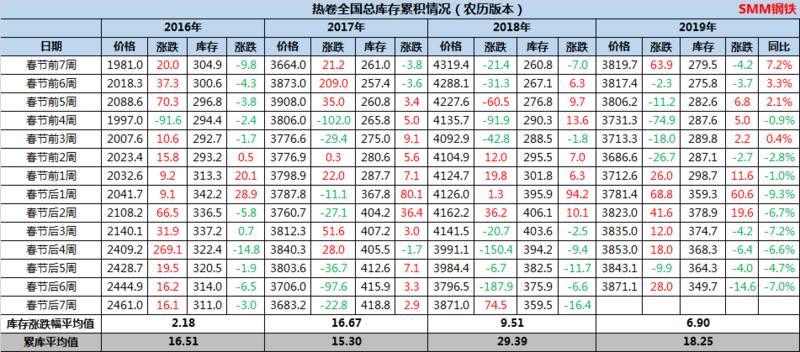

On the price side: last week's average price was 3843, this week's average price was 3871, spot prices fluctuated and rose, and the market was strong before and weak after the weekly performance, which was in line with SMM expectations as a whole [SMM Steel]