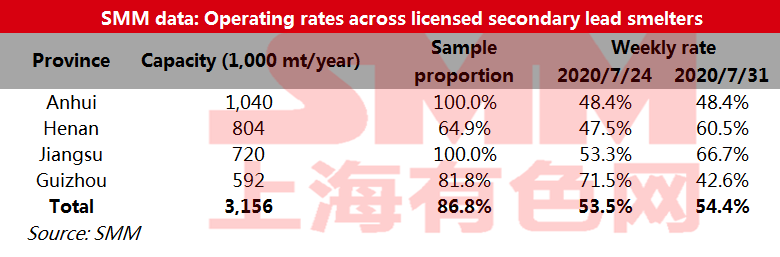

SHANGHAI, Jul 31 (SMM) – Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 54.4% in the week ended July 31, up 0.9 percentage point from the previous week, showed an SMM survey.

The average rate in Henan recovered 13 percentage points to 60.5%, as Henan Jinli commissioned capacity after equipment upgrading. Its demand for paste of lead increased.

The rate in Jiangsu came in at 66.7%, up 13.4 percentage points from a week ago, driven by capacity expansion at New Chunxing.

The average rate in Anhui was unchanged from the previous week at 48.4%, as production equipment at Anhui Dahua remains in debugging and tight supply of battery scrap prevented smelters operations from rising.

Average operating rate in Guizhou plunged 28.9 percentage points from a week ago to 42.6%, as smelters of Jinlong, Yongxin and Sanhe nearly halved their production due to local environmental inspections. Guizhou Cenxiang has not normalised production amid continued maintenance.

An SMM survey found that licensed secondary lead smelters in Anhui hold no inventories of secondary lead bullion as of July 31, with stocks of secondary refined lead of only 600 mt.

![SHFE lead 2607 traded above the daily average line intraday, recording a three-day winning streak [Lead Brief Review]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)

![[SMM Sulfur Flash] Spot Sulfur Transactions Slide, Shandong Refinery Quotes Decline](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)