SMM อัปเดตวันที่ 18 พฤษภาคม:

ตลาดโลหะ:

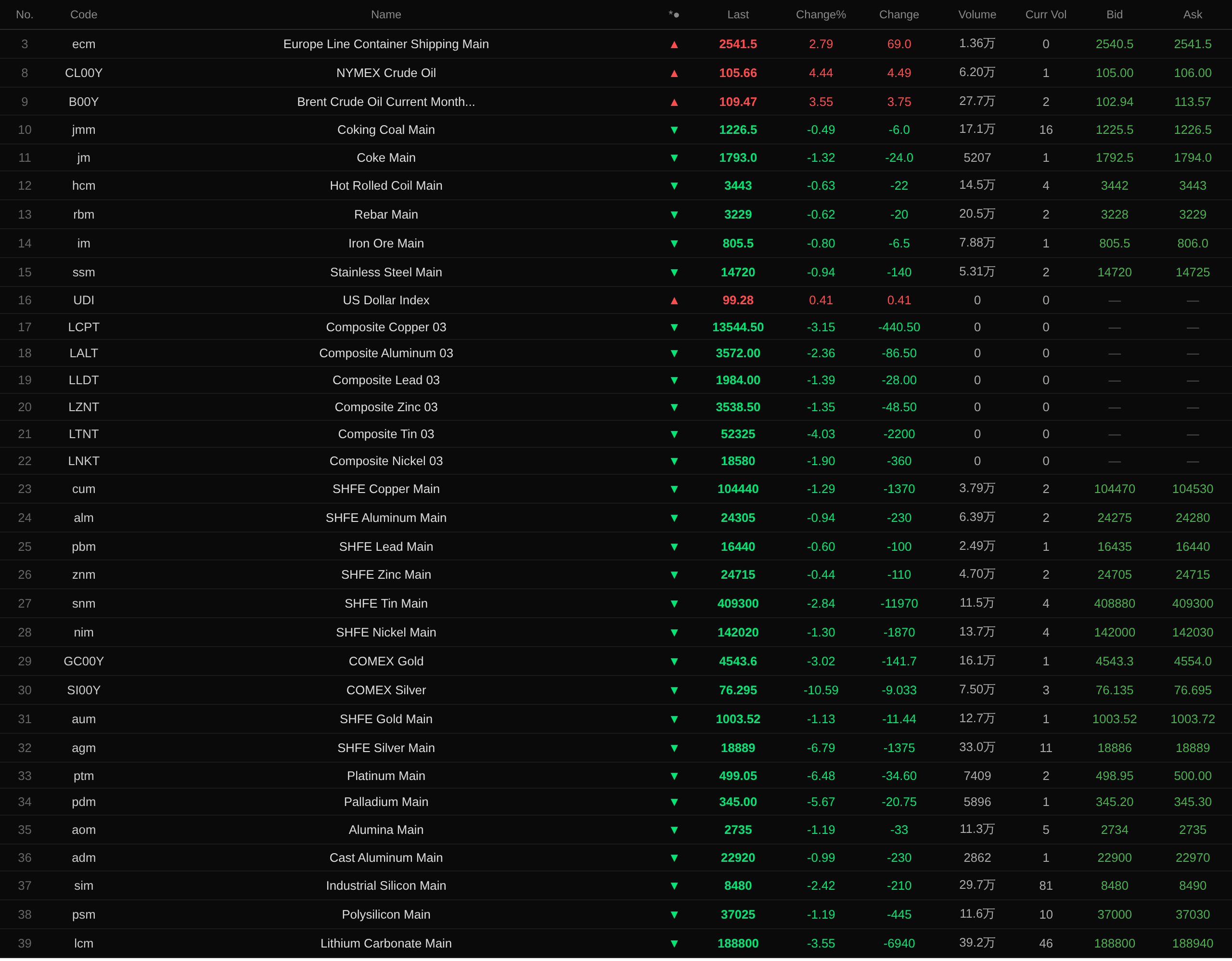

ช่วงซื้อขายข้ามคืนวันศุกร์ที่ผ่านมา ตลาดโลหะทั้งในประเทศและต่างประเทศปรับตัวลงในวงกว้าง โดยส่วนใหญ่ลดลงมากกว่า 1% ดีบุก LME นำการปรับตัวลงที่ 4.03% ทองแดง LME ลดลง 3.15% อะลูมิเนียม LME และดีบุก SHFE ลดลงมากกว่า 2% (อะลูมิเนียม LME -2.36%, ดีบุก SHFE -2.84%) ตะกั่ว LME, สังกะสี LME, นิกเกิล LME, ทองแดง SHFE และนิกเกิล SHFE ลดลงมากกว่า 1% (ตะกั่ว LME -1.39%, สังกะสี LME -1.35%, นิกเกิล LME -1.9%, ทองแดง SHFE -1.29%, นิกเกิล SHFE -1.3%) ตะกั่ว SHFE และสังกะสี SHFE ลดลงน้อยกว่า 1% (ตะกั่ว SHFE -0.6%, สังกะสี SHFE -0.44%) สัญญาเดือนใกล้ของอะลูมินาลดลง 1.19% และสัญญาเดือนใกล้ของอะลูมิเนียมหล่อลดลง 0.99%

