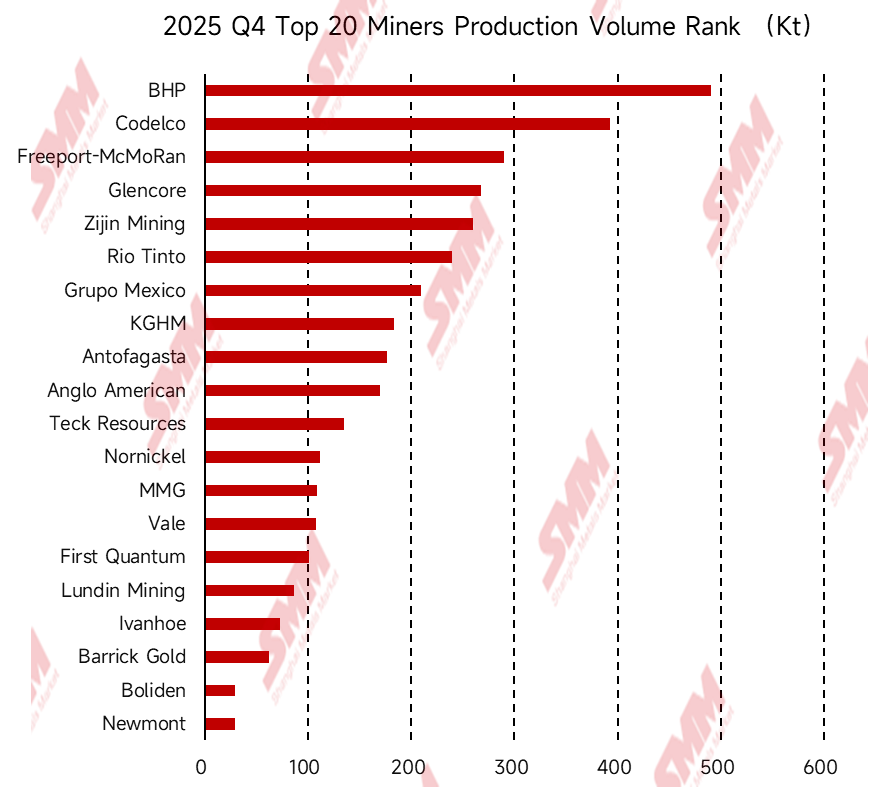

Theo thống kê của SMM, sản lượng đồng của 20 công ty khai thác hàng đầu thế giới trong quý IV/2025 đạt 3.526 kt, tăng 2,1% so với quý trước nhưng giảm 10,5% so với cùng kỳ năm ngoái.

Freeport-McMoRan

Trong quý IV/2025, sản lượng đồng của Freeport-McMoRan là 290,3 kt, giảm 29,8% so với quý trước và giảm 38,5% so với cùng kỳ, chủ yếu do ảnh hưởng của sự cố tràn bùn tại Grasberg vào tháng 9/2025 lên hoạt động của PTFI. Mục tiêu sản lượng đồng năm 2026 của Freeport-McMoRan là 1.361 kt.

Glencore

Trong quý IV/2025, sản lượng đồng của Glencore là 268,1 kt, tăng 11,9% so với quý trước và tăng 8,8% so với cùng kỳ. Nguyên nhân chủ yếu là do cải thiện hàm lượng dự kiến tại KCC, Antamina và Antapaccay. Mục tiêu sản lượng đồng năm 2026 của Glencore là 810-870 kt.

Anglo American

Trong quý IV/2025, sản lượng đồng của Anglo American là 268,1 kt, giảm 7,6% so với quý trước và giảm 14,1% so với cùng kỳ, chủ yếu do hàm lượng đồng thấp hơn tại Quellaveco và Collahuasi. Mục tiêu sản lượng đồng năm 2026 của Anglo American là 700-760 kt.

Rio Tinto

Trong quý IV/2025, sản lượng đồng của Rio Tinto là 240 kt, tăng 17,6% so với quý trước và tăng 5,3% so với cùng kỳ. Nguyên nhân chính là do Kennecott phục hồi sau bảo dưỡng ngừng nhà máy tuyển quặng vào tháng 9 và bảo dưỡng lò luyện 45 ngày trong quý IV. Bên cạnh đó, khối lượng quặng đồng xử lý tăng và hàm lượng cao hơn tại nhà máy tuyển quặng đã thúc đẩy sản lượng đồng của Kennecott. Trong khi đó, Oyu Tolgoi không chỉ phục hồi sau bảo dưỡng nhà máy tuyển quặng tháng 9 mà còn ghi nhận tăng trưởng sản lượng nhờ sản lượng tiếp tục tăng từ mỏ ngầm, cải thiện hàm lượng quặng đầu vào và tỷ lệ thu hồi cao hơn. Mục tiêu sản lượng đồng năm 2026 của Rio Tinto là 455-530 kt.

Teck Resources

Trong quý IV/2025, sản lượng đồng của Teck Resources là 134,9 kt, tăng 29,6% so với quý trước và tăng 10,5% so với cùng kỳ. Nguyên nhân chính là do sản lượng và hàm lượng quặng cao hơn tại mỏ đồng HVC, hàm lượng quặng được cải thiện tại mỏ đồng Antamina, và sản lượng tăng tại mỏ Carmen de Andacollo. Mục tiêu sản xuất đồng của Teck Resources cho năm 2026 là 455-530 kt.

![[Phân tích SMM] Giá đồng LME biến động ở mức cao; hoạt động mua hàng chậm lại trên khắp Trung Quốc, Nhật Bản và Hàn Quốc](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)