SMM May 7 News:

As of April 30, the most-traded SHFE zinc contract closed at 23,645 yuan/mt, up 165 yuan/mt for the month, a gain of 0.7%. Zinc prices rebounded from lows in April, touching a low of 23,430 yuan/mt at the beginning of the month and a high of 24,515 yuan/mt at month-end, though the overall price center pulled back. Heading into May, with the tight domestic ore supply situation persisting, how will zinc prices perform?

Macro perspective. In April, the market continued to focus on the Middle East situation. Despite repeated fluctuations, ceasefire agreements and resumed negotiations between the two sides released easing signals, boosting market sentiment. Non-ferrous metal prices generally rebounded, and zinc prices rose accordingly.

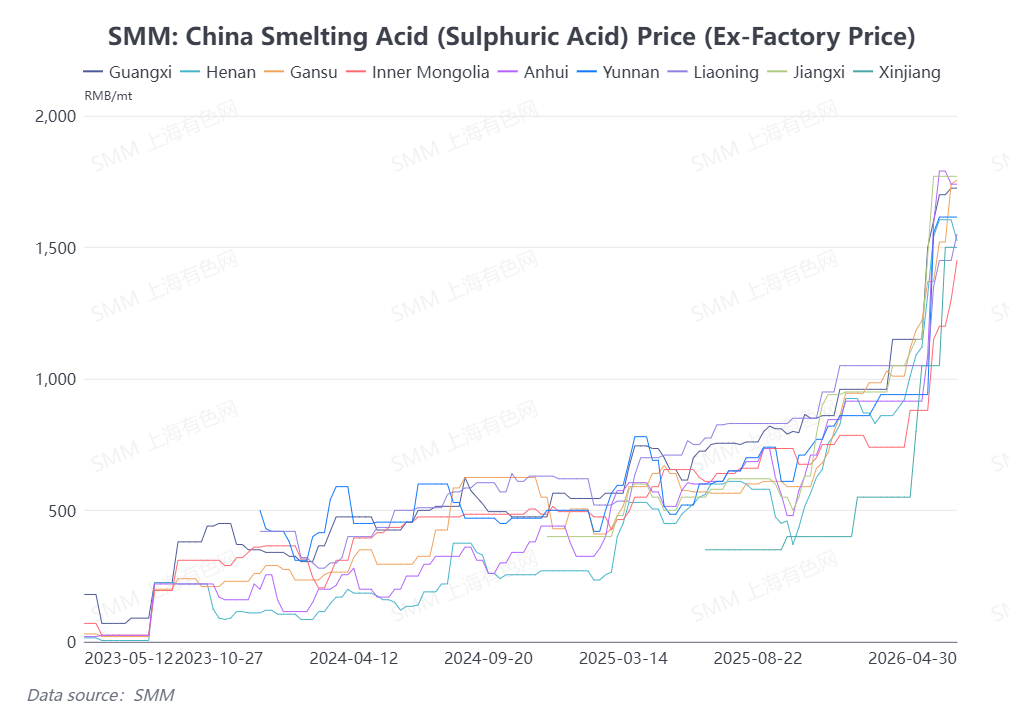

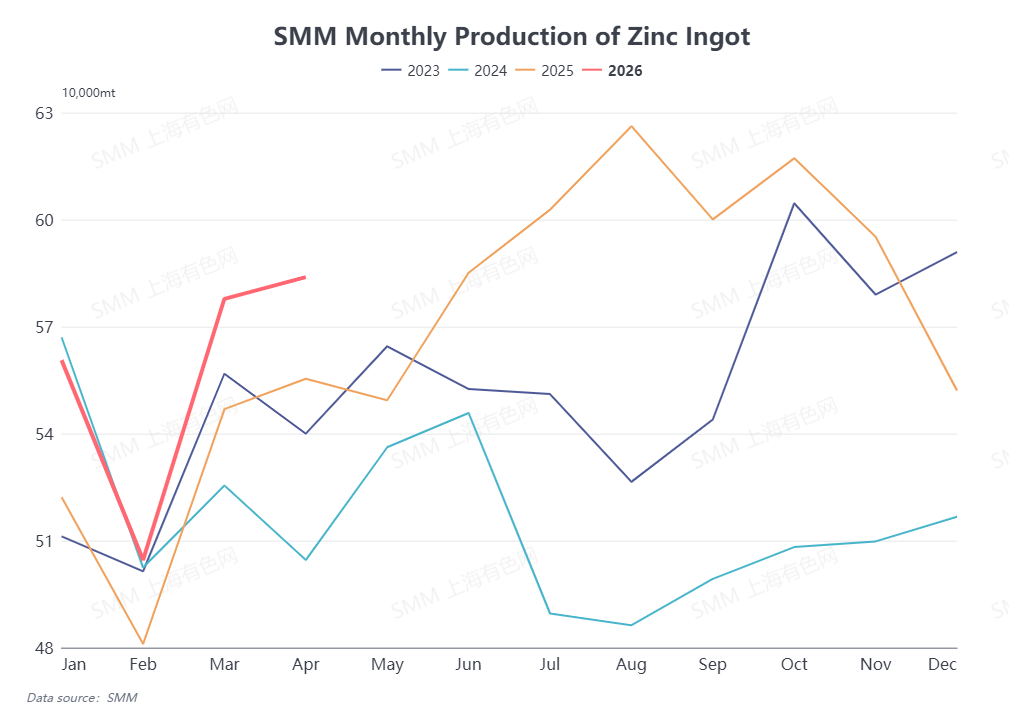

Supply side. In April, sulphuric acid prices remained elevated across many regions in China, and combined with by-product profit contributions, domestic smelters maintained high production enthusiasm, with refined zinc production edging up MoM. Heading into May, although domestic zinc concentrate TCs have fallen to historical lows, smelters have shown no obvious signs of production cuts due to still-elevated sulphuric acid prices. Refined zinc production is expected to decline only marginally MoM in May, and domestic zinc ingot supply is expected to remain robust.

