SMM April 20:

Metals Market:

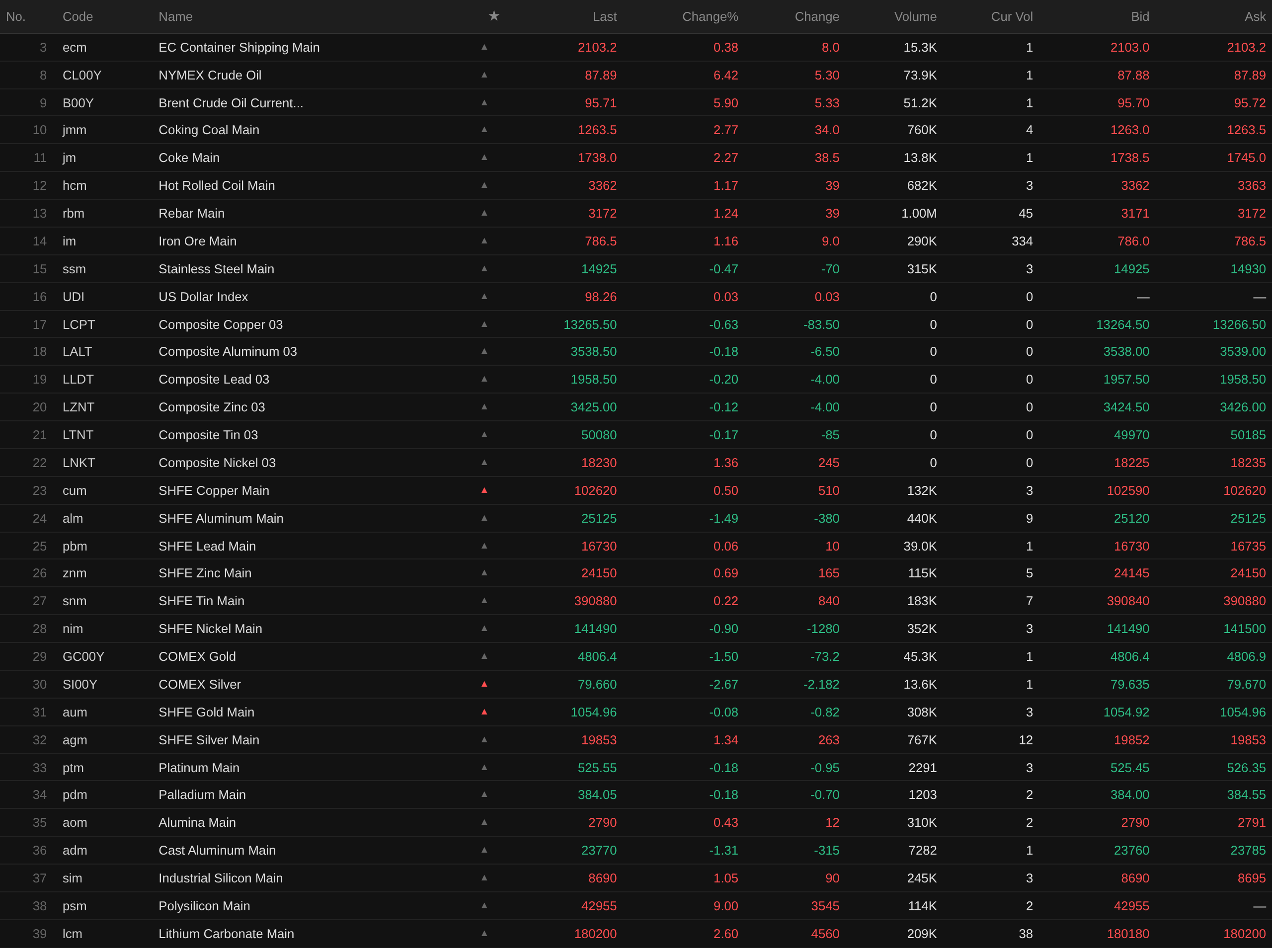

As of the daytime close, base metals on the domestic market mostly rose, with only SHFE aluminum and SHFE nickel declining. SHFE aluminum fell 1.49% and SHFE nickel fell 0.9%. The rest of the metals rose, with SHFE zinc up 0.69% and the others gaining less than 0.6%. The alumina front-month contract rose 0.43%, while the casting aluminum front-month contract fell 1.31%.