ช่วงซื้อขายข้ามคืนวันศุกร์ที่ผ่านมา โลหะกลุ่มเหล็กปรับตัวลงในวงกว้าง สเตนเลสลดลง 0.94% และแร่เหล็กลดลง 0.8% เหล็กแผ่นรีดร้อนและเหล็กเส้นลดลงมากกว่า 0.6% (เหล็กแผ่นรีดร้อน -0.63%, เหล็กเส้น -0.62%) สำหรับถ่านโค้กและโค้ก ถ่านโค้กลดลง 0.49% และโค้กลดลง 1.32%

ช่วงซื้อขายข้ามคืนวันศุกร์ที่ผ่านมาสำหรับโลหะมีค่า: ทองคำ COMEX ลดลง 3.02% ข้ามคืน ลดลง 3.96% ในรอบสัปดาห์ เงิน COMEX ร่วงลง 10.59% ลดลง 5.65% ในรอบสัปดาห์ ในจีน ทองคำ SHFE ลดลง 1.13% ลดลง 3.37% ในรอบสัปดาห์ เงิน SHFE ลดลง 6.79% ลดลง 3.26% ในรอบสัปดาห์ สาเหตุหลักมาจากอัตราผลตอบแทนพันธบัตรสหรัฐฯ ที่ปรับตัวสูงขึ้นและค่าเงินดอลลาร์สหรัฐที่แข็งค่าขึ้นโดยยังไม่มีทีท่าจะคลี่คลาย ขณะที่ความขัดแย้งสหรัฐฯ-อิหร่านเพิ่มความกังวลด้านเงินเฟ้อ ยิ่งตอกย้ำความคาดหวังของตลาดต่อการปรับขึ้นอัตราดอกเบี้ย

ณ เวลา 8:24 น. วันที่ 16 พฤษภาคม ราคาปิดช่วงซื้อขายข้ามคืนวันศุกร์ที่ผ่านมา:

