SMM News, July 15:

Metal market:

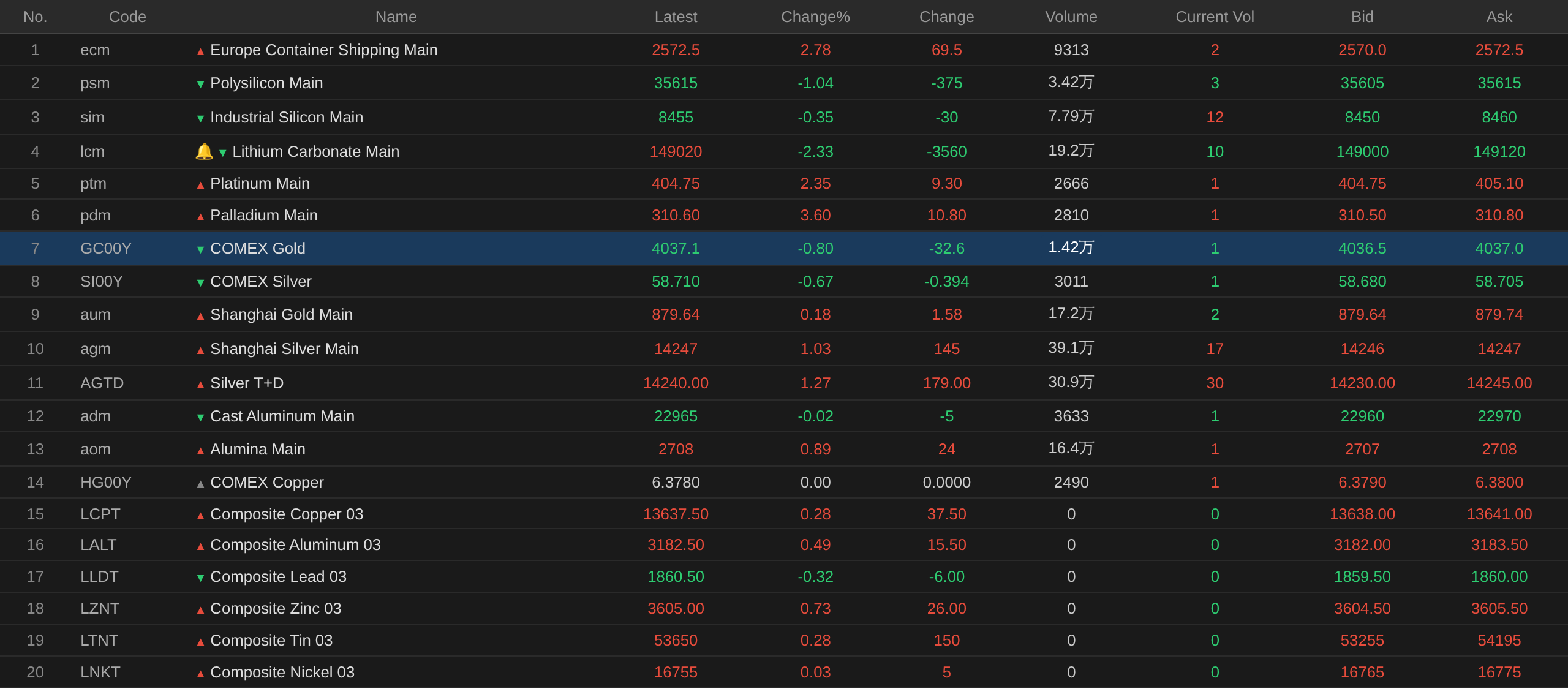

As of the midday close, domestic base metals showed mixed performance, with SHFE copper rising 0.57%, SHFE aluminum edging down, SHFE lead falling 1.8%, SHFE zinc up 0.45%, SHFE tin up 1.36%, and SHFE nickel down 0.43%.

Furthermore, aluminum casting most-traded futures edged down, alumina most-traded rose 0.89%, lithium carbonate most-traded fell 2.33%, silicon metal most-traded fell 0.35%, and polysilicon most-traded futures fell 1.04%.

Ferrous metals all rose. Iron ore rose 1.13%, rebar rose 1.24%, hot-rolled coil rose 1.09%, and stainless steel rose 0.76%. Coking coal and coke: The most-traded coking coal contract rose 2.12%, and the most-traded coke contract rose 1.1%.

Overseas base metal market: As of 11:42, LME metals nearly all rose. LME copper rose 0.28%, LME aluminum rose 0.49%, LME lead fell 0.32%, LME zinc rose 0.73%, LME tin rose 0.28%, and LME nickel edged up.

