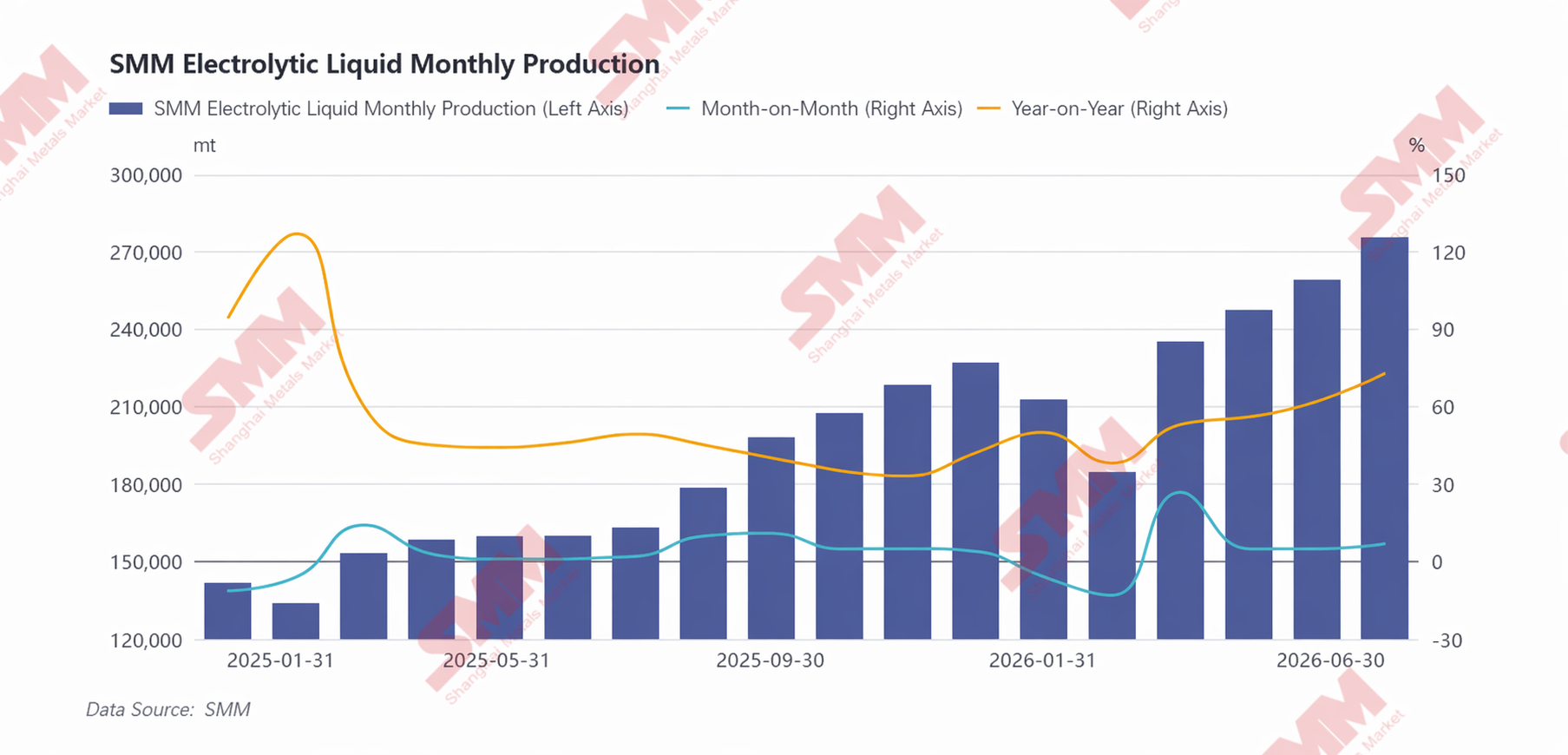

In H1 2026, China’s electrolyte market generally followed a first-down-then-up trajectory with pronounced structural divergence. Industry production and price trends moved in close step with downstream demand from power batteries and energy storage end-users, as well as upstream raw material price fluctuations.

In terms of production, the production pace of the electrolyte industry was highly tied to the operating rates of downstream battery cell manufacturers, with industry output fluctuating in sync with end-use lithium battery demand. Specifically, the market faced dual headwinds in Jan–Feb 2026. The NEV purchase tax shifted from “exempt” to “halved,” front-loading end-user car purchase demand, which, combined with the traditional off-season during the Chinese New Year holiday, led to a phased weakening of end-use demand. Downstream battery cell manufacturers proactively reduced their production schedules and compressed capacity utilization rates to match the sluggish demand, leading to a significant shrinkage in supporting electrolyte procurement orders and a concurrent month-on-month decline in industry output. After the Chinese New Year, the entire industry chain gradually resumed production, end-use demand began to recover, and electrolyte production sustained an uptrend from Mar–Jun. The power lithium battery segment provided strong support: on one hand, China’s passenger NEV exports stayed high; on the other, although overall domestic passenger vehicle sales fell short of expectations, steadily rising vehicle battery capacity, coupled with policies promoting new-energy heavy-duty and light-duty trucks that drove the penetration rate of commercial vehicle electrification steadily upward, effectively offset the pressure on overall vehicle sales and drove month-on-month growth in power battery cell demand. The energy storage track, driven by the long-term rigid demand from the global energy transition and China’s new-type power system construction, saw an accelerating pace in the implementation of tenders for wind and solar power supporting energy storage and standalone ESS projects, leading to steady expansion in ESS installations. With the dual drivers of power battery and energy storage markets, downstream battery cell enterprises continued to raise their operating loads, releasing supporting electrolyte production demand in tandem and sustaining a month-on-month increase in industry output. According to SMM statistics, over the past six months, China’s total electrolyte production reached 1.416 million mt, up 56% YoY from H1 2025.