Additionally, the lithium carbonate front-month contract rose 2.6%, the silicon metal front-month contract rose 1.05%, and the polysilicon front-month contract hit the daily limit again during intraday trading, closing at 42,955 yuan/mt with a 9% gain. The Europe containerized freight front-month contract rose 0.38% to 2,103.2.

Ferrous metals all rose except stainless steel, which fell 0.47%. Hot-rolled coil, rebar, and iron ore all gained over 1% (hot-rolled coil 1.17%, rebar 1.24%, iron ore 1.16%). Coking coal and coke: coking coal rose 2.77% and coke rose 2.27%.

Overseas market, as of 15:07, all metals fell except LME nickel, which led the gains with a 1.36% rise. The rest declined, with LME copper leading the losses at 0.63%.

Precious metals, as of 15:07, COMEX gold fell 1.5% and COMEX silver fell 2.67%. In China, SHFE gold fell 0.08% and SHFE silver rose 1.34%.

Additionally, the platinum front-month contract fell 0.18% and the palladium front-month contract fell 0.18%.

Market Data as of 15:07 Today

Macro Front

China:

[NEA: Total Electricity Consumption Reached 2,514.1 billion kWh, Up 5.2% YoY, January-March]The National Energy Administration released March electricity consumption data. From January to March, total electricity consumption reached 2,514.1 billion kWh, up 5.2% YoY. By sector, the primary industry consumed 33.6 billion kWh, up 7.1% YoY. The secondary industry consumed 1,598.7 billion kWh, up 4.7% YoY; of which, industrial electricity consumption was 1,583.6 billion kWh, up 4.9% YoY, and high-tech and equipment manufacturing consumed 274.6 billion kWh, up 8.6% YoY. The tertiary industry consumed 483.3 billion kWh, up 8.1% YoY; of which, EV charging and battery swapping services and internet data services consumed 37.6 billion and 22.9 billion kWh respectively, with growth rates of 53.8% and 44.0%. Urban and rural residential electricity consumption was 398.5 billion kWh, up 3.4% YoY.

[April LPR Unchanged: Both 5-Year and 1-Year Rates Held Steady for the Eleventh Consecutive Month]The April LPR was announced: PBOC kept the 1-year and 5-year LPR at 3% and 3.5% respectively, unchanged for the eleventh consecutive month.

[Foshan's Commercial Housing "Trade-in" Policy Is Here! First Batch Involves 22 Residential Projects]Recently, the Notice on Organizing the First Batch of Commercial Housing "Trade-in" Program by the Foshan Municipal Housing and Urban-Rural Development Bureau was officially released. This is not merely an encouraging document; it is a solution that systematically clears bottlenecks in housing replacement through model innovation and a policy package. It aims to drive the real estate market's transition from "one-sided transactions" to a "virtuous cycle between existing and new housing stock," achieving a win-win outcome for residents, enterprises, and the market. The innovation of Foshan's trade-in policy lies in bringing multiple real estate enterprises into the program: Foshan Anju, Chancheng Anju, Nanhai Youju, Shunde Chengtie, Gaoming Airport Construction, and Sanshui Anju serve as acquisition entities, while Foshan Chengfa, Foshan Urban Renewal, Foshan Lianzhi, Heyue Yaji, Shunkong Chengtou, Yongdeli Commerce, Sanshui Chanfa, and Miaohui Real Estate provide new housing sources. This model determines the value of existing homes through negotiation, establishes a "contract termination protection period" to avoid blindly pushing for lower prices, thereby completing the "sell old, buy new" closed loop and serving as a market stabilizer. (Foshan Release)

