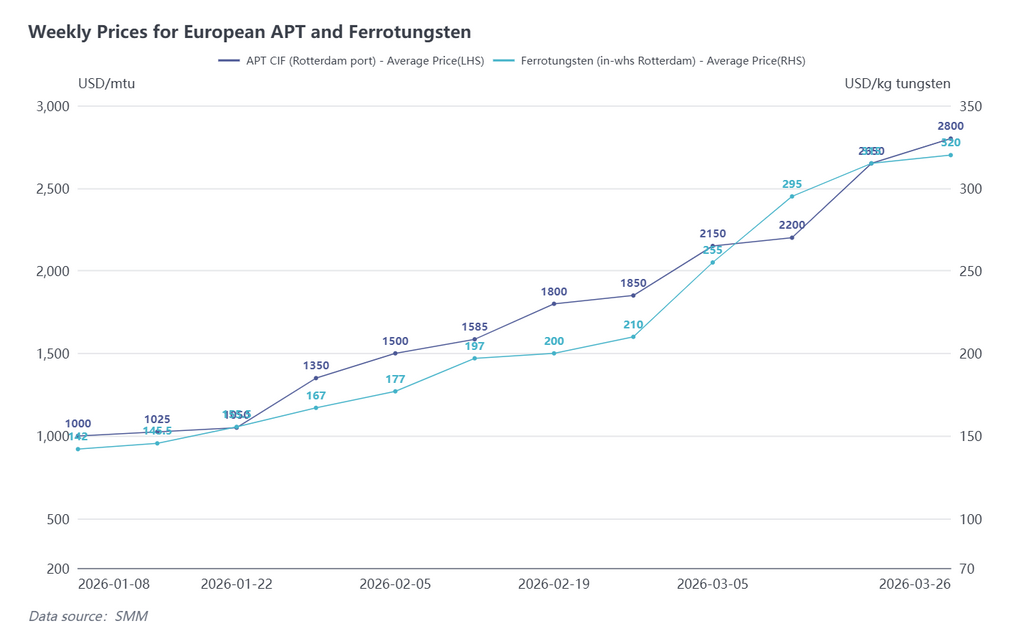

Международный рынок APT: дефицит предложения сохранялся, ценовой разрыв между внутренним и зарубежными рынками продолжил расширяться

Согласно данным SMM, по состоянию на 30 марта котировки APT на условиях CIF Роттердам составляли 2 600–3 000 долл./mtu, средняя цена — 2 800 долл./mtu, что на 150 долл. выше по сравнению с предыдущей неделей; ферровольфрам (склад в Роттердаме) котировался на уровне 310–330 долл./кг вольфрама, средняя цена — 320 долл./кг вольфрама, что на 5 долл. выше неделей ранее. В целом объём сделок на европейском рынке на прошлой неделе был ограниченным, однако дефицит сырья продолжал поддерживать умеренный рост котировок. К концу марта цены на APT в Европе в совокупности выросли на 30% по сравнению с началом месяца.

В настоящее время дефицит сырья на рынках Европы, США и Японии вряд ли ослабнет в краткосрочной перспективе. Со стороны предложения доступность APT во Вьетнаме и Индии также оставалась ограниченной, а местные объёмы APT во Вьетнаме были практически полностью распроданы. По отзывам китайских трейдеров, китайские предприятия с экспортной квалификацией в последнее время проявляли более сильную готовность к продажам, однако котировки оставались твёрдыми: предложения CIF Роттердам в целом удерживались выше 2 900 долл./mtu и в большинстве случаев требовали предоплаты. Для конечных потребителей за пределами Китая продвижение заказов шло медленно, а покупатели и продавцы продолжали согласовывать условия сделок. Кроме того, цикл экспортного одобрения и отгрузки из Китая по-прежнему занимал 3–4 месяца, что ещё больше повышало неопределённость в цепочке поставок.

Согласно опросу SMM, на внешнем по отношению к Китаю рынке APT на прошлой неделе не было заключено существенных сделок, хотя в начале марта небольшие партии уже достигали уровня 3 000 долл./mtu. Продавцы за пределами Китая уже отчётливо ощущали, что китайские поставщики становятся более агрессивными в ценовых предложениях. С точки зрения фундаментальных факторов спроса и предложения, ситуацию с дефицитом сырья в Европе и США было трудно изменить, и каждая новая сделка могла подталкивать цены вверх. По состоянию на 30 марта цена APT в Китае соответствовала примерно 2 425 долл./mtu, а ценовой разрыв с европейским рынком расширился почти до 400 долл., при этом ожидалось его дальнейшее увеличение.

