On July 15, at the , hosted by SMM Information & Technology Co., Ltd. and Shandong Aisi Information Technology Co., Ltd., co-organized by Guangxi Dasheng Power Equipment Co., Ltd., and strongly supported by Solarabic, a Middle Eastern new energy industry media, and the Guangdong Province Industrial and Trade Development Promotion Association, Shenzhen Bendakang Cable Co., Ltd. Chairman Hou Shaofan shared insights on “Copper Spot and Futures Price Fluctuations and the Status Quo of the Wire and Cable Industry”.

Macro Insights: Global and Regional Copper Consumption Patterns

2026 Global and China Copper Consumption Overview

► Global copper cathode consumption grows mildly, supply-demand pattern tightens

Global copper cathode consumption is expected to reach around 25 million mt in 2026, up 1.6% YoY. NEVs, PV and wind power, and AI computing centers become core drivers. The market will see a supply deficit, with ore supply tightness persisting.

► China's copper consumption leads the globe, driven by emerging fields

China accounts for half of global copper consumption. Its apparent consumption is set to exceed 13 million mt in 2026, up around 2% YoY, leading the world. Power grid investment, new energy, and AI data centers are the core drivers. Demand in emerging sectors is robust, while growth in traditional sectors is slowing down.

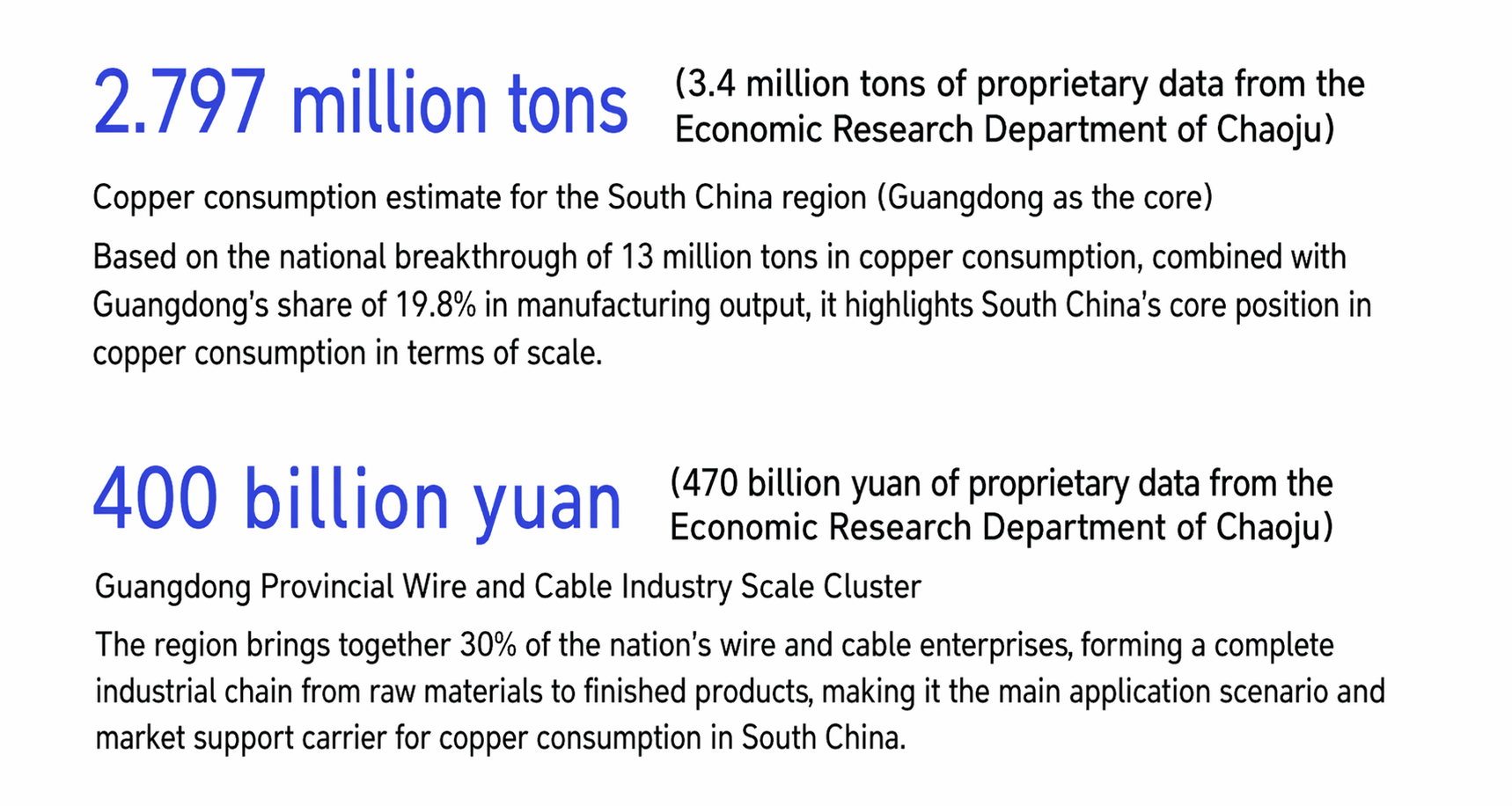

South China: A Growth Pole Driven by Export-Oriented and Emerging Momentum

South China, especially Guangdong Province, as one of the core engines of China's manufacturing, exhibits a distinct "export-oriented" and "emerging momentum-driven" copper consumption structure. It closely relies on downstream industries such as electronic information and NEVs, with a notable export orientation, making it a key growth pole for domestic copper consumption.

Regional Pattern: An Analysis of the Industrial Gap Between South China and East China

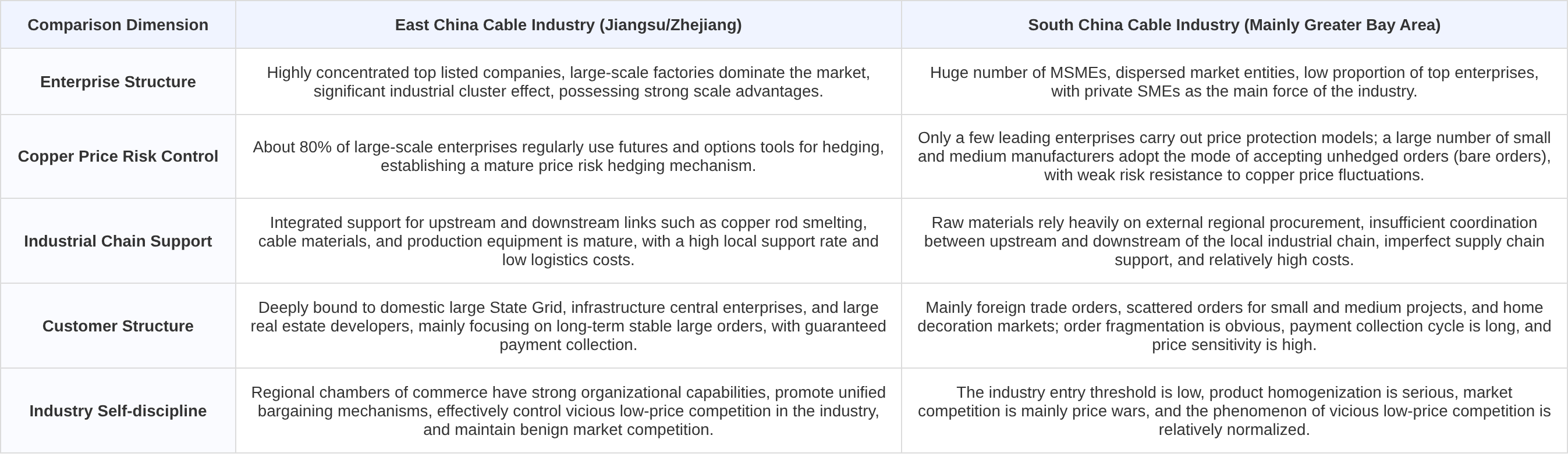

North-South Industrial Divergence: Five Core Gaps Between South China and East China's Wire and Cable Industries

► In-depth Analysis of Regional Industrial Development Models and Core Competitiveness

From five dimensions – enterprise structure, risk management, industry chain support, client resources, and industry ecosystem – the current development status of the wire and cable industries in the two regions is compared, revealing the underlying logic and development pain points behind the industrial divergence.

