ก่อนอื่น ทบทวนแนวโน้มราคาในเดือนกุมภาพันธ์ของอะลูมิเนียมอัลลอยทุติยภูมิ: ตลาดฟิวเจอร์ส: ในเดือนกุมภาพันธ์ สัญญาอะลูมิเนียมอัลลอยหล่อที่มีการซื้อขายมากที่สุดโดยรวมมีรูปแบบ “ปรับลงก่อนแล้วทรงตัว” ก่อนจะรีบาวด์หลังวันหยุด ช่วงต้นเดือนยังคงต่อเนื่องจากแนวโน้มอ่อนตัวปลายเดือนมกราคม โดยราคาฟิวเจอร์สส่วนใหญ่คืนกำไรที่ทำไว้ก่อนหน้า และความผันผวนขยายตัวชัดเจน; ต่อมาเมื่อใกล้ตรุษจีน การซื้อขายซบเซาและราคาส่วนใหญ่แกว่งในกรอบและสะสมฐาน หลังวันหยุด ราคาฟิวเจอร์สรีบาวด์อย่างรวดเร็ว เข้าสู่เดือนมีนาคม ท่ามกลางแรงรบกวนจากปัจจัยภายนอก เช่น ความขัดแย้งสหรัฐฯ–อิหร่านที่ทวีความรุนแรงขึ้น ความเชื่อมั่นฝั่งขาขึ้นกลับมาร้อนแรงอีกครั้งและราคาปรับแข็งแกร่งขึ้นอย่างเห็นได้ชัด

ตลาดสปอต: ช่วงต้นกุมภาพันธ์ ถูกกดดันจากการดิ่งลงแรงของฟิวเจอร์ส ราคาเสนอขายสปอตปรับลงเร็ว ก่อนจะหยุดลงและทรงตัว; หลังวันหยุด พร้อมกับการรีบาวด์ของอะลูมิเนียมปฐมภูมิและความคืบหน้าการกลับมาผลิต ราคาได้ฟื้นตัวขึ้นบ้าง ส่วนต่างราคา: ในเดือนกุมภาพันธ์ จุดศูนย์กลางราคาของอะลูมิเนียมปรับลง ขณะที่ราคา ADC12 ได้แรงหนุนจากต้นทุนและได้รับผลจากอุปทานหดตัว จึงค่อนข้างยืดหยุ่น โดยยังคงมีพรีเมียมเหนือราคา A00; ในเดือนมีนาคม เมื่ออะลูมิเนียมปฐมภูมิปรับขึ้นแรงอีกครั้ง พรีเมียมจึงแคบลงอย่างมีนัยสำคัญ ณ วันที่ 6 มีนาคม SMM ประเมินราคา SMM ADC12 ที่ 24,600 หยวน/ตัน เพิ่มขึ้นสะสม 750 หยวน/ตันจากต้นเดือนกุมภาพันธ์

