SMM July 13:

Metals market:

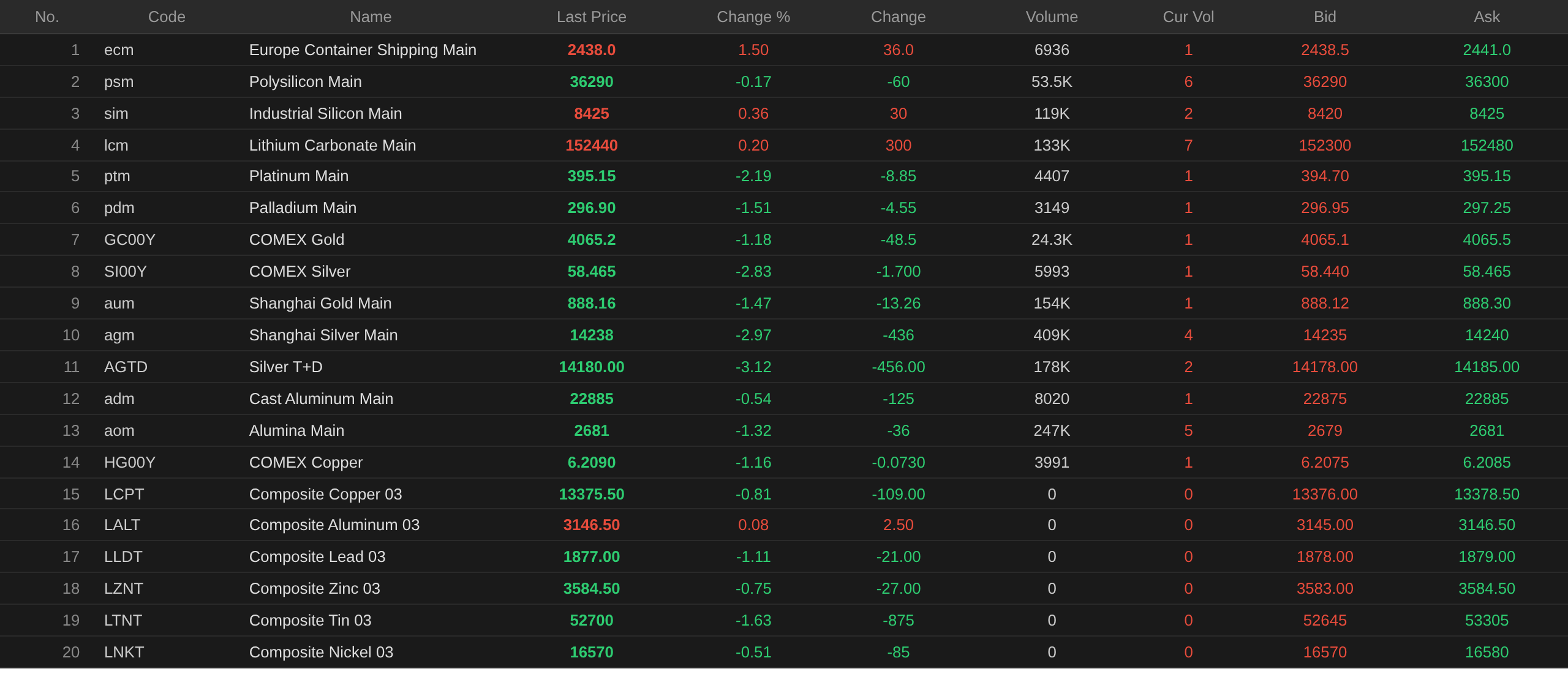

As of the midday break, the domestic base metals nearly all fell, with SHFE copper down 0.78%, SHFE aluminum down 0.37%, SHFE lead down 0.62%, SHFE zinc down 0.68%, SHFE tin down 1.51%, and SHFE nickel up 0.02%.

Additionally, the most-traded cast aluminum futures contract fell 0.54%, the most-traded alumina contract fell 1.32%, the most-traded lithium carbonate contract rose 0.2%, the most-traded silicon metal contract rose 0.36%, and the most-traded polysilicon futures contract fell 0.17%.

