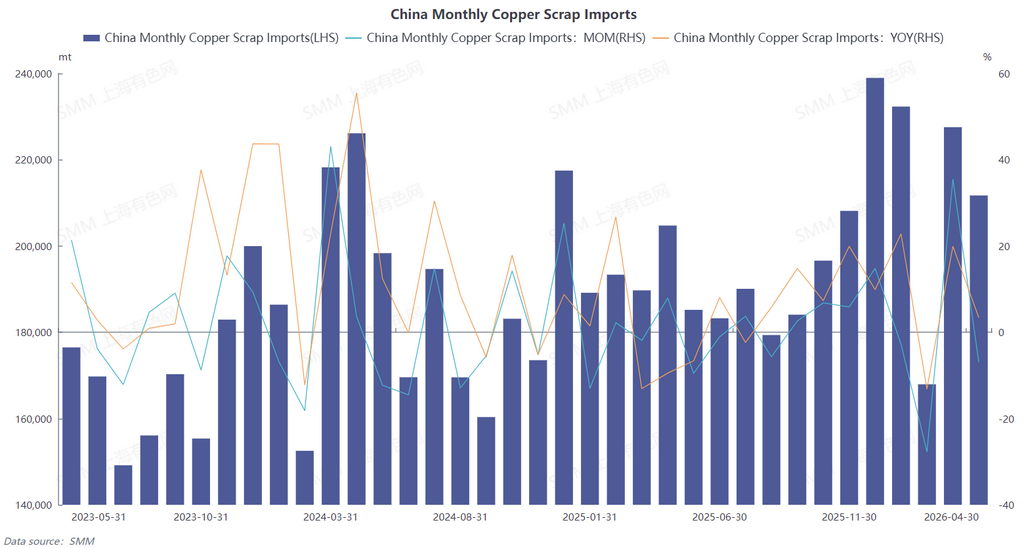

In April 2026, China imported 211,700 mt in physical content of copper scrap and shredded copper scrap, down 6.96% MoM and up 3.41% YoY. Cumulative imports from January to April 2026 reached 839,600 mt in physical content, up 8.05% YoY on a cumulative basis. (HS code: 74040000)

