SMM, 30 апреля:

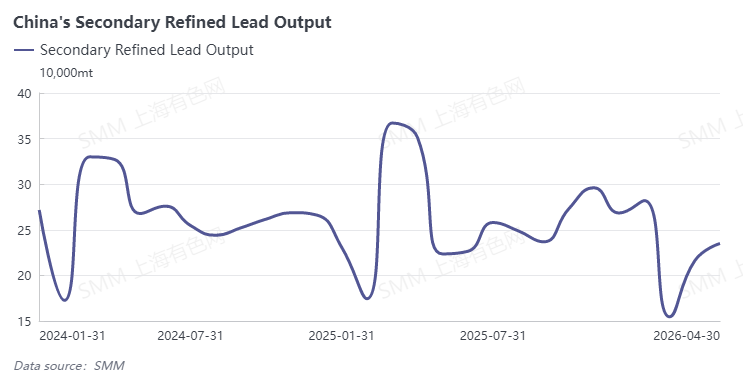

В апреле 2026 года производство вторичного свинца в Китае продемонстрировало рост к предыдущему месяцу и снижение в годовом выражении. Месячное производство вторичного свинца выросло на 12,72% м/м и снизилось на 24,61% г/г; производство вторичного рафинированного свинца выросло на 8,7% м/м и значительно снизилось на 33,14% г/г.

Рост производства в апреле был обусловлен главным образом приростом выпуска на плавильных заводах, возобновивших производство и продолживших наращивать мощности. Предприятия по выплавке вторичного свинца в Восточном, Северо-Западном, Центральном Китае и других регионах последовательно возобновляли производство с середины-конца марта и в апреле вступили в стадию наращивания мощностей, при этом загрузка стабильно росла, обеспечивая общий рост производства. В то же время ряд предприятий отрасли снижали загрузку и сокращали выпуск, что было обусловлено дефицитом сырья из отработанных аккумуляторов, высокими затратами на плавку и слабыми ценами на свинец, усугублявшими убытки, а также вялым конечным потреблением, сдерживавшим готовность заводов к производству. Тем не менее в целом прирост от возобновления производства компенсировал сокращения, и в апреле был достигнут рост к предыдущему месяцу.

В мае ожидается снижение производства вторичного свинца, месячный объём производства, по прогнозам, сократится более чем на 30 тыс. тонн. Давление со стороны предложения обусловлено двумя факторами: во-первых, несколько крупных предприятий по выплавке вторичного свинца в Восточном и Северном Китае вступают в плановые ремонтные циклы, что ведёт к поэтапному сокращению мощностей; во-вторых, заводы в большинстве регионов имеют слабые ожидания по поступлению сырья из отработанных аккумуляторов в мае, недостаточно уверены в пополнении запасов и планируют превентивное сокращение производства и снижение загрузки. Хотя отдельные заводы в Цзянси и Аньхое возобновляют или запускают производство, обеспечивая незначительное пополнение мощностей, этого недостаточно для компенсации сокращений из-за ремонтов в основных производственных районах и дефицита сырья. В целом в мае ожидается заметное снижение производства вторичного свинца.

![Фьючерс на свинец SHFE 2608 закрылся небольшим ростом, прервав четырёхдневную серию снижений; рынок в затишье с опорой на дно [Обзор фьючерсов на свинец]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![Макроэкономические риски сохраняются, следите за улучшением фундаментальных показателей; ожидается относительный отскок цен на свинец [SMM Weekly Lead Market Forecast]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)