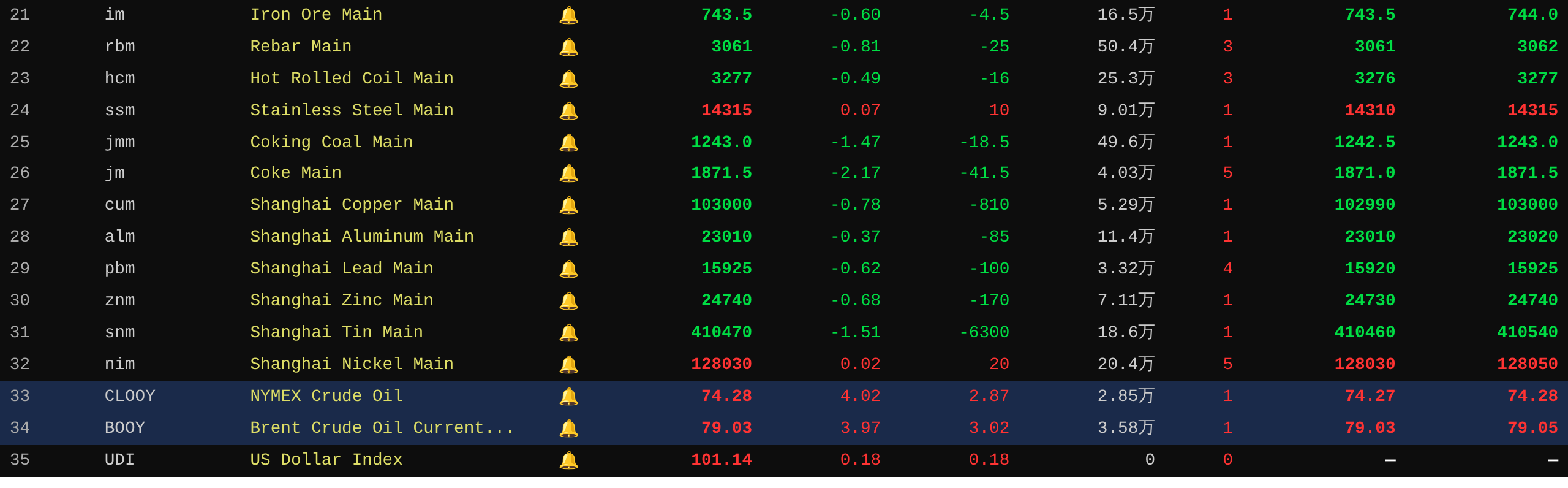

Ferrous metals mostly fell. Iron ore fell 0.6%, rebar fell 0.81%, hot-rolled coil fell 0.49%, and stainless steel edged up 0.07%. In coking coal and coke, the most-traded coking coal contract fell 1.47% and the most-traded coke contract fell 2.17%.

In overseas base metals, as of 11:47, LME metals mostly fell, with LME copper down 0.81%, LME aluminum edged up 0.08%, LME lead down 1.11%, LME zinc down 0.75%, LME tin down 1.63%, and LME nickel down 0.51%.

In precious metals, as of 11:47, COMEX gold fell 1.18% and COMEX silver fell 2.83%. In domestic precious metals, SHFE gold fell 1.47% and the most-traded SHFE silver contract fell 2.97%.

Additionally, as of the midday break, the most-traded platinum futures contract fell 2.19% and the most-traded palladium futures contract fell 1.51%.

As of the midday break, the most-traded container shipping futures (Europe route) contract rose 1.5% to 2,438 points.

As of 11:47 on July 13, midday quotes for selected futures:

Spot and fundamentals

Copper: Today, for Guangdong #1 copper cathode spot against the front-month contract: high-quality copper was quoted at 80 yuan/mt, down 30 yuan/mt from the previous trading day; standard-quality copper was quoted at a discount of 10 yuan/mt, down 60 yuan/mt from the previous trading day; and SX-EW copper was quoted at a discount of 80 yuan/mt, down 70 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 103,320 yuan/mt, down 710 yuan/mt from the previous trading day, and the average price of SX-EW copper was 103,215 yuan/mt, down 725 yuan/mt. Spot market: After the weekend, Guangdong inventory finally ended its seven consecutive declines…

Macro front

China:

[Preview: The State Council Information Office will hold a press conference on the improvement of the natural resource asset management system on Tuesday, July 14, 2026, at 3:00 PM.] The State Council Information Office will hold a press conference at 3:00 PM on Tuesday, July 14, 2026, with Vice Minister of Natural Resources Zhang Wentong and Deputy Director of the National Forestry and Grassland Administration (National Park Administration) Zhang Liming briefing on the improvement of the natural resource asset management system and taking questions from the media.