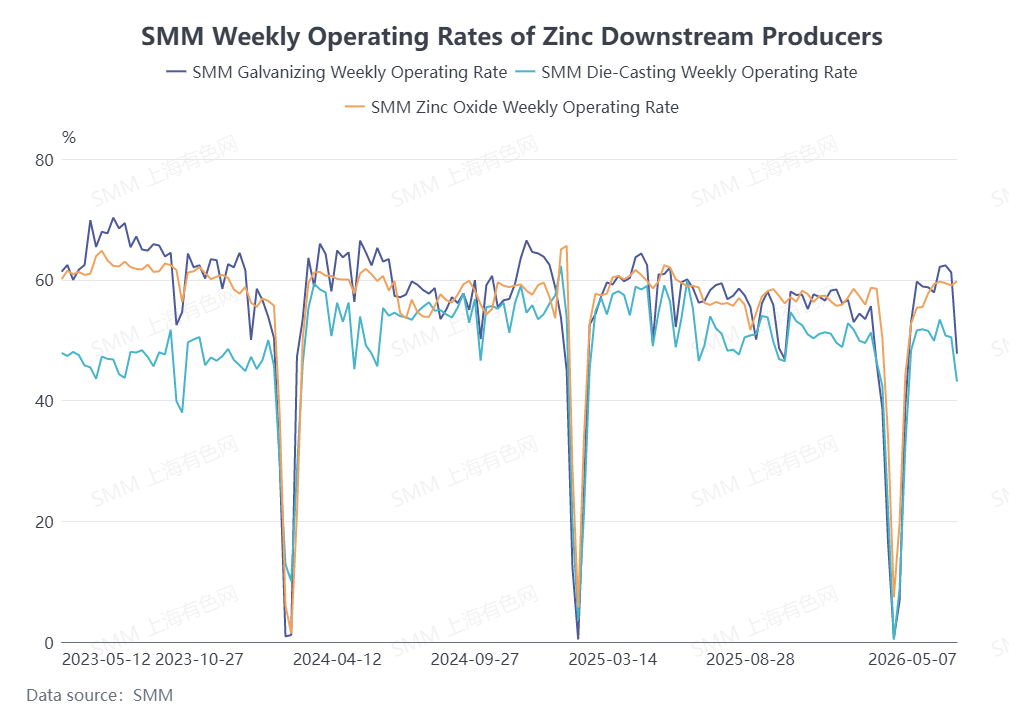

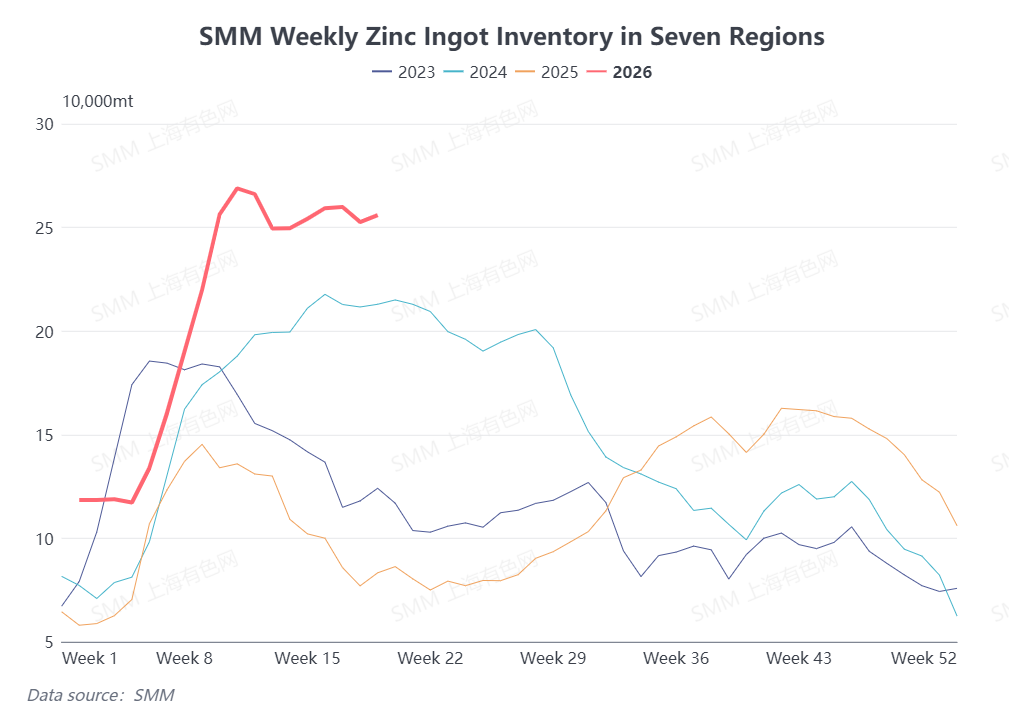

Consumption side. April coincided with China's regular peak consumption season, with end-use consumption continuing to recover. Domestic trade orders for zinc downstream improved compared to March, driving domestic consumption growth. However, heading into May, some downstream zinc enterprises halted production during the Labour Day holiday, affecting a portion of zinc ingot demand. Additionally, as the peak season gradually passes, downstream orders in China are expected to decline in May, with related operating rates falling accordingly. Combined with persistently high domestic zinc ingot inventory, overall consumption is exerting pressure on zinc prices.

Overall, from a macro perspective, the market continues to monitor progress in US-Iran negotiations. Fundamentals side, the tight ore supply situation showed no improvement in May, but smelters have not made obvious production cuts, and refined zinc supply levels remain robust. Meanwhile, consumption is expected to gradually weaken. Bullish and bearish factors coexist on the fundamentals, and continued attention should be paid to subsequent macro developments and consumption performance.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Zinc Concentrate TCs Continue to Decline, SHFE Zinc Fluctuates at Highs [SMM Zinc Futures Brief]](https://imgqn.smm.cn/usercenter/kdRPs20251217171754.jpg)