I. Lead Concentrates Market: Supply-Demand Tight Balance, Signs of TC Increases Disappear

According to SMM's latest survey, entering May, lead concentrate TCs (Pb50 TC) and silver-bearing payable indicators remained stable overall, but the rebound in silver prices firmed up some silver-bearing lead concentrate TC quotations once again.

In April, China's lead concentrates supply gradually recovered, and coupled with precious metal prices coming under pressure and weakening, some domestic lead concentrate TCs showed signs of edging up. In particular, sellers of silver-bearing lead concentrates who had quoted extremely low prices in March raised their quotations slightly out of concern over continued silver price weakness. However, as the US-Iran peace talks progressed and the Peruvian energy crisis escalated, silver prices were reassessed, and smelters regained expectations of by-product revenue from high-silver lead ore, causing the upward trend in lead concentrate TCs to simultaneously disappear.

Regarding the impact of sulphuric acid, although zinc concentrate TCs were notably reduced in May due to the sharp rise in sulphuric acid prices (SMM Zn50 domestic weekly TCs had already fallen to 700 yuan/mt in metal content), lead concentrate TCs did not decline in tandem over the same period. Multiple mine enterprises indicated that lead concentrate TCs had almost no downside room left.

On the imported ore front, smelters maintained mainstream quotations of -$150 to -$130/dmt. However, affected by the continued decline in the SHFE/LME lead price ratio, widening import losses, and limited ex-China supply, smelters showed poor enthusiasm for negotiating and purchasing imported ore, and actual transactions of imported ore remained thin.

II. Precious Metals Market: US-Iran Peace Talks and Peruvian Energy Crisis Ignite Silver Prices, Payable Indicator Transmission Yet to Materialize

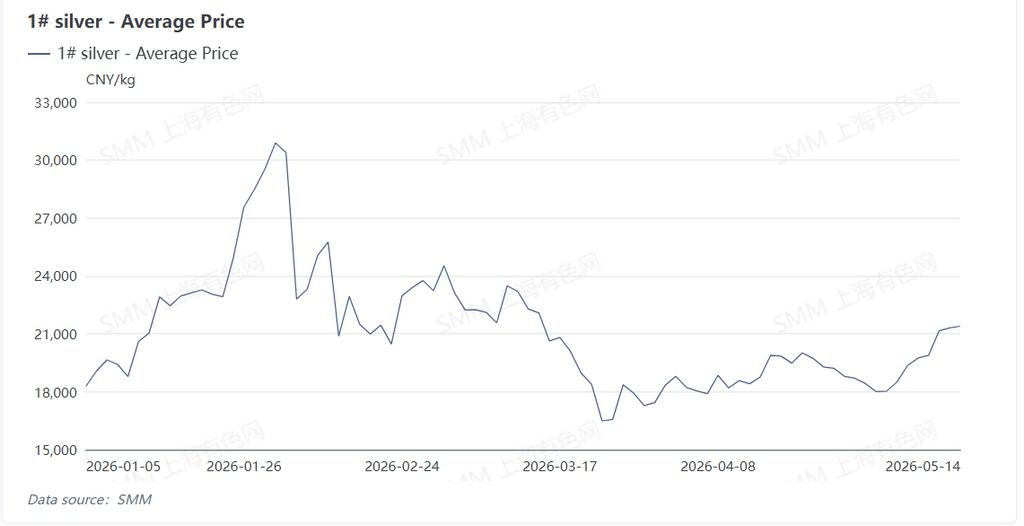

Amid disruptions from the back-and-forth US-Iran peace talks, India's sharp increase in gold and silver import tariffs, and the Peruvian energy crisis, silver prices experienced wild swings. On May 11, Peru officially issued an emergency decree on the energy crisis, consolidating the silver price rise that had previously been boosted by the US-Iran peace talks. Peru is the world's largest country by silver reserves, with silver-bearing mineral reserves of approximately 110,000 mt in metal content, accounting for 18% of the global total. In the short term, Peru's energy crisis has largely triggered sentiment-driven reactions, and whether it will have a substantive impact on mine-side supply still requires close monitoring of subsequent export dynamics of silver-bearing concentrates and lead-zinc ore.

