- Hot-Rolled Coil Production Rebounded MoM in February

According to SMM data, the average weekly production of domestic hot-rolled coils in February was 3.2004 million mt, up 0.80% MoM from January.

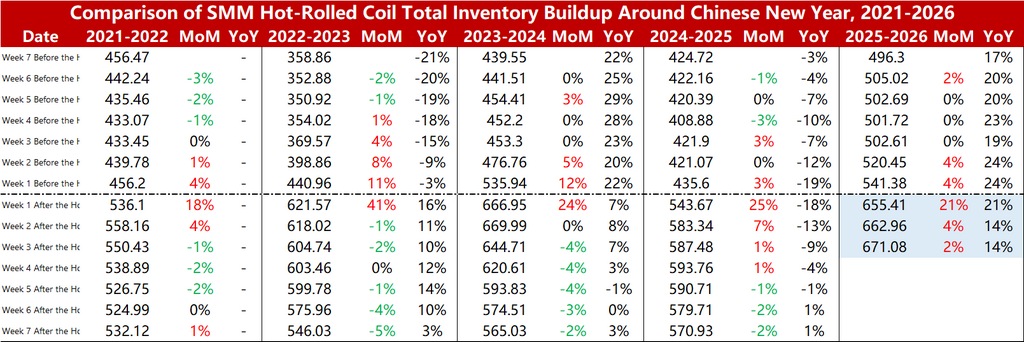

- In the first week after the Chinese New Year, SMM's total hot-rolled coil inventory is expected to accumulate by around 21%.

Post-Chinese New Year, production-wise, according to SMM data, the average hot-rolled coil production in January 2026 was approximately 3.18 million mt, and the average production in February 2026 is expected to rebound by 1%-2% MoM from January. Inventory-wise, from 2022 to 2025, the total inventory buildup in the first week after the Chinese New Year ranged from 20% to 40% WoW compared to the last week before the holiday. It is estimated that in the first week after the 2026 Chinese New Year, the total inventory will increase by around 20%-25% WoW compared to the last week before the holiday, which may be relatively close to last year's buildup level.

However, as the total hot-rolled coil inventory in the last week before the holiday was already 24% higher YoY, the market is expected to continue facing significant pressure after the Chinese New Year.

Overall, SMM estimates that in the first week after the Chinese New Year, the total hot-rolled coil inventory will increase by 1.1–1.2 million mt WoW compared to the last week before the holiday, with the buildup rate close to that of the same period last year, though the absolute buildup value is slightly higher than last year. The average apparent consumption of SMM hot-rolled coil in February is estimated to be around 2.8–2.9 million mt, lower than the same period in 2025, but the lowest point of apparent consumption is basically flat compared to 2025. Attention should be paid to whether post-holiday inventory accumulation exceeds expectations—if the buildup is significant, pressure on hot-rolled coil price trends will intensify after the holiday.

![In the Short Term, Ferrous Metals May Still Struggle to See a Sustained Trend [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![[Domestic Iron Ore Brief Commentary] Domestic Iron Ore Prices May Have Some Room to Rise Next Week](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)