SHANGHAI, Aug. 24 (SMM) – China’s copper rod wire sector makes up half of copper semis sector for its largest overcapacity. But, expansion projects of copper rod account the most in copper semi sector in recent years due to low technology requirements, short production cycle, low investment and high production value.

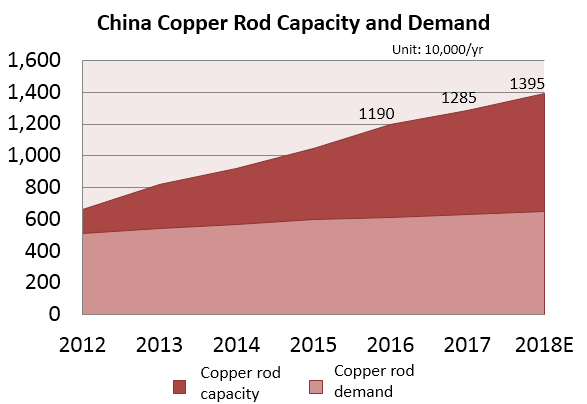

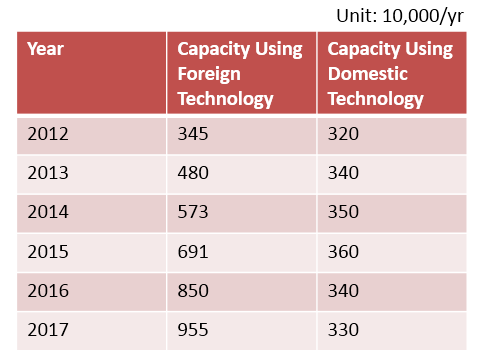

Newly-commissioned copper rod projects in recent years are mainly produced by large foreign equipment. Copper rod capacity reached 12.85 million tonnes in 2017, including 9.55 million tonnes of capacity using foreign production units and 3.3 million tonnes of capacity using domestic equipment. Copper rod capacity rose 6.2 million tonnes during 2012-2017 with compound annual growth rate at 14%. About 1.2 million tonnes of capacity will be commissioned into operation in 2018.

Trading Sees No Significant Improvement on Firm SHFE 1710 Copper, SMM Reports

Copper rod is mainly divided into two kinds, employing domestic and foreign production technologies, respectively, with foreign technologies mainly US’s SCR and Germany’s SMS SIEMAG process. Most medium and large producers produce by foreign continuous casting and rolling equipment, leading to high production efficiency and high quality of goods. Those producers held operating rate at 73% in 2016. Small producers mainly produce by up-draw process, which had low production efficiency. Many small producers closed down due to weak risk resistance capability, and those producers reported low operating rate at 31.7% in 2016. Moreover, proportion of capacity produced by foreign equipment grew to 74% in 2017 from 2012’s 51.8%, and will keep rising.

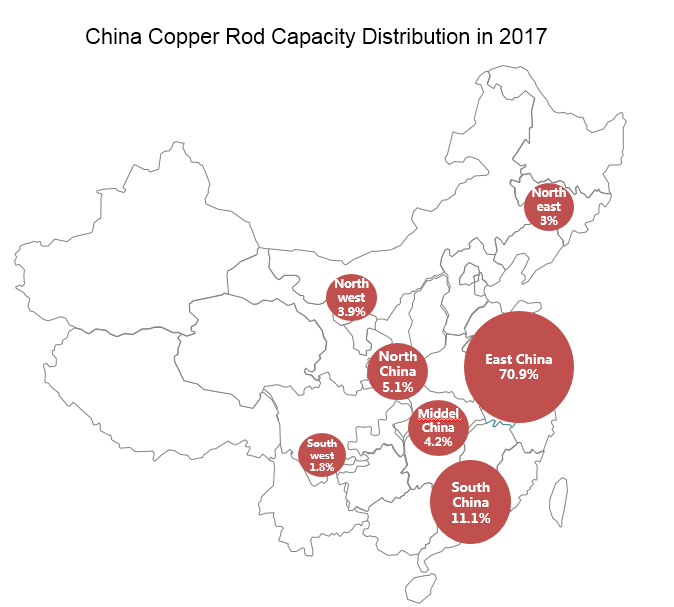

Copper rod industry has high industrial concentration, with capacity at top 20 producers accounting for 53%, and capacity in east China occupies 70.9%. However, it should be noted that rod producers are likely to expanded capacities in west China, which had rich copper ore resources, in order to reduce costs.

China’s copper rod sector is facing industrial shuffle. Many producers are suffering losses due to cutthroat competition, and processing fees have dropped to 500-700 yuan per tonne so far. Producers, with low production efficiency, high cost and weak risk resistance capability, are eliminated gradually. However, copper rod market will remain in oversupply within two years, while demand growth will be steady.

For news cooperation, please contact us by email: sallyzhang@smm.cn or service.en@smm.cn