I. Full Review of Copper Billet Industry in H1 2026

(I) Policy Side: Strict Control of Reverse Invoicing, Long-Term Restriction on Recycled Raw Material Circulation

In H1, fiscal and tax supervision became the core underlying constraint weighing on the copper billet industry. The reverse invoicing policy for recycled resources entered a phase of normalized, high-pressure implementation; natural-person individual sellers had an annual invoicing quota of 5 million yuan, which significantly narrowed circulation channels for domestic unticketed scrap brass. Grassroots recyclers showed low willingness to sell, leading to a persistent shortage of compliant domestic sources of secondary brass.

During the policy transition period, corporate compliance costs rose notably. Small and medium-sized processing plants, lacking channels for stable raw materials with invoices, were forced to proactively cut production and undertake maintenance to avoid risks. Large top-tier players leveraged their international trade qualifications and stable import sources to buffer the raw material gap, accelerating the concentration of industry capacity toward compliant large-scale enterprises. The No. 770 policy on secondary copper tax rebates continued to tighten, completely compressing the grey circulation space in the industry. The contradiction of raw materials "having the goods but no invoices available, with invoiced goods at high prices" pervaded the entire H1 cycle.

(II) Raw Materials and Imports/Exports: Domestic Secondary Supply Contracted, Premiums on Imported Secondary Brass Rose

1. Domestic Raw Material Bottleneck Intensified

The compliant circulation volume of domestic scrap brass fell sharply YoY, weakening the cost advantages of secondary brass over copper cathode. Most brass billet plants faced difficulties in raw material procurement and high credit costs, and with the natural-person quota ceiling constraint, supply could hardly return to the level seen in previous years. Meanwhile, speculation in the brass scrap market further drove up prices, and copper-zinc separation operations raised overall raw material costs.