ด้านมหภาค

หวัง อี้ แถลงข่าวต่อสื่อมวลชนเกี่ยวกับการประชุมสุดยอดจีน-สหรัฐฯ และฉันทามติที่บรรลุ หวัง อี้ ระบุว่าผู้นำทั้งสองประเทศหารือกันเกือบ 9 ชั่วโมง และเห็นพ้องว่าการสร้าง "ความสัมพันธ์เชิงสร้างสรรค์เพื่อเสถียรภาพเชิงยุทธศาสตร์จีน-สหรัฐฯ" เป็นฉันทามติทางการเมืองที่สำคัญที่สุด ตามคำเชิญของประธานาธิบดีทรัมป์ ประธานาธิบดีสี จิ้นผิง จะเดินทางเยือนสหรัฐฯ อย่างเป็นทางการในฤดูใบไม้ร่วงนี้ ทีมเศรษฐกิจและการค้าของทั้งสองประเทศบรรลุผลลัพธ์ที่สมดุลและเป็นบวกโดยรวม รวมถึงการดำเนินฉันทามติทั้งหมดจากการเจรจาครั้งก่อนต่อไป เห็นชอบจัดตั้งสภาการค้าและสภาการลงทุน แก้ไขข้อกังวลของแต่ละฝ่ายเกี่ยวกับการเข้าถึงตลาดสินค้าเกษตร และส่งเสริมการขยายการค้าสองทางภายใต้กรอบการลดภาษีตอบแทนซึ่งกันและกัน

จีน:

กระทรวงการต่างประเทศตอบคำถามรวมเกี่ยวกับประเด็นเศรษฐกิจและการค้าจีน-สหรัฐฯ รวมถึงเซมิคอนดักเตอร์ แร่หายาก โบอิ้ง และการจัดซื้อน้ำมันเมื่อวันที่ 15 พฤษภาคม นายกัว เจียคุน โฆษกกระทรวงการต่างประเทศ เป็นประธานการแถลงข่าวประจำและตอบคำถามรวมเกี่ยวกับประเด็นเศรษฐกิจและการค้าจีน-สหรัฐฯ ในเรื่องอุปทานแร่หายาก จีนมุ่งมั่นรักษาเสถียรภาพของห่วงโซ่อุปทานโลก ในเรื่องการจัดซื้อน้ำมันและเครื่องบินโบอิ้งจากสหรัฐฯ จีนแสดงความเต็มใจที่จะร่วมกันรักษาความมั่นคงด้านพลังงานและเสถียรภาพห่วงโซ่อุปทาน โดยเน้นย้ำถึงลักษณะที่เป็นประโยชน์ร่วมกันของความสัมพันธ์ทางเศรษฐกิจและการค้าจีน-สหรัฐฯ

วารสาร "ฉิวซื่อ" ตีพิมพ์บทความสำคัญของเลขาธิการใหญ่สี จิ้นผิง ในหัวข้อ "ทำให้เศรษฐกิจภาคจริงแข็งแกร่งขึ้น ดีขึ้น และใหญ่ขึ้น"บทความชี้ว่าอุตสาหกรรมการผลิตเป็นรากฐานของเศรษฐกิจภาคจริง ควรให้ความสำคัญกับการพัฒนาอุตสาหกรรมการผลิตคุณภาพสูงในตำแหน่งที่โดดเด่นยิ่งขึ้น และยึดมั่นอย่างไม่หวั่นไหวในการสร้างประเทศมหาอำนาจด้านการผลิต เรียกร้องให้ดำเนินโครงการปรับปรุงพื้นฐานอุตสาหกรรมและโครงการบุกเบิกอุปกรณ์เทคนิคสำคัญ สนับสนุนการพัฒนาวิสาหกิจที่มีความเชี่ยวชาญ ประณีต โดดเด่น และนวัตกรรม ส่งเสริมการพัฒนาอุตสาหกรรมการผลิตไปสู่ระดับไฮเอนด์ อัจฉริยะ และเป็นมิตรกับสิ่งแวดล้อม นอกจากนี้ยังเรียกร้องให้ส่งเสริมการพัฒนาแบบบูรณาการเป็นคลัสเตอร์ของอุตสาหกรรมเกิดใหม่เชิงกลยุทธ์ และสร้างเครื่องยนต์การเติบโตใหม่จำนวนหนึ่งในด้านต่างๆ เช่น เทคโนโลยีสารสนเทศยุคใหม่ ปัญญาประดิษฐ์ เทคโนโลยีชีวภาพ พลังงานใหม่ วัสดุใหม่ อุปกรณ์ไฮเอนด์ และการอนุรักษ์สิ่งแวดล้อมสีเขียว

