Key Figures at a Glance

|

Indicator |

Apr 2026 |

May 2026 |

MoM % |

YoY % |

|

Chrome ore exports (global, mt) |

2.47 million |

2.43 million |

-1.82% |

+43.08% |

|

HC ferrochrome exports (global, mt) |

117,168 |

123,795 |

+5.66% |

-48.76% |

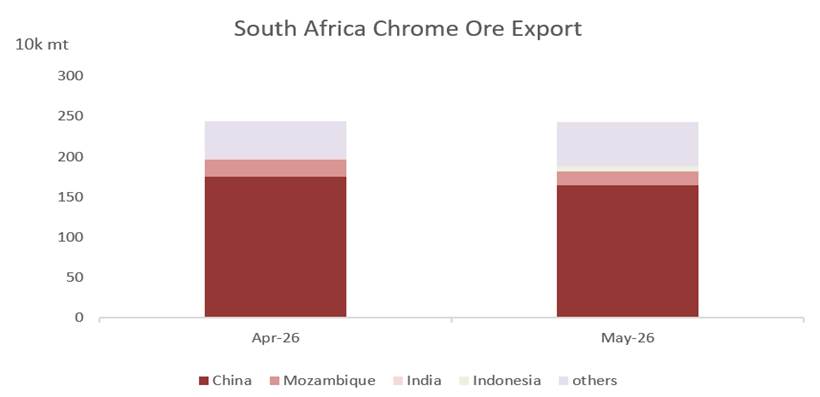

South Africa maintained robust chrome ore exports through April and May despite the slight monthly pullback. The strong year-on-year growth reflects resilient international demand, led overwhelmingly by Chinese ferrochrome producers, whose smelters continued to run at high operating rates. China absorbed a record slightly 12.5 million mt of South African chrome ore across 2025, up 23.8% year-on-year, and April–May trade flows confirm that this buying pace has carried through into 2026.

Figure 1. Top chrome ore export destinations, April & May 2026 — China's share remains dominant.

Beyond China, secondary destinations remain a small fraction of total volumes, underscoring how concentrated South Africa's chrome ore trade has become around a single buyer. This concentration leaves export volumes highly sensitive to swings in Chinese ferrochrome operating rates and stainless steel demand.

HIGH-CARBON FERROCHROME EXPORTS

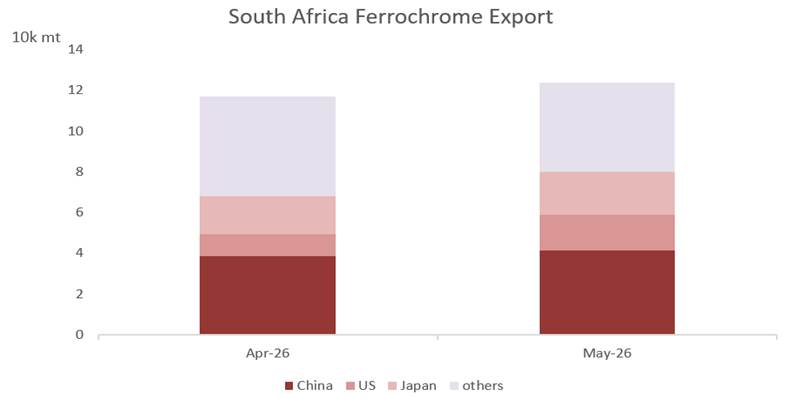

High-carbon ferrochrome exports posted a modest monthly recovery in May, but volumes remained far below year-ago levels, consistent with the sharp contraction in South African smelter output seen through late 2025. Industry export-tracking data for the fourth quarter of 2025 showed HC ferrochrome shipments down as much as 63% year-on-year as furnace closures and care-and-maintenance decisions removed capacity from the market, even as raw ore shipments surged over the same period.

Figure 2. Major high-carbon ferrochrome export destinations, April & May 2026.

Ferrochrome export destinations remain more diversified than chrome ore, spanning China, other Asian buyers and, to a lesser extent, European and North American stainless steel producers. China remains among the leading buyers of South African ferrochrome even as it continues to expand its own domestic smelting capacity, effectively competing with South African alloy in its own downstream market.

MARKET ANALYSIS AND OUTLOOK

The continued divergence between rising chrome ore exports and constrained ferrochrome shipments reflects a structural realignment already well underway in South Africa's chromium value chain, rather than a short-term fluctuation. High grid electricity costs, an ageing furnace fleet and persistent logistics bottlenecks have steadily eroded the competitiveness of domestic smelting, pushing an increasing share of production toward raw-ore export instead of local beneficiation. Broader export-tracking data for the final quarter of 2025 illustrates the scale of this shift: raw chrome ore and concentrate shipments climbed roughly 35% year-on-year even as ferrochrome exports fell sharply over the same period.

