SHANGHAI, Mar. 29 (SMM) – Copper price stopped a long-term decline since 2011 and entered bull market relatively from 2016. But, how long will the rally last? SMM senior analyst Ye Jianhua expects copper price to maintain bull to 2020, according to SMM’s data model. Besides, Ye also analyzed market hot topics and copper price outlook in 2017 from supply and demand.

Ye Jianhua, SMM Senior Copper Analyst

Collections of Stories in Base Metal Market at SMM 2017 Copper&Aluminum Summit

Supply

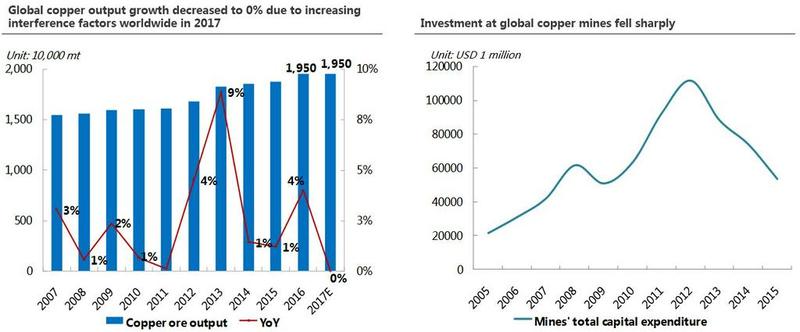

Interference rate at mines increases due largely to benefit redistribution.

After 2017 Chinese New Year holiday, interference rate at mines, heatedly debated, increases due largely to benefit redistribution among investors, workers, mines and government. In the past 5 years, interference rate was not high despite of large decline in copper price. However, there are more and more interference factors at mines after copper price rallies from 2016.

SMM expects global copper ore to increase 700,000-800,000 tonnes (Cu Content) in 2017, but the growth will be offset by interference factors, resulting in 0% of growth or negative growth.

Will copper price rise unilaterally due to interference factors at copper mines?

Global mine expenditure has been in falling territory since 2012. Global copper ore supply is higher than expected in 2015 and 2016, coinciding with long-term contract and TCs. SMM learns that no large amounts of global mines will be constructed and produce copper ores after 2018. Will copper price keep rising as zinc price with falling copper ore output? However, it is hard for copper price to rise unilaterally due to large supply elasticity. Replacement of copper rod by copper scrap rod increased sharply after 2017 Chinese New Year holiday. So, scrap copper will be the major factor on supply elasticity.

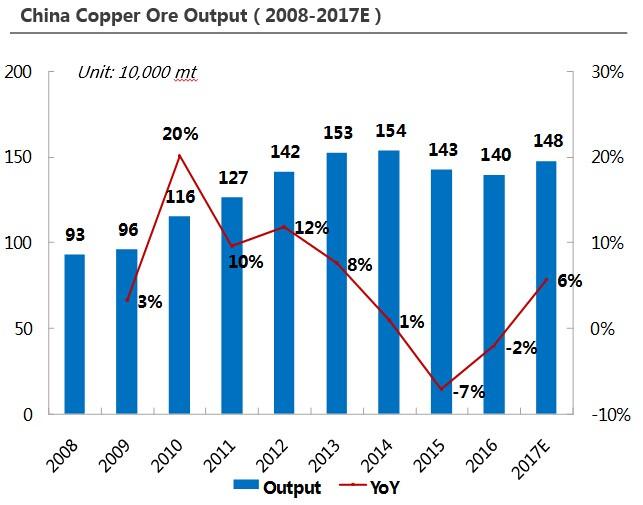

SMM expects China’s copper ore output to increase.

According to SMM’s statistics, China’s copper ore supply will reverse to increase after a 2-year decline, despite of a falling growth in global copper ore supply. China will produce 80,000 tonnes (Cu Content) of copper ore in 2017 with growth at 6%. About 50,000 tonnes will be from newly expanded mines and 30,000 tonnes will from restarted mines.

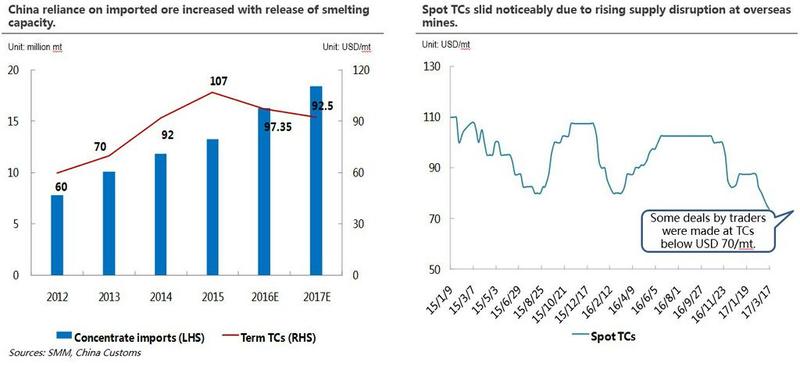

China will increase imports of copper raw materials.

