SHANGHAI, Jun 18 (SMM) – This is a roundup of China's metals weekly inventory as of June 18.

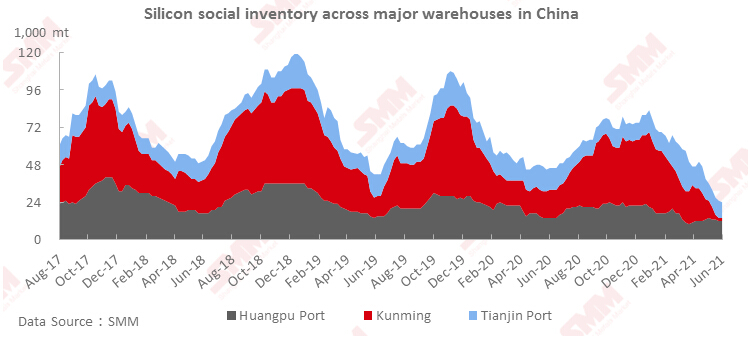

Silicon metal social inventories fell by 1,000 mt on week

Social inventories of silicon metal across Huangpu port, Kunming city and Tianjin port shrank 1,000 mt from the previous week to 24,000 mt as of Friday June 18, hitting a new low.

The inventory at Tianjin port decreased slightly amid rapid receipt and outbound. Operating rates in Yunnan increased markedly after the holiday as the power curtailment was alleviated, but most plants had to ship goods for previous orders, so the silicon metal inventories at plants are hard to increase in the short term. Social inventories of silicon metal are expected to stand stable in the short term.

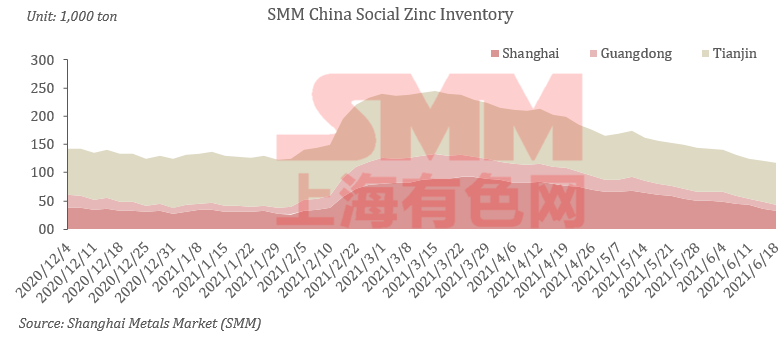

Zinc social inventories shrank 7,500 mt on week

SMM data showed that social inventories of refined zinc ingots across Shanghai, Tianjin, Guangdong, Jiangsu, Zhejiang, Shandong and Hebei decreased 7,500 mt in the week ended June 18 to 128,600 mt. The stocks fell 3,500 mt from Tuesday June 15.

Stocks in Shanghai continued to decrease as arrivals of import zinc fell and the downstream still purchased for rigid demand. In south China's Guangdong, as smelters in Yunnan resumed production one after another, market arrivals increased. Stocks in Tianjin continued to pile up as downstream demand was still weak with normal arrivals at smelters.

Stocks across the three major trading hubs (Shanghai, Tianjin and Guangdong) fell 8,000 mt this week, after a 15,800 mt decrease last week.

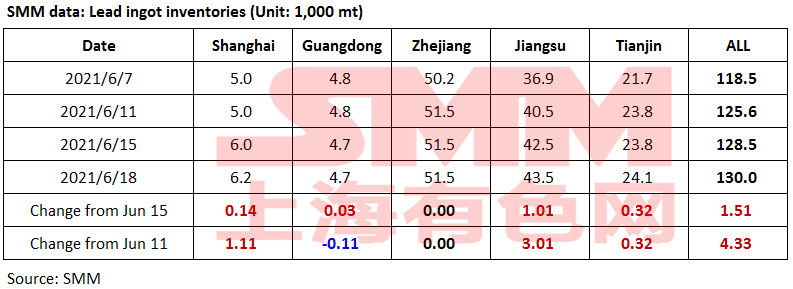

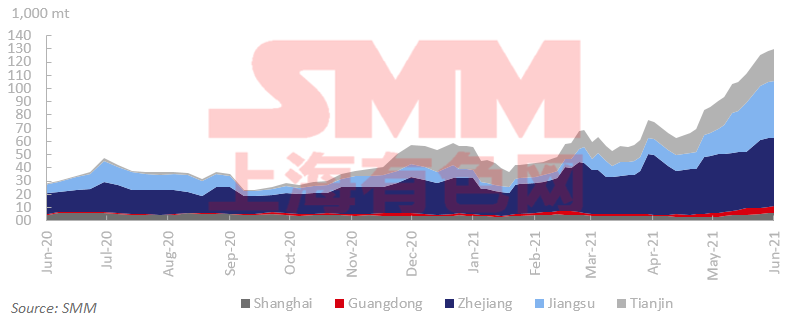

Lead ingot social inventories increased 4,300 mt on week

Social inventories of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin increased 4,300 mt from the prior week and rose 1,500 mt from June 15 to 130,000 mt as of Friday June 18, hitting a record high since March 2015, an SMM survey showed.