Industry Growing Pains: In-depth Analysis of Three Core Pain Points

Pain Point 1: Party A's "Imposed Terms" – Imbalanced Bargaining Power

01 Excessively long payment cycles; 02 "Back-to-back" payment terms shifting risk; 03 High security deposits squeezing capital; 04 Fixed prices disregarding cost fluctuations.

Pain Point 2: Wild Swings in Copper Prices – The Risk of "High-Cost In, Low-Price Out" Losses

01 Two-way risk: both sharp rises and falls put pressure on; 02 Transmission lag: the core crux of losses; 03 Breakthrough solution: using financial instruments to build a solid defense.

Pain Point Three: Industry Price Involution — the Meager Profit Dilemma of Being "Cheaper than Vermicelli"

►01 Fierce Price War: Survival Struggle in the Quagmire of Meager Profits

The industry presents a pattern of “big industry, small enterprises,” with CR10 below 12%, over 90% being small and medium-sized enterprises, and the market highly fragmented. The price war in the low and mid-end cable sector is intensifying, even giving rise to the industry joke of being “cheaper than vermicelli,” directly resulting in the industry’s average net profit margin falling below 3%. Small and medium-sized enterprises are trapped in a survival dilemma with meager profits, or even negative profits.

►02 Vicious Cycle: The Industry Paradox of Bad Money Driving Out Good

Low-price competition forces some enterprises to cut corners, causing product quality and safety risks. More seriously, substandard cable products directly threaten public property safety and even pose significant risks to the lives of the public. Entrepreneurs (this great group of people) who originally immersed themselves in industry with a craftsman’s spirit and aspired to contribute to social and economic development, once they breach the quality bottom line in the low-price involution, not only harm users and society but ultimately violate the law, end up imprisoned, and cause an irreparable tragedy. Meager profits prevent enterprises from investing in R&D and innovation, trapping them in a vicious cycle of “low price—low quality—even lower profits.” Meanwhile, the industry’s low-end capacity is severely surplus, while the high-end market has long been dominated by foreign brands, with technical barriers difficult to overcome.

Future Outlook: Industry Chain Synergy and Development Trends

Grasp the Industry Pulse · Co-Build a Synergistic Ecosystem · Open a New Chapter of Cooperation

Based on the new stage of industrial development, we start from three dimensions—trend analysis, synergistic co-construction, and cooperation opportunities—to analyze the future direction of the copper wire and cable industry. The aim is to build industry consensus, promote deep integration of the upstream and downstream, and through institutional innovation and resource integration, build a safe, stable, and win-win new pattern of industrial development.

01 Industry Trends: Growth and Standardization

Demand side benefits from the dual drivers of new energy and new infrastructure, with market growth continuously released; risk control side sees derivative tools becoming standard, with bare position models gradually phased out; the industry landscape is accelerating toward concentration among large-scale, compliant leading enterprises, with the Matthew effect prominent.

02 Synergy Initiatives: Shared Responsibility and Joint Governance

We advocate for the industry-wide adoption of a copper price-linked adjustment mechanism to share price fluctuation risks; collaborate with financial institutions to promote the “option hedging + performance guarantee” model to build operational defenses; establish an industry alliance to unify pricing floors, resist low-price involution, and share risk control and market resources.

03 Cooperation Invitation: Openness and Win-Win

Provide stable batch supply of national standard cables for PV, power grid, and new energy supporting applications; connect with professional institutions to offer copper option price insurance consulting and financial guarantee services; sincerely invite copper enterprises, financial institutions, and EPC contractors to engage in long-term strategic joint ventures to jointly create industry value.

In addition, they shared the breakthrough path: Bendakang practical cases and solutions from such perspectives as Bendakang Cable—from scale leadership to value guidance; financial innovation practice: the "option price protection" policy, empowering industry chain win-win; practical reference: Bendakang's combined strategy of "option price protection + performance bond"; innovation engine: a high-end and intelligent product matrix; smart manufacturing upgrade: digitally driven lean production practice, etc.

![[SMM Analysis]U.S. Restricts Critical Mineral Scrap Exports — Could Copper Scrap Be Next?](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)