ดอลลาร์สหรัฐ:

ณ ราคาปิดข้ามคืนของวันศุกร์ที่ผ่านมา ดัชนีดอลลาร์สหรัฐเพิ่มขึ้น 0.41% มาอยู่ที่ 99.28 เพิ่มขึ้น 1.45% ในรอบสัปดาห์ ราคาพลังงานที่สูงขึ้นและการหยุดชะงักของการขนส่งทางเรือที่ยืดเยื้อทำให้แรงกดดันเงินเฟ้อรุนแรงขึ้น ผลักดันให้ตลาดคาดการณ์ว่าเฟดจะขึ้นอัตราดอกเบี้ยในปีนี้ ราคาฟิวเจอร์สอัตราดอกเบี้ยสหรัฐฯ ร่วงลงอย่างรุนแรงในวันศุกร์ สะท้อนความเชื่อมั่นที่เพิ่มขึ้นในหมู่นักลงทุนตลาดพันธบัตรว่าเงินเฟ้อที่อยู่ในระดับสูงจะบังคับให้เฟดขึ้นอัตราดอกเบี้ยในช่วงปลายปีนี้หรือต้นปี 2027 ตามเครื่องมือ CME FedWatch ตลาดกำหนดราคาความน่าจะเป็นประมาณ 60% ที่คณะกรรมการกำหนดนโยบายการเงิน (FOMC) จะขึ้นอัตราดอกเบี้ย 25 จุดพื้นฐานภายในการประชุมเดือนมกราคมหน้า โดยมีความน่าจะเป็น 50% ที่จะขึ้นอัตราดอกเบี้ยในเดือนธันวาคม

ยอดค้าปลีกสหรัฐฯ เดือนเมษายนยังคงเติบโตต่อเนื่อง แต่ส่วนหนึ่งของการเพิ่มขึ้นอาจเป็นผลจากอัตราเงินเฟ้อที่สูงขึ้น เนื่องจากความขัดแย้งอิหร่านผลักดันราคาพลังงานและสินค้าโภคภัณฑ์อื่นๆ ให้ปรับตัวสูงขึ้น ข้อมูลที่เผยแพร่เมื่อวันพฤหัสบดีแสดงว่ายอดค้าปลีกเดือนเมษายนเพิ่มขึ้น 0.5% สอดคล้องกับที่ตลาดคาดการณ์ ขณะที่ตัวเลขเดือนมีนาคมถูกปรับลดลงเหลือ 1.6% ความขัดแย้งอิหร่านกำลังผลักดันเงินเฟ้อให้สูงขึ้น ข้อมูลจากสำนักงานสารสนเทศด้านพลังงานสหรัฐฯ แสดงว่าราคาน้ำมันเบนซินเพิ่มขึ้น 12.3% ในเดือนเมษายน แม้ราคาน้ำมันพุ่งสูง แต่การใช้จ่ายของผู้บริโภคยังไม่เปลี่ยนแปลงอย่างเห็นได้ชัดจากด้านอื่นๆ เนื่องจากจำนวนเงินคืนภาษีปีนี้สูงขึ้น ข้อมูลจากกรมสรรพากรสหรัฐฯ (IRS) แสดงว่า ณ วันที่ 25 เมษายน จำนวนเงินคืนภาษีเฉลี่ยเพิ่มขึ้น 323 ดอลลาร์เมื่อเทียบกับช่วงเดียวกันของปี 2025 อย่างไรก็ตาม แรงสนับสนุนนี้กำลังลดลง นักเศรษฐศาสตร์จาก PNC Financial Services Group ระบุว่าจากการวิเคราะห์ข้อมูลภายใน "ผู้บริโภคใช้จ่ายเงินคืนภาษีเร็วกว่าปีที่แล้ว โดยเฉพาะในกลุ่มครัวเรือนรายได้ต่ำ" พร้อมเสริมว่า "จำนวนเงินคืนภาษีที่นำไปชำระหนี้บัตรเครดิตและหนี้อื่นๆ ก็ลดลงเช่นกัน" (Jin10 Data APP)

