Latest data released by the China Association of Automobile Manufacturers (CAAM) shows that China’s fuel cell vehicle (FCV) market posted a distinct pattern of “strong start followed by a steep decline, with both supply and demand contracting” in the first half of 2026. After a rush of deliveries at the end of 2025, production and sales volumes slumped sharply in H1, sending the industry into a phase of profound adjustment. Beneath the disappointing headline figures, however, this cooling-off period marks a pivotal turning point for the sector to deflate speculative bubbles and solidify its fundamentals.

I. H1 Production & Sales Data: Multiple Signals Behind the Sharp Downturn

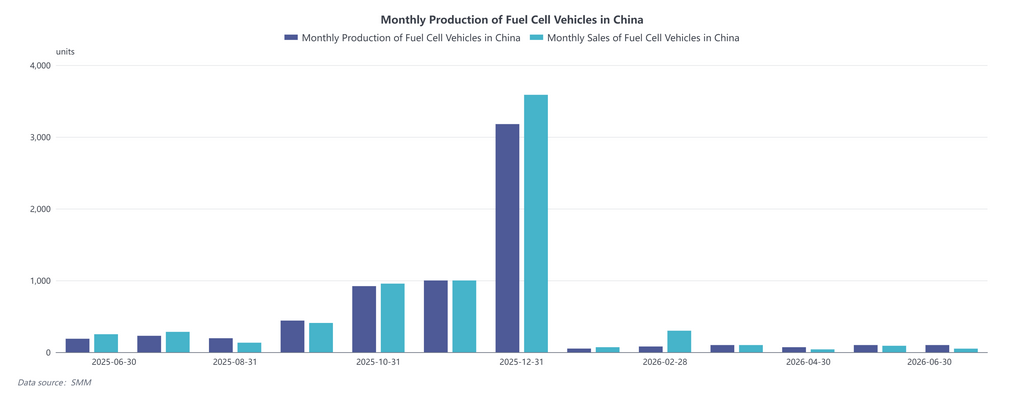

Plunging Overall Volumes: A Grim Market Reality

- Production: Cumulative output from January to June 2026 stood at only 401 units, averaging fewer than 70 units per month, representing a precipitous 71.8% year-on-year drop from H1 2025 — nearly a three-quarters decline.

- Sales: Total sales reached 550 units, falling 63.5% year-on-year. The once sky-high growth trajectory has stalled abruptly, with market sentiment cooling markedly.

Monthly Volatility: Wildly Contrasting Market Dynamics

- Rock-bottom start in January: Production and sales hit a trough, weighed down by the Spring Festival holiday and widespread market wait-and-see sentiment.

- Anomalous rebound in February: Sales surged to 300 units, nearly four times the month’s production. This surge was likely driven by concentrated deliveries of backlogged orders carried over from late 2025 or bulk purchases by major regional corporate clients, creating a false impression of robust demand.

- Prolonged slump from March to June: Both production and sales retreated to sub-100-unit monthly ranges. June saw output hold steady at 100 units, while sales dwindled to merely 50 units, building up mounting inventory pressure.

Year-on-Year Disparity: Double Headwinds of High Comparative Base and Policy Void

The late half of 2025, particularly Q4, saw monthly production and sales exceed 3,000 units at peak frenzy, creating an inflated comparative base for 2026. Compounding this headwind, subsidy incentives have been phased down, while detailed implementation rules for the new round of demonstration city cluster evaluations remain unclarified. Manufacturers have adopted conservative production schedules, and end-users have held off purchases pending new supportive policies, locking the market in a policy-driven stalemate.

II. Industry Growing Pains: Concentration of Structural Bottlenecks

Misalignment between Policy Cycles and Local Fiscal Timelines

The fuel cell vehicle sector remains heavily reliant on policy financial support. The year-end rush to claim subsidies in 2025 drained short-term demand. In 2026, local governments have slowed the disbursement of subsidy funds. Manufacturers hesitate to ramp up production, while buyers delay purchases in anticipation of updated policy frameworks, trapping the market in a standoff.

Lagging Hydrogen Refueling Infrastructure Restricts Overall Expansion

Vehicle technologies have matured considerably, yet the rollout of hydrogen refueling stations has failed to keep pace with market demand. The February sales spike was largely confined to designated demonstration cities, creating isolated hotspots. Regions outside these pilot zones face limited refueling access, stifling wider adoption and fragmenting the national market geographically.

Seasonal and One-off Distortions

The Spring Festival holiday suppressed manufacturing output in January and February, yet February’s counterintuitive sales surge underscores that short-term market performance is dominated by irregular factors such as ad-hoc bulk corporate orders. The subsequent months’ return to subdued volumes reveals a lack of sustained organic market demand.

Cost and Operational Economic Viability Crunch

Slower-than-expected cost reductions for fuel cell systems, paired with volatile hydrogen fuel prices, weigh heavily on commercial fleet operators highly sensitive to running costs. Weak economic returns have dampened corporate purchasing appetite and constrained demand growth.

III. H2 2026 Outlook: The Downturn Nears Its End, Recovery on the Horizon

Based on weak H1 performance and historical market patterns, the second half is projected to follow a trajectory of “muted early months followed by mild recovery”

- Q3: A lull phase focused on inventory destocking and policy waiting: Monthly production and sales are expected to hover between 100 and 200 units, as manufacturers hold back output pending formal policy rollouts or new demonstration project launches.

- Q4: Restorative rebound amid traditional peak season and policy windows: While volumes will unlikely match the late 2025 monthly peak of 3,000 units, monthly output and sales are highly likely to recover to a range of 500–1,000 units, reigniting industry growth momentum.

SMM’s analysis concludes that the bleak H1 2026 data represents an inevitable rationalization phase for the industry to move past speculative overheating. Once speculative bubbles are squeezed out, genuine competitiveness will be rooted in technological upgrades, expanded hydrogen infrastructure and optimized real-world commercial deployment. In H2, as supportive policy frameworks take shape and infrastructure gaps narrow, the market is set to stabilize by late Q3, with tangible recovery emerging in the fourth quarter.

![[SMM Analysis] China's Fuel Cell Vehicle H1 2026 Production and Sales Review and H2 Outlook](https://imgqn.smm.cn/usercenter/mpqgn20251217171727.jpg)

![[SMM survey] Hydrogen Energy Weekly Electrolyzer Industry Review, 20260710-0716](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)

![[SMM Survey] Weekly Review of the Hydrogen Energy Electrolyzer Industry, Jul 3-9, 2026](https://imgqn.smm.cn/usercenter/fblvS20251217171729.png)