SMM July 10 News:

In H1 2026, the silicon-based anode material market, driven by end-user demand for high energy density, saw dual improvements in both capacity and shipments. However, constrained by technical barriers and client certification cycles, the market exhibited a clear structural divergence characterized by "high-end tightness and low-end surplus."

I. Review of the Market Landscape in H1 2026

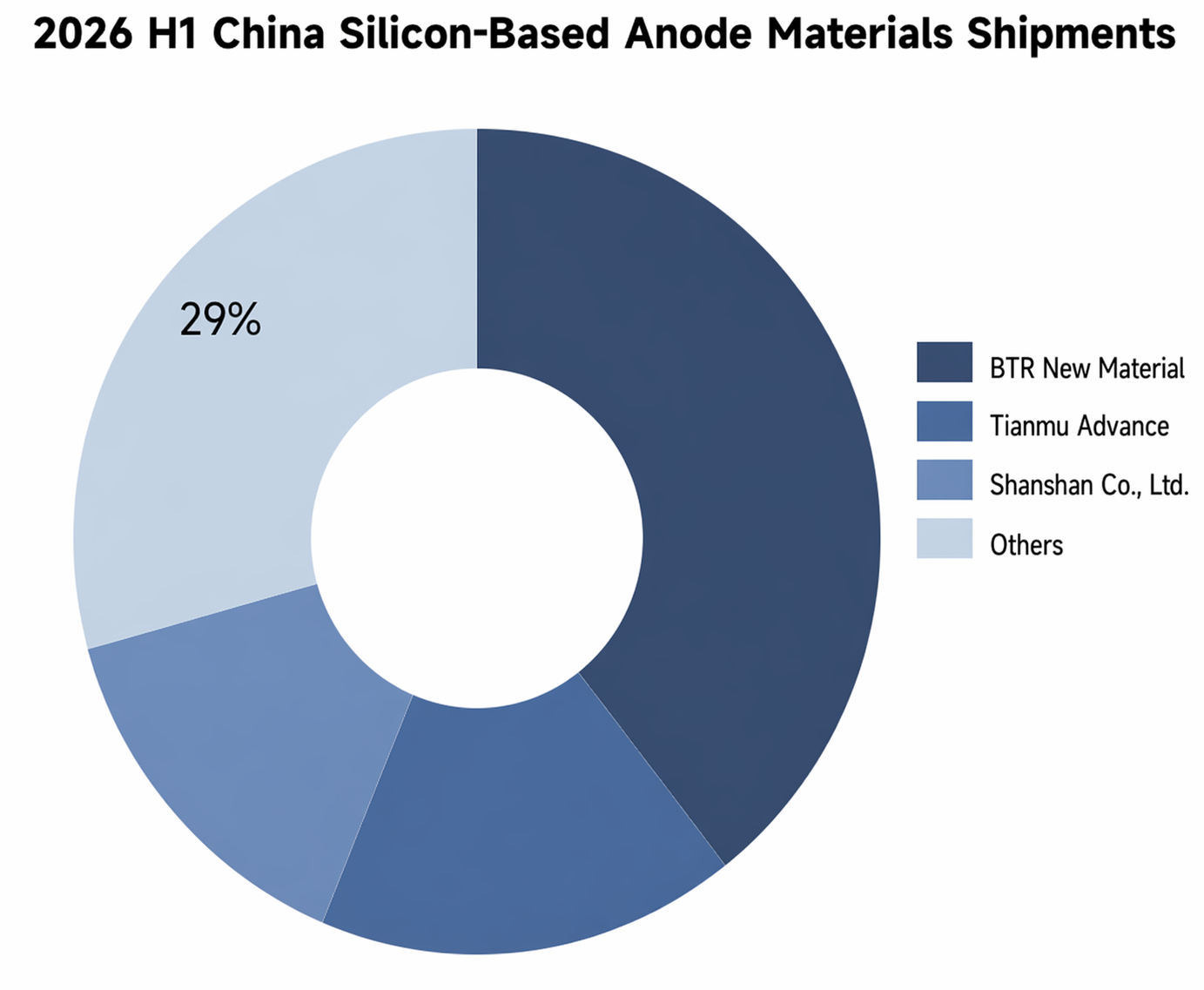

(I) H1 Market Landscape Review: Faster Capacity Release and Surging Shipments, but an Uneven Market

According to SMM data, China's silicon-based anode production reached 5,100 mt in H1 2026, surging 45% YoY from H1 2025—impressive growth. Notably, however, due to process barriers and the lock-in effect of designated projects from leading downstream battery producers, supply did not see a "hundred flowers bloom" but rather accelerated concentration toward the first tier. According to SMM data, the industry's CR3 exceeded 70% in H1 2026. This high level of concentration means small and medium-sized producers are facing increasingly severe challenges in technology validation, cost control, and large-scale stable delivery, while barriers to entry in the industry continue to rise.