From a structural perspective, H1 growth was highly concentrated among leading integrated electrolyte enterprises. These enterprises mostly held long-term locked-in orders from top battery manufacturers, ensuring demand certainty and providing a stable floor for production; simultaneously, by leveraging their own upstream raw material supporting advantages in LiPF6, solvents, etc., they could effectively hedge against raw material price fluctuations, guarantee continuous production and reasonable profits. Their overall capacity utilization rates stayed high, with some enterprises even running at full capacity. In contrast, small and medium-sized non-integrated enterprises, constrained by factors such as scattered orders and cost pressure, saw only limited production growth, with industry orders further concentrating among the leaders.

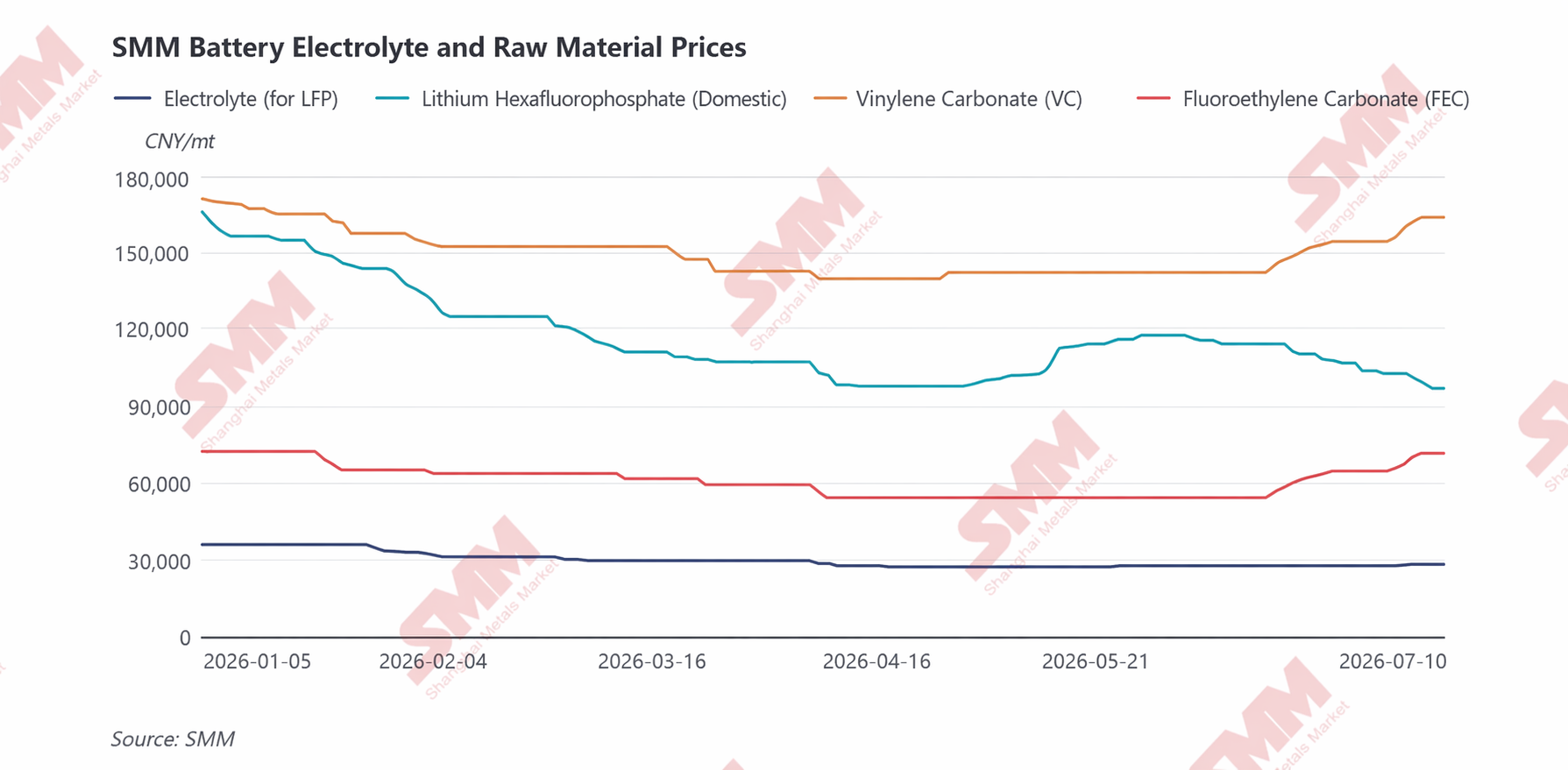

From a cost and price perspective, the H1 2026 electrolyte market was characterized by phased rotational adjustments and structural divergence driven by raw materials. Price trends at each stage were dominated by the intertwined strength and weakness of different cycles for solvents, LiPF6, and additives. The overall pattern was one of “declining costs and weak prices at the start of the year, then costs rebounding and prices stabilizing and rising mid-year driven by a tight additive supply-demand balance.”