Lead concentrates are typically rich in silver, and silver price fluctuations theoretically affect the silver-bearing payable indicator and the overall value of lead concentrates. However, according to SMM, wild swings in precious metals have not yet been transmitted to the silver-bearing pricing mechanism.

The reasons are mainly twofold:

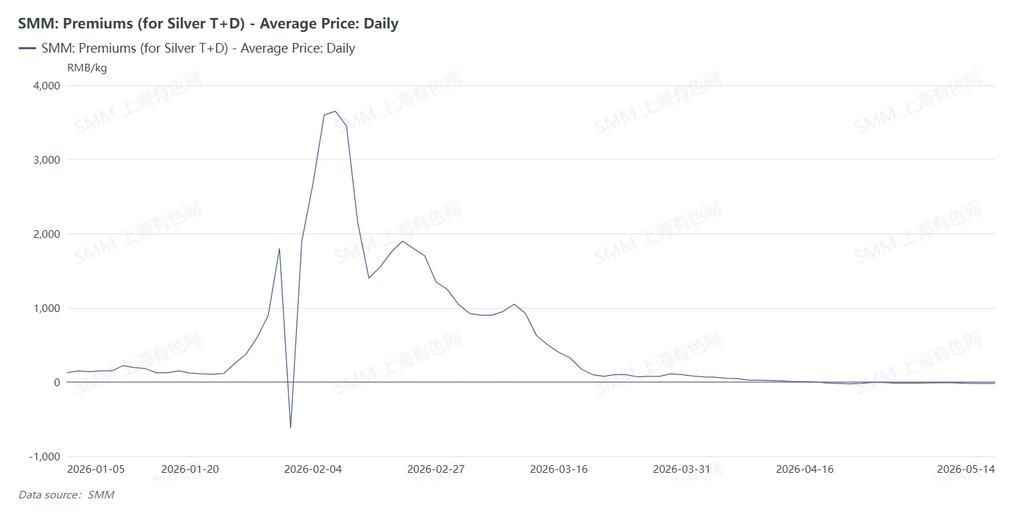

First, silver price fluctuations are primarily driven by short-term sentiment, and their sustainability remains questionable. The silver price surge triggered by Peru's energy crisis was largely a sentiment-driven reaction. The spot market struggled to catch up, discounts on actual silver ingot transactions widened, inventory gradually accumulated, and fundamentals could hardly support the relatively strong price trend.

Second, silver-bearing pricing adjustments are inherently lagging. Silver-bearing payable indicators are typically negotiated and adjusted on a monthly or quarterly basis, making it difficult for short-term silver price fluctuations to be immediately reflected. Moreover, against the backdrop of unclear precious metal trends, buyers and sellers are more inclined to maintain existing pricing methods and make adjustments once the trend becomes clearer.

III. Market Outlook: Lead Concentrate TCs Expected to Remain Stable in the Short Term

On one hand, if Peru's energy crisis continues to escalate, it may affect the supply of silver-bearing lead concentrates, creating upward pressure on the silver-bearing payable indicator, and may also put lead concentrate TCs under renewed downward pressure. However, considering that lead TCs have already fallen to low levels and that smelters have expectations of proactive production cuts due to wild swings in raw material prices, the downside room for further TC declines is relatively small.

On the other hand, the lead market is currently in the off-season for consumption, lead prices are trending weak, and primary lead smelters have limited bargaining power in raw material procurement. Against this backdrop, high-value silver-bearing lead concentrates will once again become the preferred procurement choice for smelters.

Key factors to monitor going forward: the persistence of Peru's energy crisis, and whether silver prices can hold their gains and stay high.

![SHFE Lead Moved Sideways Intraday Before Closing Lower, Weak Demand Suppressed Upside Room [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/EhsCj20251217171721.jpeg)