Copper ore output is 1.4 million tonnes (Cu Content) per year in China and most raw material supply relies on import. Moreover, large amounts of smelting capacities will be constructed. Hence, China will increase its dependence on imported raw materials.

The government encourages large SOEs to buy overseas mines to increase raw material supply in China.

With rising interference rate, spot copper concentrate has traded below $ 70 per tonne from 2017 Chinese New Year holiday to the week ending Mar. 17. SMM learned from copper smelters that decline of TCs is limited as if it drops below $ 65 per tonne, profits at copper smelters will reverse to losses. Besides, strikes at overseas mines and output suspension ease.

Will domestic copper smelters cut output with falling ore supply?

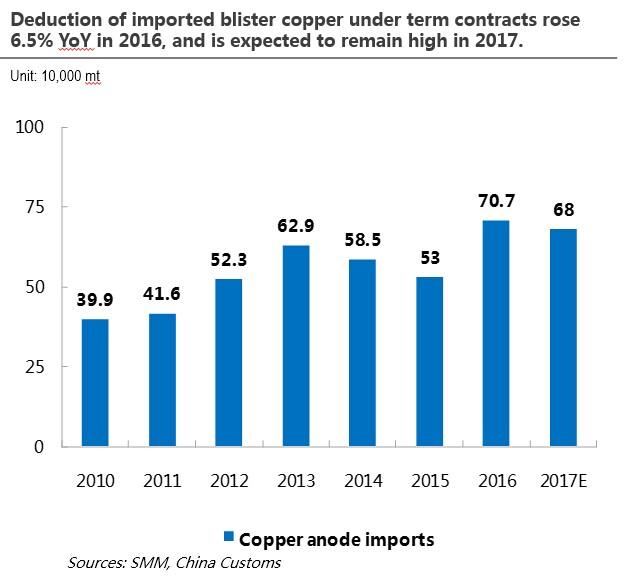

Ye said that copper smelters will not cut output as processing fees of intermedium products, such as crude copper and anode plate/sheet, stay firm at 1,400-1,500 yuan per tonne. Moreover, processing fees of crude copper under long-term contracts are rising in 2017. To sum up, copper smelters will not slash output with tightening ore supply as long as intermedium products prices stay firm.

According to SMM’s statistics, output at domestic copper smelters will reduce 100,000-110,000 tonnes (Cu Content) due to maintenance in the first half of 2017, which will be flat at 2016’s level and little lower than 2015’s level at 130,000-140,000 tonnes. No copper smelters are heard to cut output or close down due to insufficient ore supply yet.

Copper scrap will increase copper supply elasticity.

Copper scrap supply will increase gradually in China with initiative of recycling period. Copper scrap supply was higher than imports in 2016 and rose significantly in China’s market as price gap between copper cathode and copper scrap widened after copper price advanced sharply. So, copper scrap supply elasticity will be large.

SMM expects China’s copper cathode output growth to reduce in 2017.

SMM expects China’s copper cathode output to increase 3.1% YoY to 8 million tonnes in 2017 with growth down on a yearly basis. There were only 3 copper smelters put newly capacity into operation in 2016 and most newly constructed copper smelters, starting construction in the second half of 2017, will not bring plenty amounts of newly output within the year. This, combined with large base, China’s copper cathode output growth will drop in 2017.

According to SMM’s statistics, China’s crude copper and copper cathode output will increase 7.7 million tonnes and 11.4 million tonnes respectively in 2017. Copper smelters will put a large amount of crude copper and copper cathode in to operation in the year, mainly supported by SOEs and local governments. Those smelters produce goods mainly through copper concentrate, growing China’s dependency on imported copper concentrate.

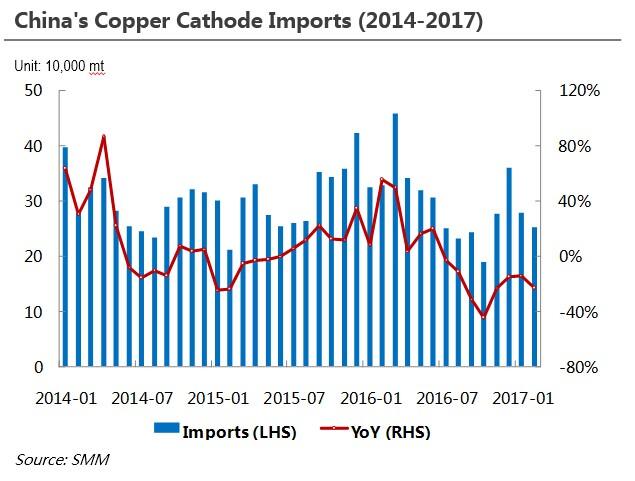

SMM expects China’s imports of copper cathode to drop gradually.

Copper cathode supply is tight in China’s market and 30% of copper cathode is imported. However, SMM expects China’s import of copper cathode to reduce gradually.

Premiums of Yangshan copper declined sharply, down as low as $ 35 per tonne, the low level in recent years, due to large losses of imported copper in 2016, strict inspections and stringent conditions of L/C. This was also one major factor behind decline of copper cathode imports in 2016. In addition, with growth of copper cathode output in China, SMM expects copper cathode import to reduce gradually.