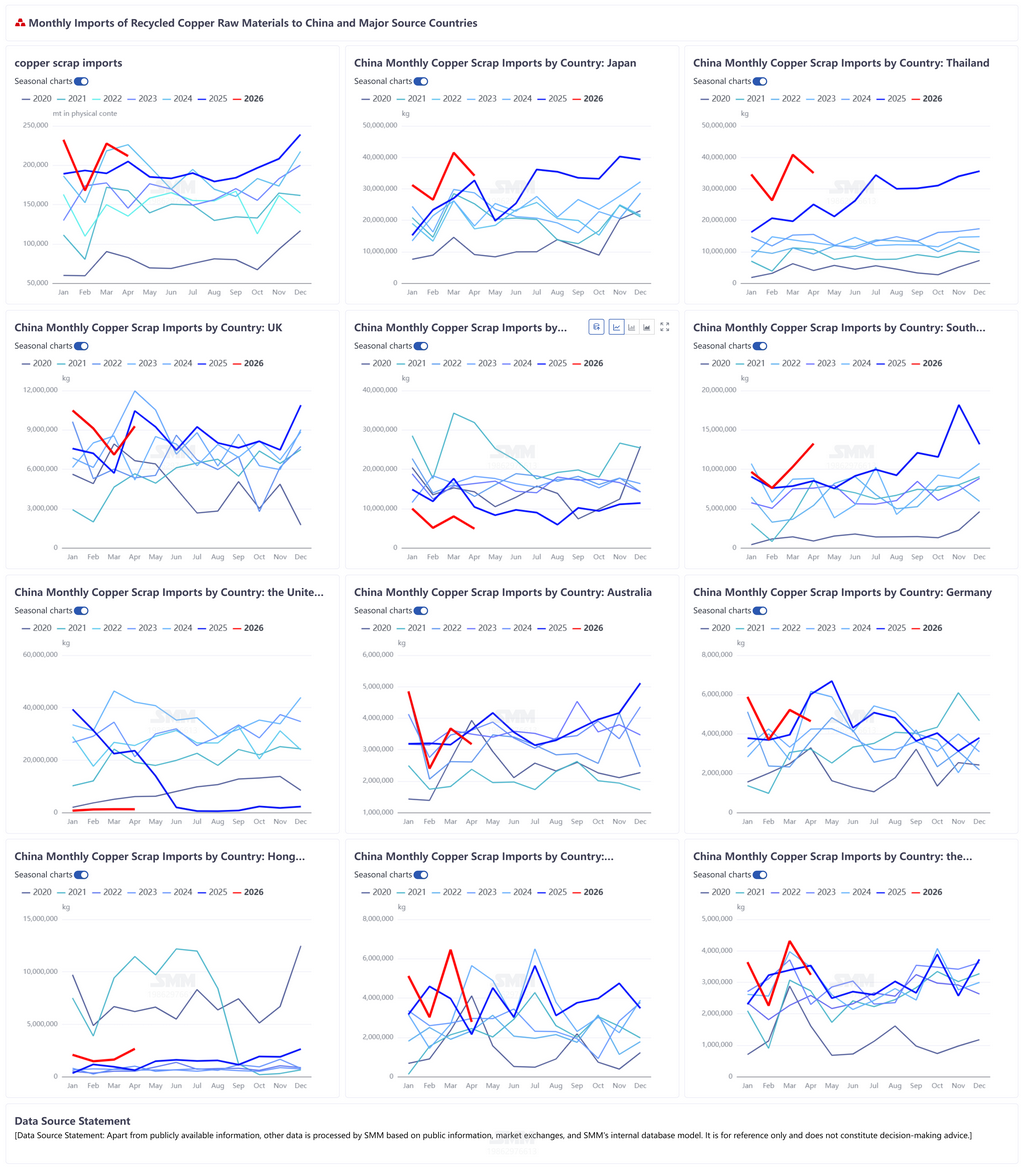

I. Top Supplier Landscape Remains Solid, Japan and Thailand Still Key Contributors

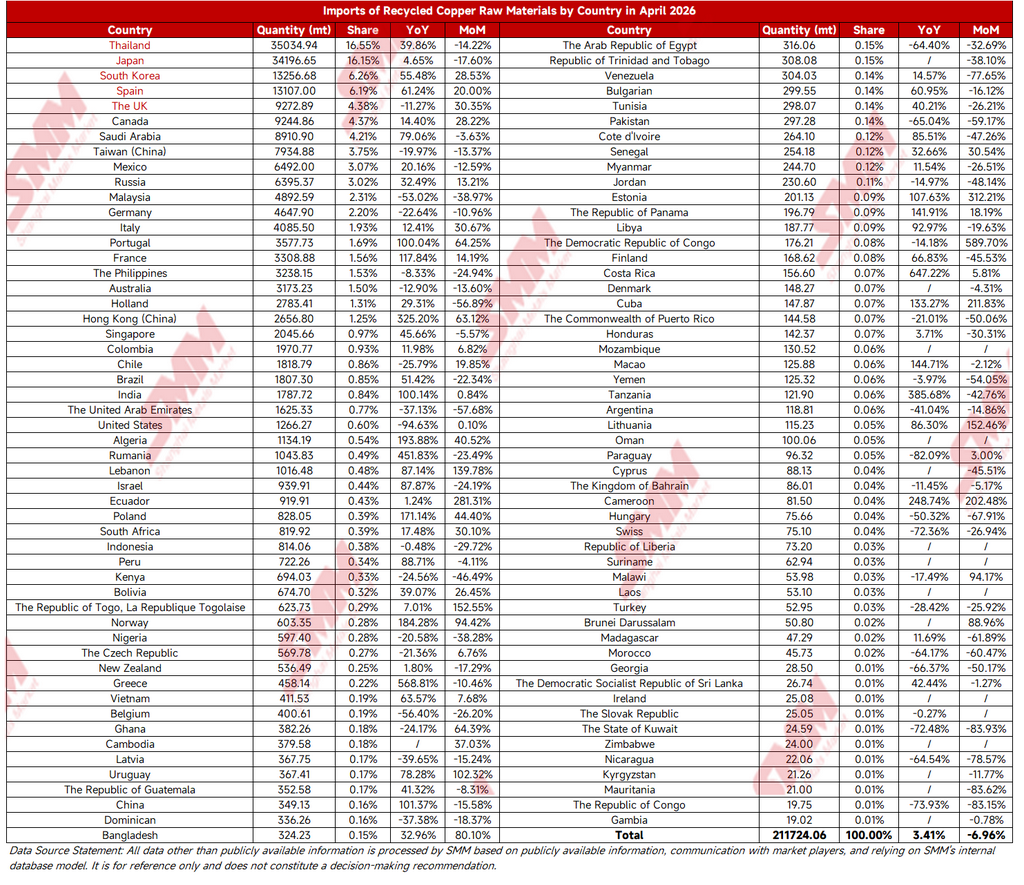

In April, the concentration of copper scrap import sources remained high, with the top three supplying countries accounting for over 40% combined:

Thailand: Exported 35,000 mt in physical content to China in April, accounting for 16.55%, up 39.86% YoY and down 14.22% MoM. It remained China's largest copper scrap import source. Despite the MoM pullback, the nearly 40% YoY growth rate was maintained, reflecting its stable supply capability.

Japan: Exported 34,200 mt in physical content to China in April, accounting for 16.15%, up 4.65% YoY and down 17.60% MoM. As the second-largest supplier, it still maintained positive YoY growth and remained an important supplementary source of copper scrap for China.

South Korea: Exported 13,300 mt in physical content to China in April, accounting for 6.26%, up 55.48% YoY and up 28.53% MoM. The impressive YoY growth rate made it one of the incremental contributors to April imports.

Among other major supplying countries, Spain, the UK, Canada, and Saudi Arabia also contributed to imports, accounting for 6.19%, 4.38%, 4.37%, and 4.21% respectively. YoY growth rates diverged significantly, with supplies from some European and American countries declining MoM.

II. Core Drivers Behind the MoM Pullback in April Imports

Narrowing import profit margins dampened purchase willingness: From late March to April, the center of copper prices continued to rebound, and ex-China secondary copper traders showed strong sentiment to hold prices firm. The bare bright copper pricing coefficient against LME remained in a high range for an extended period, with procurement costs continuing to rise. Meanwhile, domestic downstream processing enterprises had limited acceptance of high-priced copper scrap and showed strong willingness to push for lower prices. The profit margin on imported copper scrap narrowed compared to the previous period, which was one of the reasons for the MoM pullback in imports.