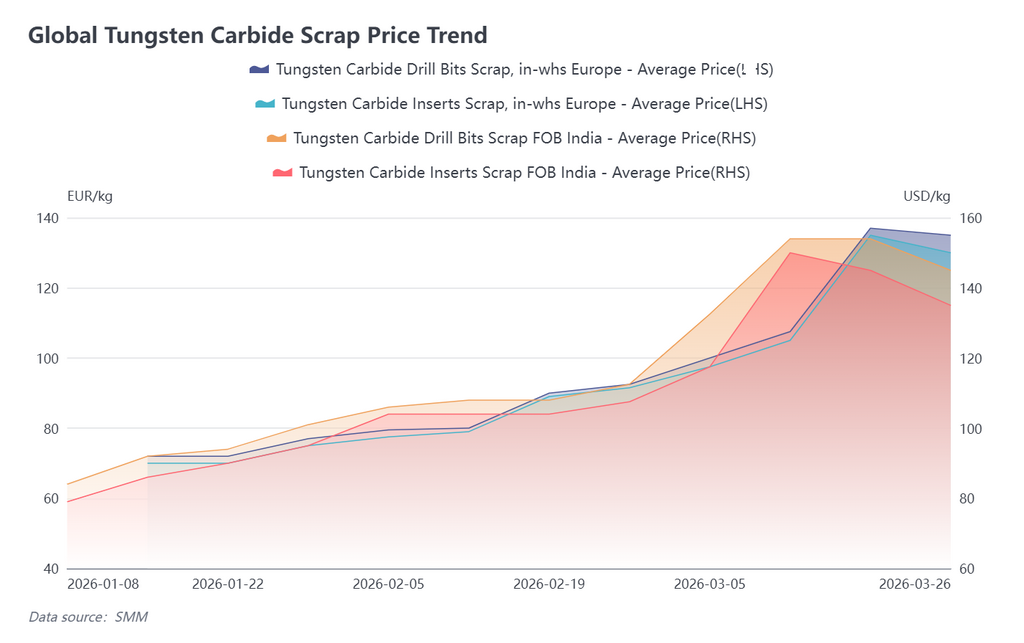

Международный рынок лома: европейский рынок вольфрамового лома колебался и стабилизировался, на индийском рынке наблюдались панические продажи

По состоянию на 26 марта европейский рынок вольфрамового лома в целом колебался и стабилизировался. Котировки на европейские твердосплавные вольфрамовые ломовые пластины составляли 125–135 евро/кг, средняя цена — 130 евро/кг, что на 5 евро ниже по сравнению с предыдущей неделей; лом вольфрамовых сверл котировался на уровне 135 евро/кг. После небольшого снижения на прошлой неделе цены на этой неделе постепенно стабилизировались. Индийский рынок вольфрамового лома, напротив, ослабевал две недели подряд: лом вольфрамовых буровых коронок котировался на условиях FOB по $140–150/кг, а лом твердосплавных вольфрамовых пластин — по $130–140/кг FOB, что на 6,8% ниже неделя к неделе.

Индийские трейдеры вольфрамового лома в основном ориентировались на китайский рынок при формировании цен. С тех пор как в середине марта цены на вольфрамовый лом в Китае начали откатываться, совокупное месячное снижение к 30 марта достигло 20%, что спровоцировало панические продажи на индийском рынке. Некоторые трейдеры, ранее удерживавшие запасы в расчете на рост, начали отгружать небольшие партии, дополнительно давя на цены. Поскольку на прошлой неделе рынок вольфрамового лома в Китае прекратил снижение и стабилизировался, ожидалось, что индийский рынок с некоторым запаздыванием последует за ним и постепенно войдет в фазу стабильности.

На европейском рынке вольфрамового лома резкий рост цен на APT в марте подстегнул ажиотажный спрос. Некоторые трейдеры в начале марта накапливали запасы в ожидании дальнейшего роста, однако под влиянием недавней коррекции цен в Китае и Индии, а также на фоне ограниченного числа сделок на рынке, в конце прошлой недели начались панические продажи, что привело к небольшому снижению цен на вольфрамовый лом в Европе. Тем не менее, поскольку фундаментальный дефицит спроса и предложения на европейском рынке сохранялся, ожидалось, что цены на вольфрамовый лом останутся высокими и будут консолидироваться либо продолжат рост.