Primary lead smelters maintained stable production this week, but downstream consumption was weak, and the users held a wait-and-see stance as lead prices fluctuated at high levels early in the week. The smelters’ deliveries slowed down markedly after the settlement of 2106 lead contract, and some smelters saw increase in inventories, which means that the transferred stocks from lead smelters to social warehouses declined. Therefore, the inventories of lead ingots increased slower amid the low consumption. Lead prices fell to near 15,000 yuan/mt again later this week, approaching the cost line, which suppressed the smelters’ enthusiasm for production. Lead ingot social inventories are expected to increase further slower next week.

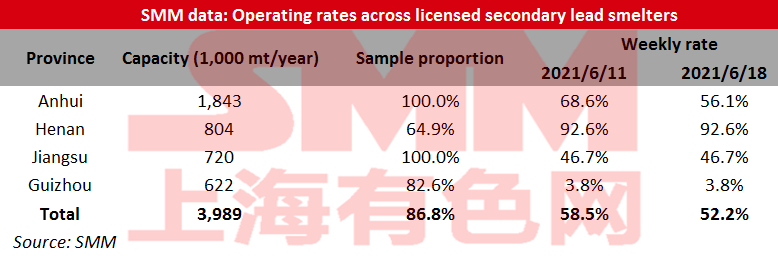

Secondary lead operating rates fell 6.36 percentage points on week

Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 52.16% in the week ended June 18, down 6.36 percentage points from the previous week, showed an SMM survey.

The cost remained high as lead-acid battery prices kept rising, while lead prices fluctuated lower, widening the losses of secondary lead smelters. Spot trade was poor, and finished product inventories were backlogged. Some large-scale smelters conducted maintenance to wait and see the market. Anhui Chilwee continued the maintenance for the second week due to the poor profits amid the busy farming season and less shipments. Tianchang, Jieshou Dadao, Huaxin Xinda and other companies halted production as well. Jiangsu New Chunxing saw decreased output on the week due to the technological transformation. In addition to the sample companies, Hebei Chentai also reduced production because of the low profits. Jieshou Dadao, Huaxin Xinda, and some other large-scale plants will gradually resume production next week, and the output of secondary lead is expected to increase slightly.

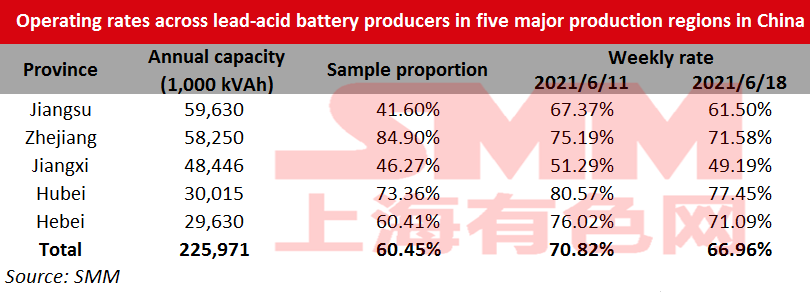

Operating rates of lead-acid battery dropped 3.87 percentage points on week

Operating rates across lead-acid battery producers in Jiangsu, Zhejiang, Jiangxi, Hubei and Hebei provinces lost 3.87 percentage points from June 11 to 66.96% as of Friday June 18.

The market of lead-acid battery remained in the traditional off-peak season, and most companies had reduced production. Many companies took holidays of 1-3 days for the Dragon Boat Festival this week, and the operating rates of lead-acid battery dropped significantly on the week amid fewer working days. The operating rates will recover next week.

