According to SMM data, during the week of March 9–13, 2026, China’s stainless steel market moved into the middle phase of the traditional peak-demand season known as “Golden March,” while trading in the most-active stainless steel futures contract rolled smoothly into SS2605. Against a backdrop of escalating geopolitical tensions and a visible turn in inventory trends, stainless steel futures continued to trade at relatively elevated levels. As of 10:15 a.m. on March 13, the contract stood at RMB 14,275/mt (about USD 2,068/mt), up RMB 40/mt (about USD 5.80/mt) from the previous Friday’s close.

This week’s key market tension remained the mismatch between rising supply and only a modest recovery in demand. Although fundamentals have yet to show strong upward momentum, geopolitical risk premiums and persistently high raw material costs have kept downside pressure limited, preventing a broader correction from taking shape.

Macro backdrop: geopolitics abroad, policy support in China

At the macro level, external black swan risks and policy support in China have created a clear contrast. Iran reiterated that it would maintain the effective closure of the Strait of Hormuz, reinforcing safe-haven demand and pushing the US dollar index higher. That, in turn, capped upside in dollar-denominated base metals. Meanwhile, US core CPI rose 2.5% year on year in February, in line with expectations, easing immediate inflation concerns. Even so, the market remains wary of a potential surge in energy prices in March.

In China, the Ministry of Finance has signaled that fiscal policy in 2026 will remain more proactive, with RMB 100 billion (about USD 14.49 billion) allocated to strengthen coordination between fiscal and financial policy, particularly in support of household consumption and private-sector investment. That measured policy support has helped improve expectations for a broader recovery in commodity demand.

Inventory draw emerges, but spot demand remains cautious

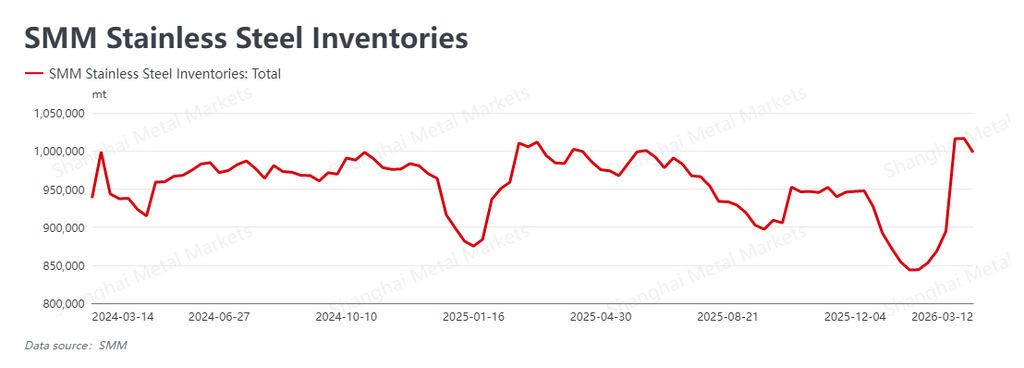

On the fundamentals side, the stainless market has finally reached a meaningful inflection point in destocking, although spot trading still appears underwhelming. The latest SMM data shows that social inventories fell to 998,100 mt this week from 1,016,400 mt the previous week, a decline of 18,300 mt, taking inventories back below the psychologically important 1 million mt threshold.

As downstream processing plants gradually resumed operations, demand continued to recover. However, while spot transactions improved from earlier levels, trading activity still fell short of the strength typically associated with the seasonal peak. End-users have largely remained focused on buying only what they need, with little appetite for active restocking.

At present, the supply increase resulting from concentrated mill restarts in March is meeting only a slow improvement in end-use demand. That still-fragile recovery continues to limit market confidence in any stronger upside breakout during the peak season.

Raw material costs remain the key floor

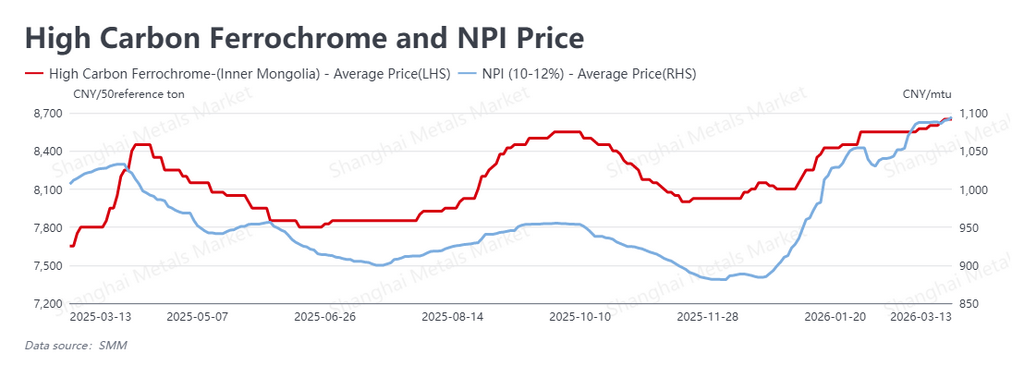

Raw material costs continued to trend higher and remain the market’s main source of downside support. With geopolitical tensions lingering and tight ore supply from Indonesia continuing to feed through the market, upstream quotations kept rising.

As of March 13, high-grade NPI moved up further to RMB 1,094.5 per nickel unit (about USD 158.61 per nickel unit), up RMB 6.5 (about USD 0.94) from a week earlier. High-carbon ferrochrome also climbed to RMB 8,650 per 50-basis mt (about USD 1,253.50 per 50-basis mt).

As raw material prices continue to move higher, stainless mills’ production cost floors are also rising. Although downstream buyers remain resistant to expensive material, room for mills to offer discounts has narrowed sharply under the pressure of high costs and, in some cases, negative margins. As a result, cost support for both futures and spot prices has become increasingly firm.

Outlook: high-level consolidation likely to continue

Overall, the stainless steel market is now caught in a complex tug-of-war defined by rising supply, only a weak recovery in demand, firm cost support, and a clear turn in inventories. The safe-haven and inflation-hedging logic stemming from the Strait of Hormuz crisis, together with NPI prices approaching the 1,100 threshold, has effectively limited downside in the futures market. At the same time, subdued spot order activity has capped upside momentum.

Looking ahead to next week, the market will be watching closely to see whether the destocking trend can continue. The main focus will shift to actual arrivals following mill restarts and the pace at which downstream orders improve. In the near term, the most-active stainless steel futures contract is expected to remain rangebound at relatively high levels. Market participants are advised to closely monitor geopolitical developments and nickel ore price movements, as both could trigger sudden directional swings.

Written by: Bruce Chew | bruce.chew@smm.cn +601167087088

![[SMM Analysis] NPI Prices Rose Sharply, Market Shifted to High-Level Standoff](https://imgqn.smm.cn/usercenter/LNpBh20251217171732.jpeg)