Precious metals: As of 11:42, COMEX gold fell 0.8%, and COMEX silver fell 0.67%. Domestic precious metals: SHFE gold rose 0.18%; SHFE silver most-traded rose 1.03%.

Furthermore, as of the midday close, platinum most-traded futures rose 2.35%, and palladium most-traded futures rose 3.6%.

As of the midday close, the most-traded Europe shipping futures contract rose 2.78% to 2,572.5 points.

As of 11:42 on July 15, some futures midday quotes:

Spot and Fundamentals

Copper: Today, Guangdong #1 copper cathode spot against the front-month contract: High-quality copper was quoted at 80 yuan/mt, flat with the previous trading day; standard-quality copper was quoted at a discount of 20 yuan/mt, flat with the previous trading day; SX-EW copper was quoted at a discount of 80 yuan/mt, flat with the previous trading day. The average price of Guangdong #1 copper cathode was 105,205 yuan/mt, up 1,100 yuan/mt from the previous trading day, and the average price of SX-EW copper was 105,095 yuan/mt, up 1,085 yuan/mt from the previous trading day. Spot market: Guangdong inventory ended a two-session rising streak and fell again today, mainly due to reduced arrivals...

Macro Front

Domestic:

[National Bureau of Statistics (NBS): H1 GDP rose 4.7% YoY; national economy operated within a reasonable range; new momentum grew rapidly] The National Bureau of Statistics (NBS) released data showing that, according to preliminary estimates, H1 GDP reached 69,570.4 billion yuan, up 4.7% YoY at constant prices. By industry, the value added of the primary industry was 3,152.2 billion yuan, up 3.7% YoY; the secondary industry was 25,047.3 billion yuan, up 3.9%; and the tertiary industry was 41,370.9 billion yuan, up 5.2%. By quarter, Q1 GDP grew 5.0% YoY and Q2 grew 4.3%. On a QoQ basis, Q2 GDP rose 0.9%. Overall, the national economy operated within a reasonable range in H1, with new quality productive forces cultivated and strengthened and high-quality development progressing toward new heights of quality. At the same time, we must recognize that external instabilities and uncertainties are mounting, the contradiction between strong supply and weak demand in China remains pronounced, and the foundation for economic improvement still needs consolidation. In the next phase, we will adhere to the principle of seeking progress while maintaining stability, improving quality and efficiency, intensify counter-cyclical and cross-cyclical adjustments, continue to expand domestic demand and optimize supply, enhance growth and revitalize existing assets, focus on building a strong Chinese market, accelerate the cultivation and strengthening of new momentum, step up efforts to stabilize employment, enterprises, markets, and expectations, and promote the effective improvement of quality and reasonable growth of quantity in the economy.

[PBOC reverse repo operations achieved a net injection of 911.5 billion yuan on the day] The PBOC conducted 426.5 billion yuan of 7-day reverse repo operations and 1,400 billion yuan of 6-month outright reverse repo operations today. With 15 billion yuan of 7-day reverse repos and 900 billion yuan of outright reverse repos maturing today, the operations resulted in a net injection of 911.5 billion yuan on the day.

US dollar:

As of 11:42, the US dollar index extended the previous trading day's decline, falling 0.11% to 100.83. Data: A key turning point signal emerged in US inflation. June CPI recorded its first MoM decline in six years, while core inflation was basically flat, prompting the market to dramatically scale back bets on a July rate hike by the US Fed. On Tuesday, data released by the US Bureau of Labor Statistics showed that the June Consumer Price Index (CPI) rose 3.5% YoY, below market expectations of 3.8% and a significant pullback from the prior reading of 4.2%. Core CPI rose 2.6% YoY, also below expectations of 2.8% and the prior reading of 2.9%. (Wall Street See)

According to CME "FedWatch": The probability of the US Fed holding rates steady in July is 84.5%, while the probability of a cumulative 25-basis-point rate hike is 15.5%. For September, the probability of holding rates steady is 42.2%, the probability of a cumulative 25-basis-point hike is 50%, and the probability of a cumulative 50-basis-point hike is 7.8%. (Jin10 Data APP)

Fed Chairman Walsh stated that he places equal emphasis on the Fed's employment and inflation mandates—a point he has repeatedly stressed since assuming the role of Fed Chairman. "In the mandate you have given us, we do not favor one part over the other," Walsh told members of the House Financial Services Committee. "Price stability and full employment are not trade-offs. I am committed to achieving both. When later asked if he supported targeted measures to address the unemployment rate and employment opportunity gaps between Black and White Americans, Walsh stated: "The US must not leave anyone behind. Economic opportunity is critical to the trajectory of growth for the US over the next five to ten years, meaning every American needs the opportunity to be productive." (Jin10 Data APP)