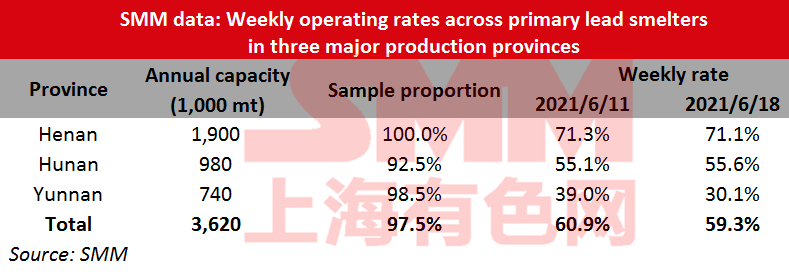

Primary lead operating rates declined 1.55 percentage points on week

Operating rates across primary lead smelters in Henan, Hunan and Yunnan provinces lost 1.55 percentage points from the previous week to 59.3% in the week ended June 18, showed an SMM survey.

Henan Shibin reduced production slightly, and Shuikoushan Jinxin may reduce production next week, both due to the insufficient stocks of raw materials. Shuikoushan Zhihui fully resumed operation this week, and the production was slightly increased. Mengzi Mining and Metallurgy suspended production. Chifeng Shanjin has cut production by over 100 mt/day this week, and will start a maintenance for 20 days from June 20. Jiangxi Copper Group reduced production by 20% this week. Quotations of crude and refined lead stood high as lead prices dropped in the mid-week, and the cost for smelters to stock raw materials was relatively high. The operating rates of refined lead smelters dropped slightly amid insufficient raw materials.

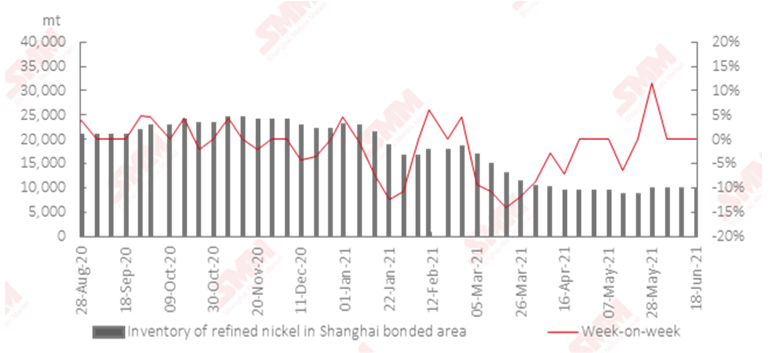

Shanghai bonded refined nickel stocks remained unchanged on week

Inventories of refined nickel in the Shanghai bonded areas remained unchanged from a week ago and stood at 9,700 mt as of June 18, showed SMM data.

The tradable goods in the bonded area were limited, and there were few offers amid tepid trade. Shanghai bonded refined nickel stocks remained flat for the third consecutive week.

Nickel ore inventories at Chinese ports fell 550,000 wmt to 4.96 million wmt

Nickel ore inventories across all Chinese ports decreased 550,000 wmt from June 11 to 4.96 million wmt as of June 18, showed SMM data.

In Ni content, the stocks stood at 39,100 mt.

SMM data also showed that nickel ore stocks across seven major Chinese ports decreased 450,000 wmt during the same period to 3.33 million wmt.

Nickel ore inventories dropped significantly this week, with the total inventory falling below 4 million wmt again. Domestic ferronickel production increased, and the demand for nickel ore was strong. In addition, steel plants' port pick-up was concentrated this week, and inventories dropped a lot. Due to the early bad weather in the Philippines, nickel ore inventories at Chinese ports dropped occasionally recently, while the overall upward trend will remain unchanged in the second and third quarters.

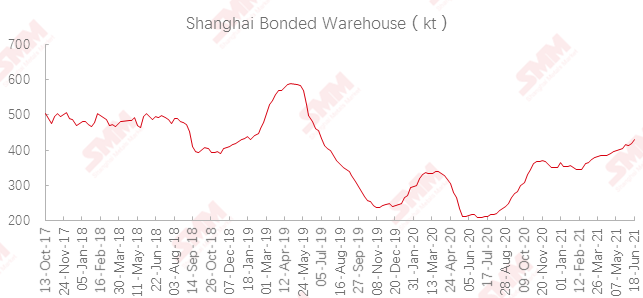

Shanghai bonded copper stocks rose 10,300 mt on week

Stocks of copper in Shanghai bonded areas increased on larger arrivals for the second consecutive week.

SMM data showed that the stocks rose 10,300 mt from the prior week to 429,300 mt as of Friday June 18.

Terms of trade has not been opened up to now. The import losses in the week mostly stood at 600 yuan/mt with sluggish demand for customs declaration. The buying in foreign trade market was very limited, and the inbound goods flowed into the bonded warehouse one after another, which accounted for the continuous increase in stocks.