In H1 2026, driven by the resonance of multiple demands from new energy, AI computing power, and consumer electronics, China's copper foil industry continued the high prosperity trend that began in Q4 2025. The overall industry presented a pattern of rising volumes and prices and supply-demand tightness.

1. Capacity utilization rate continued to rise, with a supply gap in high-end categories

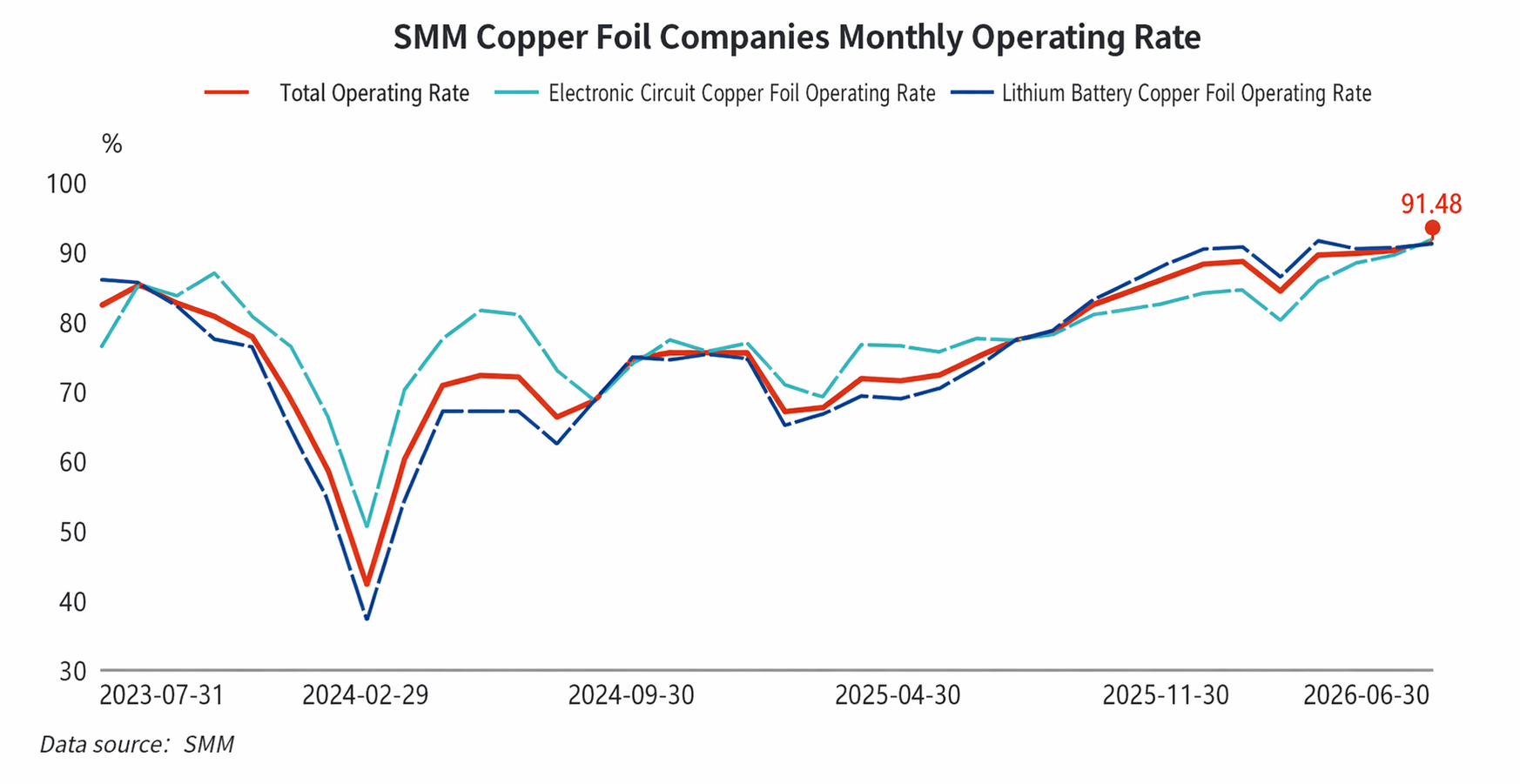

On the supply-demand side, in H1 the industry's operating rate operated at high levels overall, steadily climbing from 88.56% at the start of the year to over 91% by the end of Q2, consistently holding above the 90% mark. Demand for both lithium battery copper foil and electronic circuit copper foil strengthened simultaneously. Benefiting from the intensive roll-out of local energy storage subsidies and the rising penetration rate of NEVs in H1, power batteries maintained a high production schedule pace. Coupled with the concentrated installation rush before the "630" grid connection for energy storage, the incremental growth in demand for lithium battery copper foil was pronounced. Meanwhile, AI computing centers and 5G/6G communication equipment boosted the rapid volume growth in demand for high-end electronic copper foils such as RTF and HVLP series, driving the conversion of ordinary capacity to high-end. Consequently, a supply gap emerged in traditional electronic circuit copper foil. Moreover, against the backdrop of optimistic end-use demand and the fact that new capacity release still requires time, SMM expects that China's lithium battery copper foil supply and demand for the full year 2026 will present a slight shortage pattern.