คณะกรรมการผู้ว่าการเฟดออกแถลงการณ์เมื่อวันศุกร์ว่าได้แต่งตั้งเจอโรม พาวเวลล์เป็นประธานรักษาการจนกว่าผู้สืบทอดตำแหน่ง เควิน วอร์ช จะเข้าสาบานตนอย่างเป็นทางการ เฟดระบุว่า "ขั้นตอนชั่วคราวในการแต่งตั้งประธานคนปัจจุบันเป็นประธานรักษาการนี้ สอดคล้องกับแนวปฏิบัติในการเปลี่ยนผ่านประธานครั้งก่อนๆ" ในการตอบสนองต่อเรื่องนี้ ผู้ว่าการเฟด โบว์แมน และ มิลาน ระบุว่าไม่สนับสนุนการแต่งตั้งรักษาการดังกล่าว เมื่อวันที่ 15 พฤษภาคม วาระการดำรงตำแหน่งประธานเฟดของพาวเวลล์สิ้นสุดลง (Wallstreetcn)

นักวิเคราะห์จาก BofA Global Research: หากการเติบโตทางเศรษฐกิจโลกที่แข็งแกร่งทำให้เฟดไม่สามารถลดอัตราดอกเบี้ยได้ ตลาดเกิดใหม่อาจมีผลงานที่ดี อย่างไรก็ตาม ภายใต้สถานการณ์การเติบโตที่ไม่สมมาตร (เอื้อต่อสหรัฐฯ) หรือภาวะ Stagflation ทั่วโลก ตลาดเกิดใหม่จะเปราะบางมากขึ้น ในด้านค่าเงิน แม้ว่าจุดกระตุ้นจากการเลือกตั้งยังอีกหลายเดือน แต่แนวโน้มสินค้าโภคภัณฑ์และนโยบายการเงินควรยังคงสนับสนุนเงินเรียลบราซิลต่อไป (Wallstreetcn)

ข้อมูล:

สัปดาห์นี้ จีนจะเผยแพร่ข้อมูลรวมถึงยอดค้าปลีกสินค้าอุปโภคบริโภครวมเดือนเมษายนเทียบรายปี มูลค่าเพิ่มภาคอุตสาหกรรมของวิสาหกิจขนาดใหญ่เดือนเมษายนเทียบรายปี อัตราดอกเบี้ยเงินกู้ลูกค้าชั้นดี (LPR) ระยะ 1 ปี ณ วันที่ 20 พฤษภาคม และสัดส่วนเงินหยวนในระบบ Swift สำหรับการชำระเงินทั่วโลกเดือนเมษายน สหรัฐฯ จะเผยแพร่ข้อมูลรวมถึงจำนวนผู้ขอรับสวัสดิการว่างงานรายใหม่สัปดาห์สิ้นสุดวันที่ 16 พฤษภาคม การเปลี่ยนแปลงการจ้างงาน ADP รายสัปดาห์สิ้นสุดวันที่ 2 พฤษภาคม ดัชนียอดขายบ้านรอปิดเดือนเมษายนเทียบรายเดือน จำนวนบ้านเริ่มสร้างรายปีเดือนเมษายน ใบอนุญาตก่อสร้างเดือนเมษายน ดัชนีภาคการผลิตเฟดฟิลาเดลเฟียเดือนพฤษภาคม จำนวนผู้ขอรับสวัสดิการว่างงานต่อเนื่องสัปดาห์สิ้นสุดวันที่ 9 พฤษภาคม ดัชนี PMI ภาคการผลิตเบื้องต้นของ S&P Global เดือนพฤษภาคม ดัชนี PMI ภาคบริการเบื้องต้นของ S&P Global เดือนพฤษภาคม ดัชนีความเชื่อมั่นผู้บริโภคมหาวิทยาลัยมิชิแกนเดือนพฤษภาคม (ตัวเลขสุดท้าย) ดัชนีตลาดที่อยู่อาศัย NAHB เดือนพฤษภาคม คาดการณ์เงินเฟ้อ 1 ปีเดือนพฤษภาคม (ตัวเลขสุดท้าย) และดัชนีชี้นำ Conference Board เดือนเมษายนเทียบรายเดือนสหราชอาณาจักรจะเผยแพร่ข้อมูล ได้แก่ อัตราการว่างงาน ILO เฉลี่ย 3 เดือนของเดือนมีนาคม อัตราการว่างงานเดือนเมษายน จำนวนผู้ขอรับสวัสดิการว่างงานเดือนเมษายน CPI รายเดือนเดือนเมษายน ดัชนีราคาขายปลีกรายเดือนเดือนเมษายน PMI ภาคการผลิตเบื้องต้นเดือนพฤษภาคม PMI ภาคบริการเบื้องต้นเดือนพฤษภาคม ดัชนีคำสั่งซื้อภาคอุตสาหกรรม CBI เดือนพฤษภาคม ดัชนีความเชื่อมั่นผู้บริโภค GfK เดือนพฤษภาคม การกู้ยืมสุทธิภาครัฐเดือนเมษายน และยอดค้าปลีกรายเดือนปรับฤดูกาลเดือนเมษายน เยอรมนีจะเผยแพร่ข้อมูล ได้แก่ PPI รายเดือนเดือนเมษายน PMI ภาคการผลิตเบื้องต้นเดือนพฤษภาคม ดัชนีความเชื่อมั่นผู้บริโภค GfK เดือนมิถุนายน GDP รายปีไม่ปรับฤดูกาลขั้นสุดท้ายไตรมาส 1 และดัชนีบรรยากาศธุรกิจ IFO เดือนพฤษภาคม ยูโรโซนจะเผยแพร่ข้อมูล ได้แก่ ดุลการค้าปรับฤดูกาลเดือนมีนาคม CPI รายปีขั้นสุดท้ายเดือนเมษายน CPI รายเดือนขั้นสุดท้ายเดือนเมษายน PMI ภาคการผลิตเบื้องต้นเดือนพฤษภาคม ดุลบัญชีเดินสะพัดปรับฤดูกาลเดือนมีนาคม และดัชนีความเชื่อมั่นผู้บริโภคเบื้องต้นเดือนพฤษภาคม แคนาดาจะเผยแพร่ข้อมูล ได้แก่ CPI รายเดือนเดือนเมษายน และยอดค้าปลีกรายเดือนเดือนมีนาคม นอกจากนี้ยังมีการเผยแพร่ CPI พื้นฐานรายปีเดือนเมษายนของญี่ปุ่น PMI ภาคการผลิตเบื้องต้นเดือนพฤษภาคมของฝรั่งเศส และอัตราการว่างงานปรับฤดูกาลเดือนเมษายนของออสเตรเลีย

นอกจากนี้ ในจีน สำนักงานสถิติแห่งชาติ (NBS) จะเผยแพร่รายงานรายเดือนราคาอสังหาริมทรัพย์ที่อยู่อาศัยใน 70 เมืองขนาดใหญ่และขนาดกลาง สำนักงานข่าวสารคณะรัฐมนตรีจะจัดแถลงข่าวเกี่ยวกับผลการดำเนินงานเศรษฐกิจของประเทศ และจะเปิดรอบใหม่ของการปรับราคาน้ำมันสำเร็จรูปในประเทศ เวลา 02:00 น. ของวันที่ 21 พฤษภาคม เฟดสหรัฐฯ จะเผยแพร่รายงานการประชุมนโยบายการเงิน ธนาคารกลางออสเตรเลียจะเผยแพร่รายงานการประชุมนโยบายการเงินเดือนพฤษภาคม หัวหน้านักเศรษฐศาสตร์ ECB เลน และผู้ว่าการเฟด วอลเลอร์ จะกล่าวในการประชุมวิจัยของ ECB ประธานเฟดสาขาฟิลาเดลเฟีย พอลเซน ผู้มีสิทธิ์ลงคะแนนใน FOMC ปี 2026 จะกล่าวสุนทรพจน์