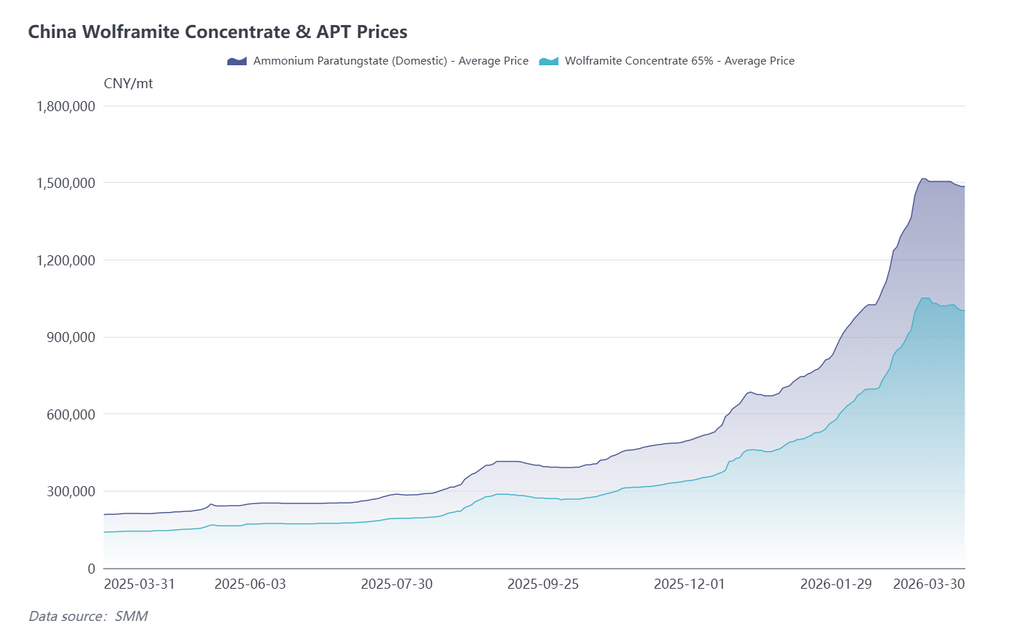

Рынок вольфрама Китая: в начале апреля вошел в фазу коррекции, публикация квот на добычу вызвала краткосрочные колебания

На прошлой неделе китайский рынок вольфрама в целом консолидировался на высоких уровнях, при этом снижение в основном сосредоточилось в сегменте руды. Поскольку к концу марта некоторые предприятия постепенно получили одобрение квот на добычу, были запущены рыночные тендеры, настроения покупателей и продавцов разошлись, а стремление покупателей сбивать цены усилилось.

Под влиянием передачи настроений из сегмента руды рынок APT на этой неделе может продолжить инерционное снижение. Хотя цены по долгосрочным контрактам оставались стабильными, настроения на рынке спотовых заказов легко нарушались колебаниями в сегменте руды, из-за чего в краткосрочной перспективе цены оставались под давлением. Порошковый сегмент и конечные потребители в downstream-секторе в целом сохраняли стабильность, ранее размещенные заказы исполнялись относительно ровно, а рынок лома уже первым прекратил снижение.

В целом китайский рынок вольфрама в начале апреля всё ещё находился в фазе коррекции, и дальнейшая динамика будет зависеть от темпов отгрузок после публикации квот на добычу руды. В краткосрочной перспективе цены могут испытывать некоторое понижательное давление. Однако фундаментальная поддержка оставалась устойчивой, и с наступлением традиционного сезона пикового спроса в апреле и мае ожидается, что в целом цены продолжат получать поддержку для роста.

Прогноз: За пределами Китая сегмент сырья демонстрировал бычьи настроения, тогда как рынок лома постепенно стабилизировался; в апреле китайский рынок войдёт в фазу коррекции, однако фундаментальные факторы спроса и предложения остаются устойчивыми, а ценовой разрыв между внутренним и зарубежными рынками в краткосрочной перспективе может продолжить расширяться. В долгосрочной перспективе китайский рынок по-прежнему сохраняет потенциал для дальнейшего роста.

![[SMM Analysis] Краткий анализ рынка импорта и экспорта вольфрама в мае](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)