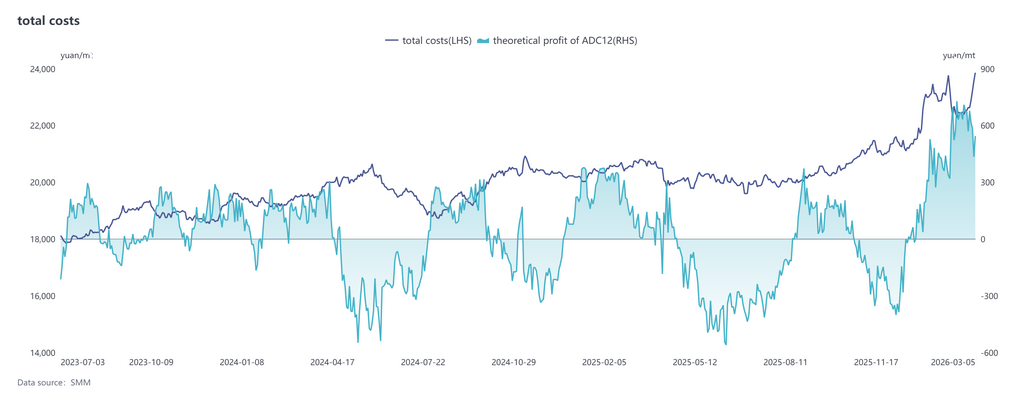

ด้านต้นทุน ตามข้อมูลล่าสุดของ SMM ต้นทุนรวมเชิงทฤษฎีของอุตสาหกรรม ADC12 ในเดือนกุมภาพันธ์ลดลงมาอยู่ที่ 22,492 หยวน/ตัน ลดลง 2.6 จุดเปอร์เซ็นต์เมื่อเทียบเดือนต่อเดือนจากเดือนมกราคม จากมุมมองโครงสร้างต้นทุน ต้นทุนเศษอะลูมิเนียมต่อหนึ่งตันปรับลงมาอยู่ที่ 20,245 หยวน โดยสัดส่วนลดลงเล็กน้อยเป็น 90.0% และยังเป็นแหล่งต้นทุนหลัก; ต้นทุนทองแดงต่อหนึ่งตันทรงตัวโดยพื้นฐานที่ 850 หยวน สัดส่วนขยับขึ้นเล็กน้อยเป็น 3.8%; ต้นทุนซิลิคอนต่อหนึ่งตันขยับขึ้นเป็น 491 หยวน สัดส่วนฟื้นกลับมาเป็น 2.2% โดยรวม การเปลี่ยนแปลงของโครงสร้างต้นทุนค่อนข้างเล็ก และเศษอะลูมิเนียมยังคงมีบทบาทครองสัดส่วนอย่างเด็ดขาดในระบบต้นทุน ช่วงเวลาเดียวกัน กำไรเชิงทฤษฎีของอุตสาหกรรมสำหรับ ADC12 อยู่ที่ราว 643 หยวน/ตัน โดยรวมยังอยู่ในแดนกำไร เข้าสู่เดือนมีนาคม ภายใต้ฉากหลังที่ราคาอะลูมิเนียมปฐมภูมิปรับขึ้นต่อเนื่อง และอุปสงค์จัดซื้อวัตถุดิบค่อย ๆ ปลดปล่อยจากการที่ผู้ประกอบการกลับมาดำเนินงาน คาดว่าราคาเศษอะลูมิเนียมจะทรงตัวได้ดี และจุดศูนย์กลางต้นทุนระยะสั้นมีแนวโน้มขยับสูงขึ้นต่อไป กลายเป็นแรงขับเคลื่อนหลักที่หนุนให้ราคาอะลูมิเนียมทุติยภูมิแข็งแกร่งขึ้น

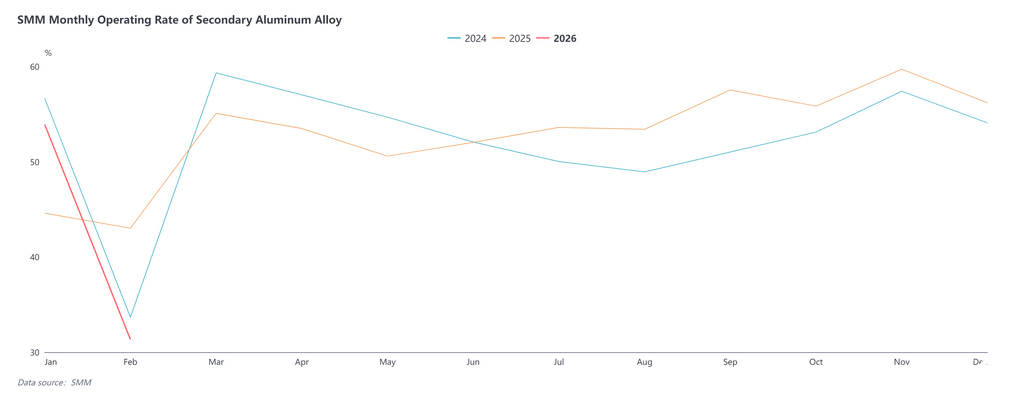

ด้านอุปทาน อัตราการดำเนินงานของอุตสาหกรรมอลูมิเนียมผสมทุติยภูมิอยู่ที่ 31.3% ในเดือนกุมภาพันธ์ ลดลงอย่างรุนแรง 22.6 จุดจากเดือนก่อนหน้าและลดลง 11.7 จุดจากปีก่อนหน้า ภายใต้ผลกระทบจากการหยุดผลิตในช่วงเทศกาลตรุษจีน จำนวนวันผลิตที่มีประสิทธิภาพขององค์กรลดลงอย่างเห็นได้ชัด โดยส่วนใหญ่มีปริมาณผลิตลดลง 30–50% ส่งผลให้ด้านอุปทานของอุตสาหกรรมหดตัวลงอย่างมาก นอกจากนี้ การควบคุมด้านสิ่งแวดล้อมในบางพื้นที่เข้มงวดขึ้นก่อนวันหยุดยาว และเนื่องจากกฎระเบียบนโยบายการคลังและภาษี เช่น "การออกใบแจ้งหนี้ย้อนกลับ" ยังไม่มีความชัดเจน องค์กรจึงระมัดระวังในการผลิตมากขึ้น บางแห่งหยุดงานล่วงหน้าหรือเลื่อนการกลับมาดำเนินการ และบางแห่งหยุดผลิตเกือบทั้งเดือน