2. Processing fees rose across the board, with the industry's profitability continuing to recover.

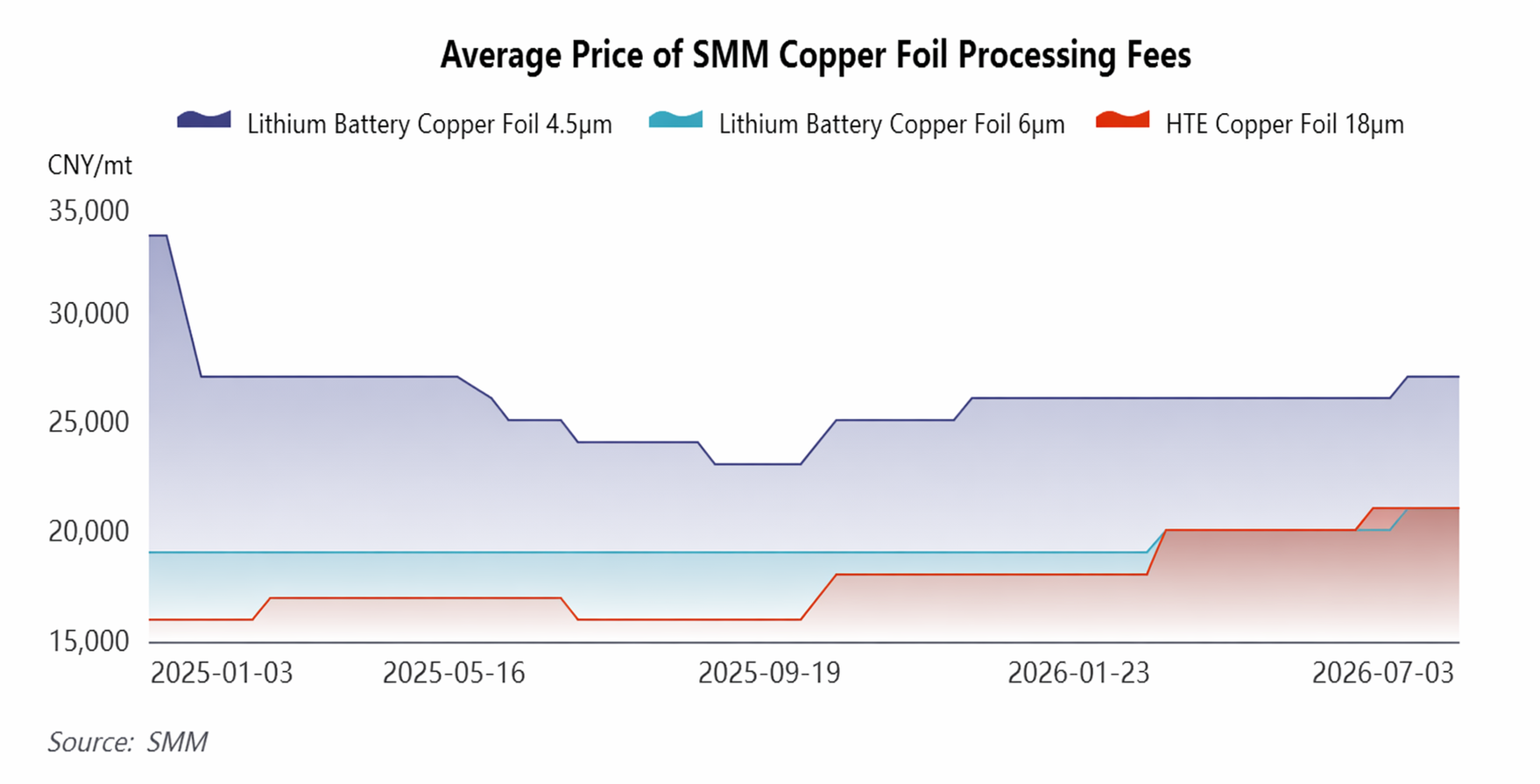

On the price side, benefiting from supply-demand tightness, copper foil processing fees for all specifications climbed steadily. As of the end of June 2026, mainstream specification processing fees rose comprehensively compared to the start of the year: the 4.5μm lithium battery copper foil processing fee was raised by 1,000 yuan/mt to 27,000 yuan/mt; the 6μm lithium battery copper foil processing fee was raised by 2,000 yuan/mt to 21,000 yuan/mt; and the 18μm HTE copper foil processing fee rose by 3,000 yuan/mt to 21,000 yuan/mt. The rise in processing fees effectively offset cost pressure from raw material price fluctuations, strengthening the industry's profitability resilience.