Phased export decline from some core supplying countries: Thailand and Japan, the top two suppliers, both saw MoM declines in exports to China in April, with Thailand down 14.22% MoM and Japan down 17.60% MoM. Although their combined share still exceeded 30%, the MoM incremental growth disappeared, weakening their support for overall imports. Meanwhile, some traditional suppliers such as Malaysia, Germany, and Italy also experienced MoM declines, amplifying the overall pullback in imports.

III. Reasons Supporting Continued YoY Growth in Imports

The structural shortage of tax-inclusive copper scrap in China remained unresolved. The core market contradiction in April continued from the previous period: invoice issues had not been substantially improved, domestic tax-invoiced copper scrap circulation remained persistently tight, and domestic trade prices stayed high. From March to April, spot prices of imported bare bright copper in Zhejiang maintained fluctuating at highs, with discounts against futures contract basically stable in the range of 300-800 yuan/mt. Against this backdrop, downstream compliant enterprises' rigid demand for imported tax-invoiced copper scrap remained strong to meet production and tax compliance requirements, and imported sources remained a key channel to fill the domestic supply gap.

Looking ahead to May, as the domestic peak consumption season draws to a close, downstream operating rates are expected to pull back marginally. Combined with the difficulty in restoring import profit margins amid high copper prices outside China, copper scrap imports are expected to remain in the doldrums. However, given that the structural shortage of tax-inclusive copper scrap in China is unlikely to be resolved in the short term, and some emerging supplying countries' export potential is still being released, the likelihood of a sharp decline in imports is relatively small, and the overall volume is expected to hover at highs. (Detailed breakdown of April copper scrap imports by country is attached below)

![Downstream Operating Rates Declined and Procurement Volume Decreased, Spot Trades Were Inactive [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/FSTyq20251217171713.jpg)

![Suppliers Concentrated Shipments, Spot Premiums Continued to Decline [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)