In Jan–Feb, the industry was in a traditional demand off-season. As the concentrated end-use demand growth in Q4 2025 had tightened market supply-demand conditions, driving up electrolyte raw material prices (LiPF6, solvents, additives) to highs for the year, the slowdown in end-user procurement pace at the start of 2026 caused all upstream raw materials to simultaneously enter a downward price channel. This dragged the overall electrolyte production cost continuously lower, and prices further pulled back following the loosening on the cost side, resulting in an overall weak market at the start of H1.

Entering Mar–Apr, clear structural divergence began to emerge in the raw material segment. On the solvent side, logistical disruptions affecting upstream core raw materials like ethylene oxide due to geopolitical conflicts in the Middle East led to tightened supply expectations and rising risk-averse sentiment, rapidly driving up solvent raw material prices and subsequently causing carbonate solvent prices to surge in phases. However, the LiPF6 and additive segments were relatively in the doldrums, with overall ample industry supply and moderate profit margins for enterprises in the earlier period. Downstream electrolyte producers had a strong desire to bargain down procurement prices, causing LiPF6, VC, and FEC prices to continue drifting lower. The cost uplift brought by rising solvent prices during this period was limited and insufficient to offset the cost decline caused by LiPF6 and additives; the overall electrolyte cost still declined somewhat, and market prices continued to run weak.

In May–Jun, the electrolyte cost logic shifted again, with the market focus moving from solvents to LiPF6 and additives. In May, as earlier geopolitical risk sentiment on the solvent side gradually subsided, upstream raw material prices pulled back, combined with overall loose market supply, causing solvent prices to continue weakening and exerting some downward pressure on electrolyte costs. However, the LiPF6 market saw a phased recovery. Affected by a sharp rise in lithium carbonate prices, coupled with simultaneous price increases for phosphorus pentachloride and anhydrous hydrogen fluoride, cost pressure on LiPF6 producers increased significantly, with prices approaching the cost floor; meanwhile, the market had continued destocking earlier, resulting in tight circulating supply. The marginal repair of the supply-demand pattern pushed LiPF6 prices to bottom out, providing some support for electrolyte prices. Entering June, lithium carbonate prices began to pull back from mid-May, dragging LiPF6 prices down again and weakening lithium chemicals’ cost support for electrolytes. In stark contrast, the additive segment strengthened once more. As downstream power battery and energy storage demand continued to recover and electrolyte operating rates climbed steadily, VC and FEC demand continued to expand. However, new industry capacity ramp-up progress fell short of expectations, limiting effective supply growth, and market supply-demand conditions continued to tighten. Producers showed a strong willingness to hold prices firm and push for hikes; electrolyte manufacturers, to ensure normal order deliveries, had no choice but to passively accept raw material price increases, further fueling the rise in VC and FEC prices, which became the core dominant factor driving the phased increase in electrolyte costs.

Looking ahead to H2, the power segment is expected to show growth, driven by sustained strong new orders for passenger NEVs, increased vehicle battery capacity, and the gradual advancement of commercial vehicle electrification. Energy storage demand remains robust, and enterprises’ overall production schedules are expected to maintain firm growth. Supported by demand, H2 electrolyte demand is expected to improve further compared to H1, driving production growth. From a cost and price perspective, the continued recovery in downstream demand will further tighten the supply-demand balance for core additives like VC, with the short-term tightness persisting; LiPF6 prices, supported by lithium carbonate costs, are expected to stay high and move sideways. Overall, backed by the rigid support of core raw materials, H2 electrolyte prices are expected to sustain a drifting higher trend.

Note: If you have any supplements or corrections regarding the details mentioned in this article, please feel free to contact us. Contact information is as follows:

Tel: 021-20707858 Hu Xuejie, Thank you!

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lyu Yanlin 021-20707875

Zhang Haohan 021-51666752

Wang Zihan 021-51666914

Wang Jie 021-51595902

Xu Yang 021-51666760

Xu Mengqi 021-20707868

Hu Xuejie 021-20707858

![[SMM Analysis] Separator Market 2026 Semi-Annual Review: Supply-Demand Pattern Tightens Marginally, Price Center Gradually Moves Up](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)

![H1 Refined Cobalt Price Surged over 97% YoY; Demand Remains the Current Focus; What Can the Market Expect Going Forward? [Weekly Observation]](https://imgqn.smm.cn/usercenter/oVqJl20251217171730.jpg)