น้ำมันดิบ:

ณ ราคาปิดตลาดข้ามคืนวันศุกร์ที่ผ่านมา ความขัดแย้งระหว่างสหรัฐฯ-อิหร่านเรื่องการเดินเรือผ่านช่องแคบฮอร์มุซยังไม่ได้รับการแก้ไข ทำให้ราคาน้ำมันทั้งสองเกณฑ์มาตรฐานปรับตัวขึ้น WTI เพิ่มขึ้น 4.44% และเบรนท์เพิ่มขึ้น 3.55% ในรอบสัปดาห์ WTI เพิ่มขึ้น 10.73% และเบรนท์เพิ่มขึ้น 8.08%

เนื่องจากความขัดแย้งกับอิหร่านทำให้อุปทานพลังงานจากอ่าวเปอร์เซียถูกตัดขาด โรงกลั่นน้ำมันของสหรัฐฯ กำลังเร่งการผลิตเชื้อเพลิงเพื่อเติมเต็มช่องว่างอุปทานของน้ำมันเบนซิน ดีเซล และน้ำมันเครื่องบิน นักวิเคราะห์กล่าวว่าแนวโน้มการเติบโตอย่างรวดเร็วนี้คาดว่าจะทำให้โรงกลั่นหลายแห่งดำเนินการที่กำลังการผลิตสูงสุดที่มีประสิทธิภาพอย่างน้อยตลอดช่วงที่เหลือของปี 2026 อุปทานน้ำมันดิบสำรองที่ลดลงในยุโรปและภูมิภาคอื่นๆ ประกอบกับความยากลำบากในการฟื้นฟูโครงสร้างพื้นฐานหลังความขัดแย้งในตะวันออกกลางในระยะสั้น กำลังผลักดันให้ส่วนต่างกำไรจากการกลั่นน้ำมันดิบเพิ่มสูงขึ้นนักวิเคราะห์ระบุว่าแนวโน้มการเติบโตอย่างรวดเร็วนี้คาดว่าจะทำให้โรงกลั่นหลายแห่งดำเนินการที่กำลังการผลิตสูงสุดที่มีประสิทธิภาพอย่างน้อยจนถึงสิ้นปี 2026 ข้อมูลจากสำนักงานสารสนเทศด้านพลังงานสหรัฐฯ แสดงให้เห็นว่า "อัตราการใช้กำลังการผลิต" ปรับตัวสูงขึ้นติดต่อกัน 3 สัปดาห์ และขณะนี้ใกล้แตะ 92% ในช่วงสัปดาห์ที่ผ่านมา การผลิตน้ำมันเบนซินแตะระดับสูงสุดในรอบ 9 เดือน ขณะที่การผลิตน้ำมันเชื้อเพลิงเครื่องบินแตะระดับสูงสุดนับตั้งแต่ฤดูร้อนปี 2024 (Jin10 Data APP)

รัฐมนตรีว่าการกระทรวงพลังงานสหรัฐฯ ไรท์ กล่าวในงานที่ซาบีนพาส รัฐเท็กซัส เมื่อวันศุกร์ว่า สหรัฐฯ จะเติมน้ำมันดิบทุกบาร์เรลที่ปล่อยออกจากคลังสำรองน้ำมันเชิงยุทธศาสตร์ (SPR) กลับคืน เขากล่าวว่า: "เรากำลังปล่อยน้ำมันออกมาตอนนี้ และสำหรับทุกบาร์เรลที่ปล่อยออก เราจะเติมกลับอย่างน้อย 1.2 บาร์เรลเข้าคลังสำรอง ท้ายที่สุดแล้ว เราจะทำให้คลังสำรองมีขนาดใหญ่กว่าตอนที่เราเริ่มต้น" (Jin10 Data APP)