Electricity relief begins to filter through

A potential inflection point emerged in early 2026. In January, the National Energy Regulator of South Africa (NERSA) approved an initial negotiated electricity tariff framework for ferrochrome smelters, and in early April Eskom concluded a tentative five-year negotiated pricing agreement (NPA) with major integrated producers, including Samancor Chrome and Glencore-Merafe, that would lower the effective rate to roughly 62 cents/kWh, down from the previously approved 87.74 cents/kWh framework. If ratified by NERSA and sustained, this relief could ease pressure on smelter margins and slow the shift toward raw-ore exports — though the benefit will take time to translate into furnace restarts and is unlikely to have materially influenced the April–May 2026 trade data covered in this report.

Export policy remains a key swing factor

South Africa's government continues to advance measures intended to revive domestic beneficiation, including a permitting requirement for chrome ore exports administered by the International Trade Administration Commission (ITAC) and a proposed export tax on unprocessed ore, discussed at rates of up to 25%. Implementation timing remains uncertain following public consultation. Reaction within the industry is mixed: integrated producers with in-house smelters have broadly welcomed the measures, while non-integrated miners warn that export curbs could reduce revenue and jobs without necessarily redirecting more ore to under-utilized domestic furnaces, many of which are held by producers that already have secure, long-term ore supply. Formal adoption of export controls or a tax would be a significant swing factor for trade volumes in the second half of 2026.

Logistics bottlenecks keep reshaping trade routes

Persistent congestion and underperformance across Transnet's rail network and the Richards Bay terminal have continued to push volumes toward alternative routes, particularly the Maputo corridor via Komatipoort in Mozambique, which now handles more than half of South Africa's chrome ore exports. This diversification has helped sustain export volumes but adds cost and route risk, as illustrated by periodic disruptions at the Mozambican border and a recent reported shift of some volumes toward regional trading hubs such as Hong Kong.

China remains the demand anchor; Indonesia a growing headwind

Chinese buyers absorbed a record 12.5 million mt of South African chrome ore across 2025, up 23.8% year-on-year, as Chinese ferrochrome capacity and stainless steel output continued to expand. According to SMM data, China's monthly high-carbon ferrochrome output climbed steadily over 2025 — from roughly 553,600–592,200 mt in the first quarter, to 710,400–751,300 mt in the second quarter, above 790,000 mt from July onward, and reaching a year-end high of approximately 882,100–887,900 mt in November–December. This demand base is expected to remain the primary support for South African chrome ore exports through 2026. At the same time, Indonesia's fast-growing domestic ferrochrome and stainless steel capacity is gradually reducing its historical reliance on imported alloy, a headwind that applies more directly to South African ferrochrome exports than to chrome ore shipments.

Price and regulatory backdrop

SMM assessments indicate that chrome ore prices have limited room for further near-term upside given thin producer margins, even as strong Chinese ferrochrome operating rates keep underlying demand firm. Ferrochrome prices, by contrast, remain pressured by global oversupply and soft ex-China demand. Further out, the European Union's Carbon Border Adjustment Mechanism (CBAM), effective from January 2026, may gradually reshape sourcing patterns for chromium-bearing alloys among European stainless steel producers — a factor with limited near-term impact on this report's data but worth monitoring for its effect on non-China trade flows over 2026–27.

Outlook — H2 2026

■ Chrome ore exports are likely to stay elevated, supported by firm Chinese ferrochrome and stainless steel demand, though a finalized export permit/tax regime could dampen volumes moving through non-integrated export channels.

■ High-carbon ferrochrome exports should remain range-bound at levels well below 2024–25, with any meaningful recovery contingent on the pace of NPA-driven electricity relief and subsequent furnace restarts.

■ Chrome ore prices are expected to see limited further upside near term amid low producer margins; ferrochrome prices are likely to stay under pressure from global oversupply.

■ Transnet and Maputo-corridor logistics performance will remain a key swing factor for shipment volumes of both commodities.

![[SMM Analysis] H1 2026 China Rhenium Market Semi-Annual Review](https://imgqn.smm.cn/usercenter/QmrGh20251217171725.jpg)

![Short-term Bull Momentum Repair, Aluminum Alloy Drifting Higher; Cautious Price Adjustments in Spot Market, Sluggish Transactions [ADC12 Daily Price Review]](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)

![Low Willingness to Sell among Manufacturers, Weak Futures and Spot Prices [SMM SiMn Weekly Review]](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)