[PBOC Reverse Repo Operation Achieves Net Injection of 217 Billion Yuan on the Day]The PBOC conducted a 224 billion yuan 7-day reverse repo operation today. With 7 billion yuan in 7-day reverse repos maturing today, the day saw a net injection of 217 billion yuan. (Jin10 Data App)

Regarding the US Dollar:

As of 11:47, the US dollar index rose 0.18% to 101.14. The surge in oil prices reignited market concerns over inflation. The previous week, oil prices had already recorded their largest weekly gain since mid-May. Traders subsequently ramped up bets on further monetary policy tightening by the US Fed—the interest rate swap market is now pricing in a cumulative Fed rate hike of nearly 40 basis points by December, a significant increase from about 15 basis points in early June. (Wall Street CN)

A Wall Street Journal survey of economists this month shows the impact of the conflict with Iran on the US economy is far smaller than economists previously feared. However, the bad news is that the conflict has made inflation, already well above the Fed’s 2% target, more entrenched and has deprived the Fed of room to cut interest rates. Compared with the April survey, conducted about a month after the conflict erupted, economists’ views have shifted markedly. Forecasters now expect the US economy to grow by 2.1% this year, measured by inflation-adjusted gross domestic product from Q4 2025 to Q4 2026, up from the 2% estimate in April. The average probability of a recession within the next 12 months expected by economists fell to 25% from 33% in April, the lowest level since early 2025. Yet, improved growth prospects have been accompanied by growing inflation concerns. Economists expect consumer price index inflation to be 3.4% over the 12 months ending in December, up from 3.2% in the April survey. Inflation worries have extended beyond the war-driven boost to energy costs. Economists predict the personal consumption expenditures price index excluding food and energy, a gauge closely watched by Fed officials, will rise 3.2% in 2026, higher than the 2.9% forecast in April. (Jin10 Data App)

According to CME "FedWatch": The probability of the US Fed maintaining the current interest rate in July is 62.1%, and the probability of a cumulative 25-basis-point rate hike is 37.9%. The probability of the Fed maintaining the current rate through September is 26.4%, that of a cumulative 25-basis-point hike is 51.8%, and that of a cumulative 50-basis-point hike is 21.8%. (Jin10 Data App)

Investors will focus on the semi-annual testimony of the new Fed Chairman, Kevin Warsh, before Congress on Tuesday and Wednesday for his latest views on inflation and interest rates, as well as updates on the progress of his plan to reform the Fed. Warsh is likely to be questioned by lawmakers about his extensive plan to reform the US Fed. The Fed previously announced the appointment list for the five working groups Warsh established to evaluate everything from communication methods to the size of the balance sheet. Ian Lyngen, head of US rates strategy at BMO Capital Markets, said investors will focus on Warsh’s testimony for more details and guidance on how the chair constructs the overall state of the US economy and Fed policy. The market is currently in a state of low volume and low confidence, at least until Tuesday’s inflation data and Warsh’s testimony are released. (Jinshi Data APP)

On the data front:

Today will see the release of China’s June M2 money supply YoY, China’s June year-to-date new yuan loans, and China’s June year-to-date incremental social financing, among other data. Also, attention should be paid to Fed Governor Bowman’s speech on “Modernizing Financial Regulation.”

On the crude oil front:

As of 11:47, oil prices on both sides are up, with WTI up 4.02% and Brent up 3.97%. Uncertainty over the situation in the Strait of Hormuz is directly driving oil prices higher. (Wall Street CN)

Separately, Iraq's prime minister will visit Washington on Monday to deepen strategic ties with the US, with oil and gas agreements expected to be signed as part of a broader effort to boost economic, trade, and investment cooperation. Amid the ongoing US-Iran military escalation, Iraq has been seeking to balance its ties with neighboring Iran and the US. "The agreements to be signed will include multiple memoranda of understanding in the oil and gas sector, and Iraq is preparing to bring in a number of American companies to provide momentum for raising oil capacity," said Iraqi government spokesperson Hader Al-Abudi. The planned oil and gas agreements will also seek to open alternative export channels to reduce Iraq’s exposure should the Strait of Hormuz be disrupted, the Iraqi National News Agency quoted Al-Abudi as saying. Like other Gulf producers, Iraq suffered a drop in oil revenues during the US-Iran war due to the physical closure of this critical waterway. (Jinshi Data APP)

Spot Market at a Glance:

►

►

►

►

►

►

►

►

►

►

►

►

►

![September Rate Hike Probability Plummets to 22%, Low Inventory + Easing Trade Dual Drivers Resurface [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/BaCbN20251217171752.jpg)

![Hard Supply Gap Supports Floor Price, Macro Swings Dominate Short-Term Pace [SMM Tin Morning Briefing]](https://imgqn.smm.cn/usercenter/qWcEp20251217171751.jpeg)

![Delivery Inventory Buildup Pressures, Short-Term Lead Prices Will Consolidate on a Subdued Note [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)