ตามรายงานของสื่อสหรัฐฯ รัฐบาลทรัมป์วางแผนปรับปรุงกระบวนการอนุมัติโครงการน้ำมันภายในเขตสำรองปิโตรเลียมแห่งชาติ-อะแลสกา เพื่อเพิ่มการผลิตน้ำมันดิบในเขตอาร์กติกของสหรัฐฯ การดำเนินการของกระทรวงมหาดไทยมีเป้าหมายเพื่อจัดตั้งกรอบการอนุมัติใหม่สำหรับการก่อสร้างและดำเนินงานสิ่งอำนวยความสะดวกในการผลิตน้ำมันและโครงสร้างพื้นฐานที่เกี่ยวข้อง ภายใต้แผนนี้ โครงการที่มีคุณสมบัติอาจได้รับการวิเคราะห์และอนุมัติเร็วขึ้น อาจภายในเพียง 30 วัน มาตรการนี้อาจเป็นประโยชน์ต่อบริษัทที่ถือสัญญาเช่าในเขตสำรอง เช่น ConocoPhillips, Santos และ Repsol รวมถึงเร่งการพิจารณาของรัฐบาลต่อโครงการต่างๆ เช่น โครงการ Willow ของ ConocoPhillips ซึ่งเคยถูกคัดค้านอย่างหนักจากนักเคลื่อนไหวด้านสภาพภูมิอากาศ ในช่วงความขัดแย้งกับอิหร่าน โดยมีอุปทานทั่วโลกประมาณ 20% ติดอยู่ในอ่าวเปอร์เซีย รัฐบาลทรัมป์ได้เพิ่มการเรียกร้องให้บริษัทน้ำมันสหรัฐฯ เพิ่มการผลิต (Jin10 Data APP)

ราคานำเข้าและส่งออกของสหรัฐฯ พุ่งขึ้นในเดือนเมษายน บันทึกการเพิ่มขึ้นมากที่สุดในรอบกว่า 4 ปี โดยได้รับแรงกดดันจากตลาดน้ำมันที่เกี่ยวข้องกับความขัดแย้งอิหร่าน ส่งสัญญาณเพิ่มเติมว่าเงินเฟ้อกำลังเพิ่มขึ้นในเศรษฐกิจที่ใหญ่ที่สุดของโลก ข้อมูลที่เผยแพร่เมื่อวันพฤหัสบดีโดยสำนักงานสถิติแรงงานแสดงให้เห็นว่าดัชนีราคานำเข้าเพิ่มขึ้น 1.9% เมื่อเทียบรายเดือน ซึ่งเป็นการเพิ่มขึ้นมากที่สุดนับตั้งแต่เดือนมีนาคม 2022 โดยต้นทุนปิโตรเลียมพุ่งขึ้น 19% ราคาส่งออกเพิ่มขึ้น 3.3% เมื่อเทียบรายเดือน ซึ่งเป็นการเพิ่มขึ้นมากที่สุดในรอบกว่า 4 ปีเช่นกัน (Wallstreetcn)

![โลหะปรับตัวขึ้นในวงกว้าง ดีบุก SHFE พุ่งขึ้นกว่า 2% ในขณะที่ทองคำและโลหะเงิน SHFE ดีดตัวขึ้น แต่ปรับตัวลดลงเป็นสัปดาห์ที่ห้าติดต่อกัน และโลหะเงิน SHFE ร่วงลงกว่า 10% ในสัปดาห์นี้ [ตลาดข้ามคืน]](https://imgqn.smm.cn/usercenter/fNuSg20251217171735.jpg)