US Dollar:

As of 15:07, the US dollar index rose 0.03% to 98.26. According to a CITIC Securities research report, US Fed Governor Miran and three other economists recently co-published a working paper titled "A User's Guide to Restructuring the Federal Reserve's Balance Sheet," whose structure bears similarities to the previously widely discussed "A User's Guide to Restructuring the Global Trading System." The paper challenges the conventional view that the US Fed cannot significantly reduce its balance sheet, arguing that reserve demand is largely determined by the regulatory environment and that balance sheet reduction can be achieved without causing unexpected market stress by adjusting the regulatory framework, curbing precautionary motives, and addressing other sources of reserve demand. Using Monte Carlo simulations, the paper estimates the potential balance sheet reduction space at $1.2 trillion to $2.1 trillion. We believe the "balance sheet reduction guide" has a certain degree of real-world feasibility, but some options are somewhat idealistic. (Jin10 Data APP)

According to the CME "Fed Watch": the probability of the US Fed raising interest rates by 25 basis points in April was 0.5%, while the probability of keeping rates unchanged was 99.5%. The probability of a cumulative interest rate cut of 25 basis points by June was 4.5%, the probability of keeping rates unchanged was 95%, and the probability of a cumulative rate hike of 25 basis points was 0.5%. (Jin10 Data APP)

On the macro front:

Germany's March PPI month-on-month rate, Canada's March CPI month-on-month rate, and other data were to be released today. Also worth noting: German Chancellor Merz and European Central Bank President Lagarde delivered speeches; Trump said a US delegation would arrive in Islamabad on the evening of the 20th for negotiations, while Iran denied reports of a second round of talks being held in Islamabad.

Crude oil:

As of 15:07, oil prices in both markets surged, with WTI up 6.42% and Brent up 5.9%. Iran had once again closed the Strait of Hormuz, driving oil prices sharply higher.

On the 19th local time, an Iraqi oil ministry official said the closure of the Strait of Hormuz would block the export of nearly 4 million barrels of Iraqi crude oil over the next three days. The Iranian Islamic Revolutionary Guard Corps Navy issued a statement on the 18th saying that, due to the US violating ceasefire commitments and failing to lift the naval blockade on Iranian ports and vessels, the Strait of Hormuz would be blocked starting that evening. (CCTV News)

Gary Pedersen, head of trading house Gunvor, warned that the oil market was facing more turbulence as Middle East tensions collided with seasonal slowdown in crude oil demand, increasing the likelihood of further sharp and unpredictable fluctuations in crude oil prices. (Jin10 Data)

The International Energy Agency forecast that global crude oil demand would decline by 1.5 million barrels per day in Q2, the largest drop since the COVID-19 pandemic. OPEC's forecast was relatively mild, projecting a daily decline of 500,000 barrels. (Jin10 Data)

A CICC research report noted that as the Iran situation entered its 7th week, the situation saw a further turning point. Although the first round of peace talks "collapsed," both the US and Iran "announced" the reopening of navigation through the Strait of Hormuz, which still largely boosted optimistic sentiment in the market, despite subsequent reversals. This was largely in line with our base case assumption: while short-term reversals remain possible, a complete loss of control over the medium term is not the base case scenario, as Trump still has midterm elections to consider, and a comprehensive and uncontrollable escalation serves neither side's interests. Under this scenario, the Brent crude oil price center would gradually pull back to around $80 in Q2 and Q3, and the US Fed could still cut interest rates. (Jin10 Data APP)

SMM Daily Review

►

►

►

►

►

►

►

►

►

►

►

►

![Geopolitical Disruptions Drove Repeated Bull-Bear Reversals, BC Copper Saw Wild Swings with Slight Gains [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/LbxVx20251217171714.jpeg)