3. Exports surged significantly, with the trade structure continuing to improve.

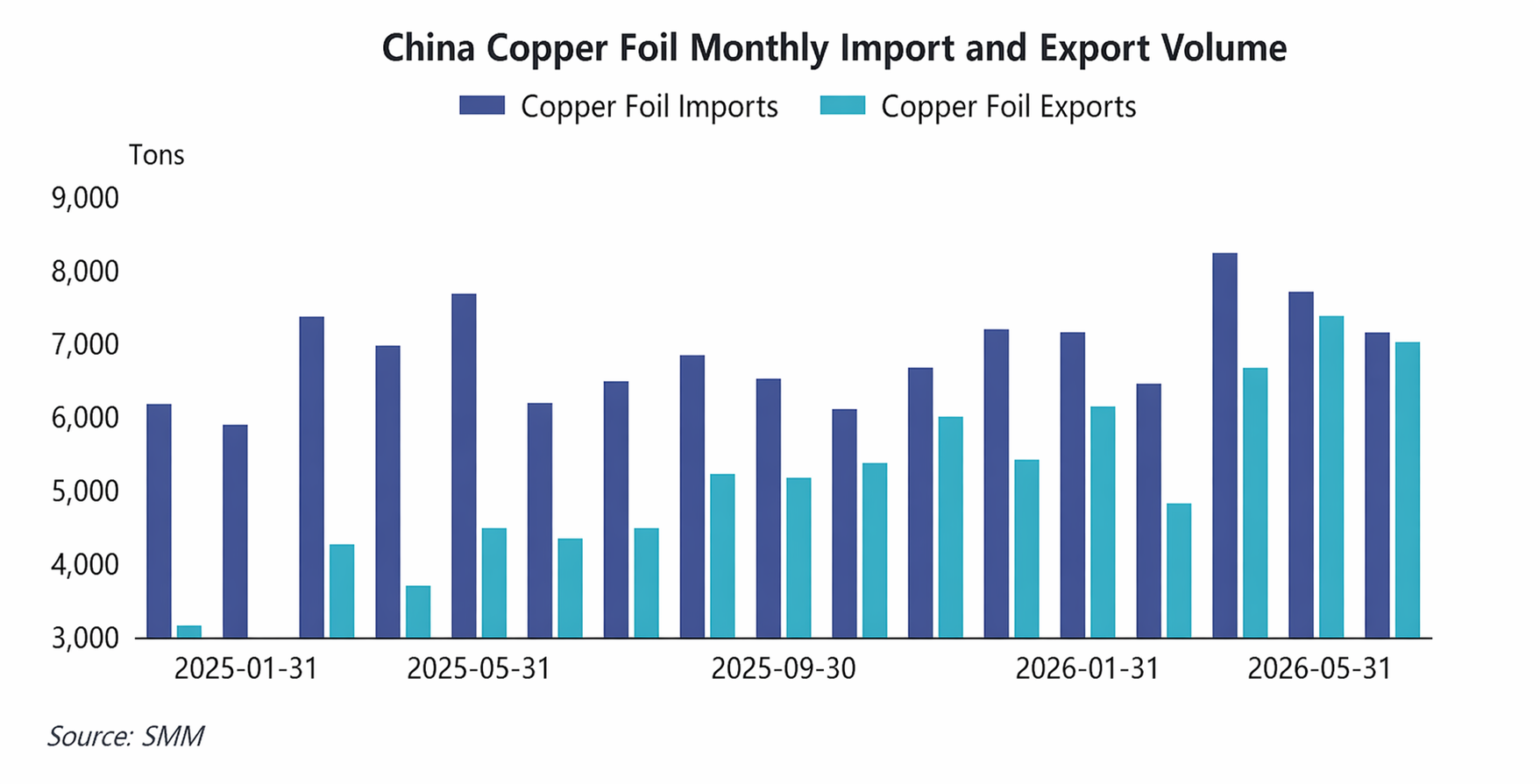

Import and export, in H1 China's copper foil exports continued to surge. From January to May 2026, China's cumulative copper foil exports were 32,000 mt, surging 71.79% YoY, with new monthly highs set in March and April. The main export destinations were Thailand, South Korea, Malaysia, etc. On the import side, growth slowed down significantly; from January to May 2026, cumulative imports were 36,600 mt, up only 7.63% YoY, while imports in May fell both YoY and MoM. Domestic substitution for low and mid-end products continued to advance, but high-end HVLP series products still rely on imports from Taiwan, China, and Japan, leaving ample room for domestic substitution. The industry's trade deficit narrowed significantly from $103.14 million at the start of the year to $45.9 million in May.

IV. H2 Market Outlook: The upcycle extends, with a tight supply-demand balance supporting high processing fees.

Looking ahead to H2, high industry prosperity is expected to continue. On the demand side, policies supporting energy storage and digital infrastructure under the 15th Five-Year Plan will continue to be implemented, and, coupled with the advancement of renewable energy targets outside China, incremental growth potential remains. Meanwhile, the NEV penetration rate will keep rising, and seasonal strength in AI, 5G/6G, and consumer electronics will become more pronounced. On the supply side, most enterprises are currently running near full production schedules. If new capacity ramp-ups fall short of expectations, the supply-demand gap for lithium battery copper foil could widen further in Q3 and Q4, supporting processing fees at high levels. Regarding imports and exports, Japanese and Taiwan, China enterprises are accelerating their switch to high-end electronic copper foil capacity, providing Chinese domestic enterprises with ongoing export opportunities in the mid-end market. Annual exports are expected to hit a record high, and the trade deficit will continue its narrowing trend.

![2026 China's Copper Anode Market H1: Supply Contraction Reverses the Pattern [SMM Analysis]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)