A CICC research note indicated that US June CPI fell 0.4% MoM on a seasonally adjusted basis, with YoY growth pulling back to 3.5%; core CPI was flat MoM and up 2.6% YoY, both below market expectations. The decline in energy prices was the main driver of cooling inflation. Looking ahead, as tensions escalate again between the US and Iran, the outlook for energy inflation remains uncertain. Meanwhile, the AI inflation effect is gradually materializing, with upstream hardware supply-demand mismatch, rising prices for software and related products, and AI capex boosting aggregate demand all potentially making core inflation stickier. For policy, the cooling inflation data in June supports the Fed holding rates steady at its July meeting, but recent remarks by Waller suggest [1] the Fed is reassessing the possibility of a "preventive rate hike." We maintain our base case of no rate hikes for the year, but flag that the bar for hiking has already fallen. If one or two hotter-than-expected inflation prints emerge, it could push the Fed to further discuss rate hike options.

A CITIC Securities research note stated that US June CPI came in below expectations across the board, retail gas prices fell, core services inflation was flat MoM, and the second-round inflation effect was minimal. CITIC Securities believes US inflation is not sticky, noting that headline CPI YoY has definitively passed its cycle peak and is expected to trend mildly downward in Q3, hit bottom in September, rise to a secondary peak around year-end, and then decline rapidly next March. CITIC Securities still expects the Fed to stay on hold for the full year, sees room for derivative-priced rate hike expectations to be revised further down, considers US Treasuries currently unsuitable for allocation-based opportunities—with short-dated bonds better than long-dated ones—and believes the US dollar index faces difficulty sustaining upward momentum but has support, while the technology-driven theme in US equities retains its appeal.

On the data front:

Today will see the release of figures including China's June total electricity consumption YoY, China's June total electricity consumption, the US June PPI annual rate, the US June PPI monthly rate, the US July New York Fed Empire State Manufacturing Index, the Eurozone May industrial output MoM rate, Canada's May wholesale sales MoM rate, and the Bank of Canada's interest rate decision as of July 15.

Additionally, attention needs to be paid to: the National Bureau of Statistics (NBS) releasing the monthly report on residential selling prices in 70 large and medium-sized cities; the State Council Information Office holding a press conference on the state of the economy; the State Council Information Office holding a press conference to brief on the execution of monetary policy and financial statistics for H1 2026; the National Energy Administration releasing total electricity consumption data around the 15th of each month. Fed Governor Barr spoke on artificial intelligence at the Fed’s annual financial inclusion conference; 2027 FOMC voting member and Chicago Fed President Goolsbee participated in a fireside chat; Fed Governor Lisa Cook delivered remarks at the Fed’s annual financial inclusion conference; Fed Governor Bowman also spoke at the same conference; permanent FOMC voting member and New York Fed President Williams gave a speech; Fed Chair Warsh attended the Senate Banking, Housing, and Urban Affairs Committee hearing on the Fed’s Semi-annual Monetary Policy Report; Bank of England Governor Bailey spoke; the Bank of Canada announced its interest rate decision and monetary policy report, and Bank of Canada Governor Macklem and Senior Deputy Governor Rogers held a monetary policy press conference. ASML published its Q2 2026 financial report.

Crude oil:

As of 11:42, both benchmarks rose, with WTI up 1.02% and Brent up 1.32%.

Despite improved risk sentiment from cooling inflation, the crude oil market remains driven by geopolitics. The US announced the reinstatement of a naval blockade on vessels transiting Iranian ports and coastal areas, with escalating Middle East tensions supporting oil prices. Meanwhile, the US and European refined product markets are historically tight, heightened Middle East strains have fanned fuel supply concerns, and high oil prices continue to pressure consumers. Goldman’s Privorotsky believes Brent around $85 itself is manageable, the real story is in refined products, distillates rather than crude oil are the true inflation signal, and heating oil futures have hit new highs since the conflict erupted, highlighting tightness in the product market, with any further disruption disproportionately hitting inflation. (Wall Street CN)

Additionally, Iran’s Islamic Revolutionary Guard Corps said in a statement on the 15th that as long as the US continues attacks on Iran, the region will not export “a drop of oil” or natural gas. (Xinhua)

Spot market overview:

►

►

►

►

►

►

►

►

►

►

►

►

►

►

![[Live] Analysis of Power Cable Development Patterns in the 15th Five-Year Plan, Copper and Aluminum Market Analysis, Exploring Opportunities in the Middle East and Africa, and Outlook for PV Enamelled Wire](https://imgqn.smm.cn/usercenter/oeWiG20251217171714.jpeg)

![Copper Futures and Spot Price Fluctuations and the Current Status of the Wire and Cable Industry [South China Cable Conference]](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)