ด้านอุปสงค์ก็ยังคงอ่อนแอ นอกเหนือจากปัจจัยตามฤดูกาลแล้ว หลายปัจจัย เช่น การลดสต็อกก่อนวันหยุดของผู้ผลิต การปรับนโยบายภาษีซื้อรถยนต์พลังงานใหม่ และผู้บริโภคปลายทางที่รอดูส่วนลดในงานแสดงรถยนต์ฤดูใบไม้ผลิ ล้วนส่งผลให้การผลิตและยอดขายรถยนต์ในเดือนกุมภาพันธ์ลดลง สร้างแรงกดดันต่อคำสั่งซื้อของผู้ผลิตอลูมิเนียมทุติยภูมิ เมื่อเข้าสู่เดือนมีนาคม เนื่องจากห่วงโซ่อุตสาหกรรมกลับมาดำเนินการเต็มรูปแบบและตารางการผลิตรถยนต์ค่อยๆ ฟื้นตัว อุปทานและอุปสงค์คาดว่าจะฟื้นตัวไปพร้อมกัน โดยอัตราการดำเนินงานของอุตสาหกรรมมีแนวโน้มที่จะปรับตัวสูงขึ้นทุกสัปดาห์และกลับสู่ระดับปกติก่อนวันหยุด อย่างไรก็ตาม อัตราการฟื้นตัวยังคงขึ้นอยู่กับการรับคำสั่งซื้อที่แท้จริงจากผู้บริโภคปลายทาง

คำแปลภาษาอังกฤษของข้อความข้างต้นคือ:

โดยรวมแล้ว ราคา ADC12 ในเดือนมีนาคมคาดว่าจะผันผวนในขณะที่ยังทรงตัวได้ดี ในด้านมหภาค ความตึงเครียดที่เพิ่มขึ้นในตะวันออกกลางทำให้ความกังวลของตลาดต่อความมั่นคงของอุปทานอลูมิเนียมเพิ่มสูงขึ้น ส่งผลให้ราคาอลูมิเนียมทั้งในและต่างประเทศปรับตัวขึ้น ในขณะที่ราคาอลูมิเนียมปฐมภูมิยังคงอยู่ในระดับสูงและการไหลเวียนของเศษอลูมิเนียมยังคงตึงตัว ต้นทุนการผลิตอลูมิเนียมทุติยภูมิไม่น่าจะผ่อนคลายลง ส่งผลให้ผู้ผลิตมีความตั้งใจที่จะยึดราคาให้มั่นคงและมีแนวโน้มที่ราคาจะขึ้นมากกว่าลง ในระยะสั้น การสนับสนุนจากต้นทุนและการปล่อยอุปทานที่ค่อยเป็นค่อยไปจะช่วยหนุนราคา ADC12 และคาดว่าตลาดจะยังทรงตัวได้ดี แนวโน้มในระยะกลางจะขึ้นอยู่กับการฟื้นตัวของการบริโภคปลายทางที่แท้จริงมากขึ้นหากคำสั่งซื้อในภาคการหล่อแบบไดคาสติ้งเพิ่มขึ้นอย่างมีนัยสำคัญ คาดว่าศูนย์กลางราคาจะยังคงปรับสูงขึ้นต่อเนื่อง; หากการฟื้นตัวของอุปสงค์ต่ำกว่าคาด ประกอบกับอัตราการเดินเครื่องฝั่งอุปทานที่ยังเพิ่มขึ้นต่อเนื่อง ราคาเข้าสู่รูปแบบผันผวนในระดับสูง โดยรวมแล้ว คาดว่าศูนย์กลางการเคลื่อนไหวของราคา ADC12 ในเดือนมีนาคมจะค่อย ๆ ปรับสูงขึ้น โดยขอบเขตและจังหวะการปรับขึ้นได้รับอิทธิพลหลักจากความแข็งแกร่งของการปลดปล่อยการบริโภคปลายน้ำและสภาวะอุปทานวัตถุดิบ

![[SMM ข่าวด่วนอะลูมิเนียม] Vedanta ทำสถิติผลผลิตอะลูมิเนียมสูงสุดเป็นประวัติการณ์ เพิ่มแรงสนับสนุนด้านอุปทานเล็กน้อย](https://imgqn.smm.cn/usercenter/BrEfh20251217171652.jpg)

![การกลับมาทำงานหลังวันหยุดส่งผลให้อัตราการเดินเครื่องของผู้ผลิตอะลูมิเนียมทุติยภูมิเพิ่มขึ้นอย่างรวดเร็วในเดือนมีนาคม [บทวิเคราะห์ SMM]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)