(II) Market Share by Technology Route

From the perspective of technology route structure, silicon oxide anode, thanks to its long-term accumulation in consumer electronics and part of the EV sector, still accounts for the bulk of silicon-based anode shipments. However, in terms of the incremental market and high-end application trends, CVD-process silicon carbon anode is rapidly emerging as the "sole solution" for next-generation high-performance systems. Against this backdrop, although the overall shipment share of the CVD route remains lower than other silicon-based systems, its penetration rate in newly designated high-end projects has already increased significantly, and the generational shift of technology routes is irreversible. Its market share is expected to expand further in the coming years.

(III) Price Trend Review

The divergence in pricing was the most telling snapshot of the market in H1. Against the backdrop of tight effective capacity and high certification thresholds, the short-term supply-demand mismatch supported downstream demand for high-end silicon-based anodes, with high-quality products in a "hard to secure" position and prices showing strong performance. In sharp contrast, low and mid-end products faced the dual pressures of slowing demand growth and sufficient homogeneous capacity to meet downstream needs, leading to intensifying cost-performance competition, falling prices under pressure, and the prelude to an industry reshuffle.

II. Market Outlook

In the short term: high-end remains firm, low and mid-end under pressure

Looking ahead to H2 2026, high-end silicon-based anode prices are expected to continue to consolidate at highs. Although planned production lines are coming on stream one after another, constrained by client certification cycles and yield ramp-up progress, effective supply growth will remain limited, and the tight supply-demand balance is unlikely to be broken in the short term. In contrast, low and mid-end silicon-based anodes will face the dual squeeze of concentrated new capacity releases and moderate downstream demand growth, with increasing downward price risk and likely acceleration in the elimination of outdated capacity.

In the longer term: the value inflexion point is approaching, and the price center is expected to move lower

In the medium and long term, the theoretical cost of CVD silicon carbon anode is expected to trend downward, driven by three main factors: first, the continuous expansion of raw material capacity, with prices expected to fall further; second, CVD equipment is trending toward larger scale, combined with the continuous increase in localisation rates, which is expected to significantly reduce unit depreciation costs; third, as 10kt-scale production lines gradually reach full production, economies of scale will be unleashed, further diluting manufacturing costs. Overall, the value inflexion point for silicon carbon anodes is bound to arrive, at which point its unit capacity cost could become on par with or even more competitive than graphite, thereby realizing true commercial application.

Key Points to Watch

The core aspects of the subsequent market evolution are mainly in three areas: first, whether the ramp-up speed of new silicon-based anode capacity can achieve a dynamic balance with downstream acceptance of high prices; second, the pace of clearing out outdated low and mid-end capacity, which will determine the reshaping of the supply landscape; third, whether material enterprises can sustain their technological premium in an industry environment where "growth does not come with greater profit," and build a long-term competitive moat through product iteration and cost optimization. The interplay of these three factors will profoundly influence the competitive landscape and development path of the silicon-based anode material industry in the coming years.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875

Zhang Haohan 021-51666752

Wang Zihan 021-51666914

Wang Jie 021-51595902

Chen Bolin 021-51666836

Xu Yang 021-51666760

Xu Mengqi 021-20707868

Hu Xuejie 021-20707858

Yang Le 021-51595898

Wang Zhaoyu 021-51666827

Li Yisha 021-51666730

Huang Chencong 021-51595860

Lin Ziya 021-5166-6902

![[SMM Analysis] Riding the Winds In and Outside China, Breaking the Iron Law of Old Cycles: 2026 Energy Storage Battery Cell Semi-Annual Review and Outlook](https://imgqn.smm.cn/usercenter/WBREf20251217171728.png)

![[SMM Analysis] Separator Market 2026 Semi-Annual Review: Supply-Demand Pattern Tightens Marginally, Price Center Gradually Moves Up](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)