There is a probability for China to export copper cathode in the future.

LME inventory increased sharply for 3 times in 2016 after Chinese copper smelters delivered large amounts of goods into LME Asian inventory. China’s copper cathode export doubled and hit a record high in 2016, on a yearly basis.

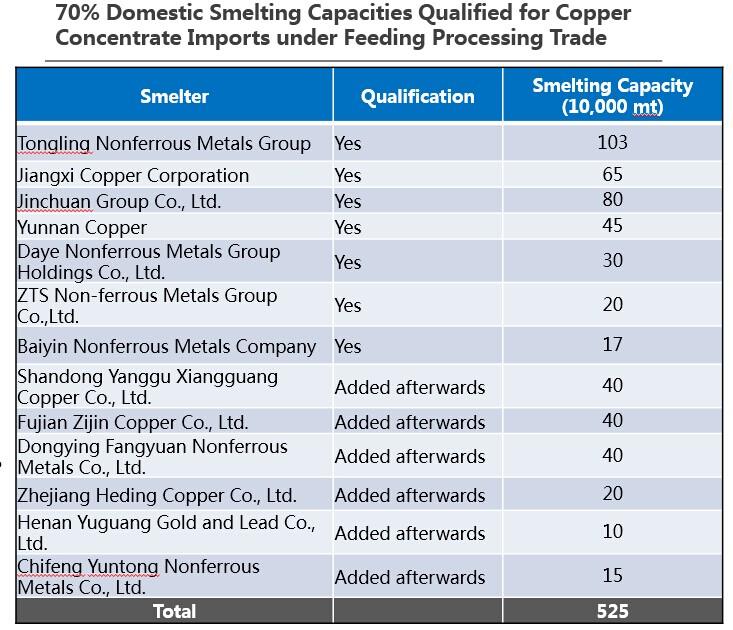

SMM learns that processing capacity of imported copper concentrate accounts for 70% of total crude copper capacity in China at present.

SMM expects copper cathode import to drop further in 2017, and China may be one of copper cathode exporters in the future.

Copper Consumption

Copper consumption at copper processing industry is modest and its peak season is uncertain yet.

SMM survey finds that after the Chinese New Year holiday, orders at copper tube/pipe, and plate/sheet, strip and foil industries recovered rapidly, while those from copper wire rod field were anemic dragged down by power cable & wire consumption, which accounts for 53% of total consumption. Sluggish consumption of power cable & wire slacks market optimistic sentiment.

SMM predicts copper consumption to drop slightly at end-user market in 2017.

According to SMM’s data, China’s copper consumption growth expanded 3.02% from 2015’s 2.7% in 2016, exceeding market expectation, due to all-time auto sales and production, replenishment demand from home appliance industry, rising investment in power industry and improving real estate market. However, SMM predicts copper consumption to reduce slightly to 2.58% in 2017 with worries on real estate, home appliance and power industries.

Copper Inventory

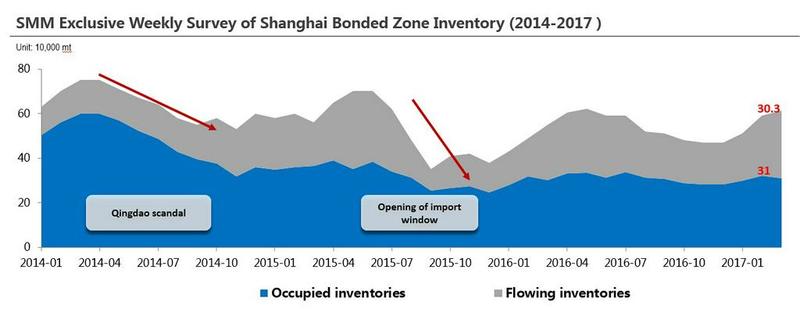

Copper supply will increase with outflow of goods from inventory at bonded area.

Requirements on import finance of copper and carry trade are stricter after fraudulent loan acquisition in Qingdao in 2014 and copper inventory at bonded area flows into market. About 300,000 tonnes of copper from inventory at bonded area will flow into market in the future.

Global visible copper inventory rises significantly.

Global visible copper inventory hits record high at present and invisible inventory is also high. There is no replenishment demand from copper smelters and processing producers so far and most demand is from end-user market, including home appliance and power cable & wire producers, which is lengthening raw material-building period.

Conclusion

Global copper cathode remains oversupply while copper concentrate supply sees a slight deficit. Copper output reduction resulted by strike at Escondida copper mine is higher than expected. Besides, strikes at copper mines in Indonesia and Peru are continuing.

SMM expects copper price to increase at first and then decline in 2017 with highest level at $ 6,400 per tonne in the first half of the year and lowest level at $ 4,800 per tonne in the second half of year. Copper price will mainly fluctuate between $ 5,300-5,400/mt in the whole year. Besides, SMM predicts mainstream of copper price to lurch up gradually before 2020.

For news cooperation, please contact us by email: sallyzhang@smm.cn orservice.en@smm.cn.