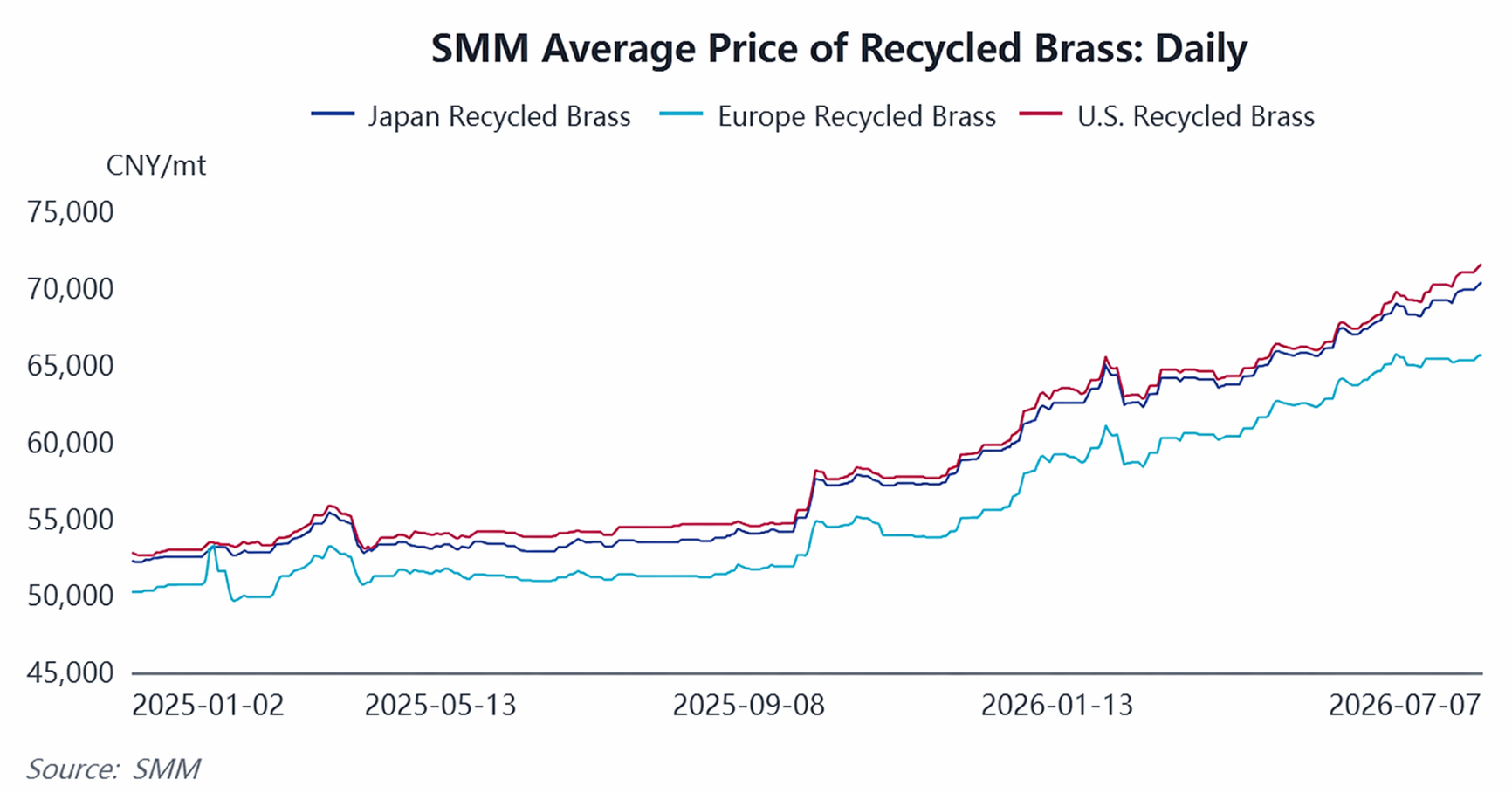

2. Imported Cargo Became a Mainstream Supplement, but Costs Continued to Rise

Domestic enterprises turned to bulk purchasing of imported secondary brass with invoices. In H1, imports of secondary brass maintained YoY growth, however, overseas scrap copper export policy uncertainties and rising international copper prices pushed up procurement premiums. Available overseas scrap brass supply tightened, and import procurement coefficients continued to climb, further raising raw material costs for brass billet.

Data Source: SMM

Data Source: SMM

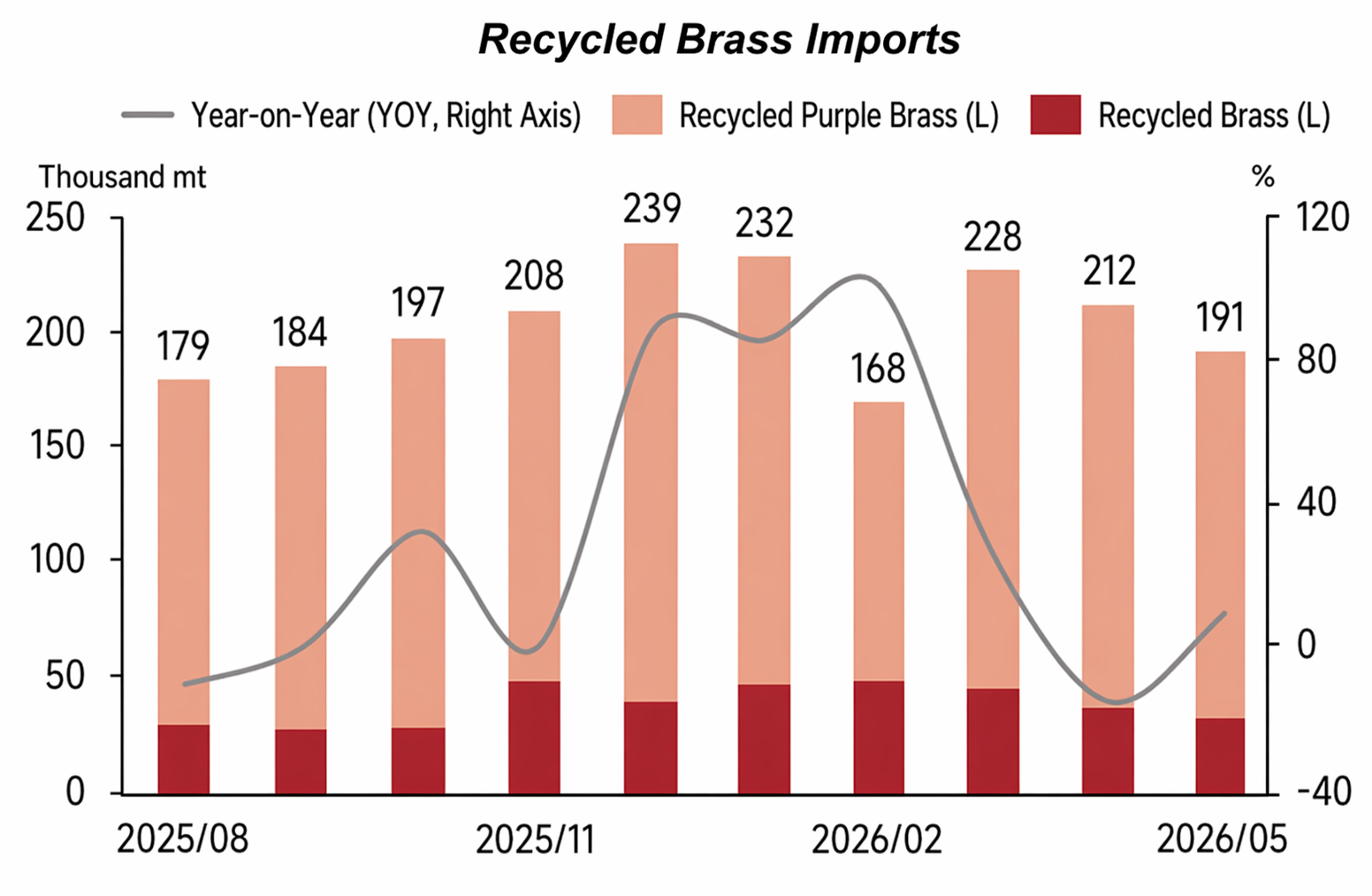

From January to May, cumulative imports of brass billet in China were approximately 11,400 mt, down 1.23% YoY, but the cumulative import value reached $105.7079 million, up 23.42% YoY, highlighting a pattern of shrinking volume and rising prices. In terms of import sources, in May, South Korea remained the largest source country (accounting for approximately 40%), with Japan second (at approximately 16%), showing initial signs of regional diversification.

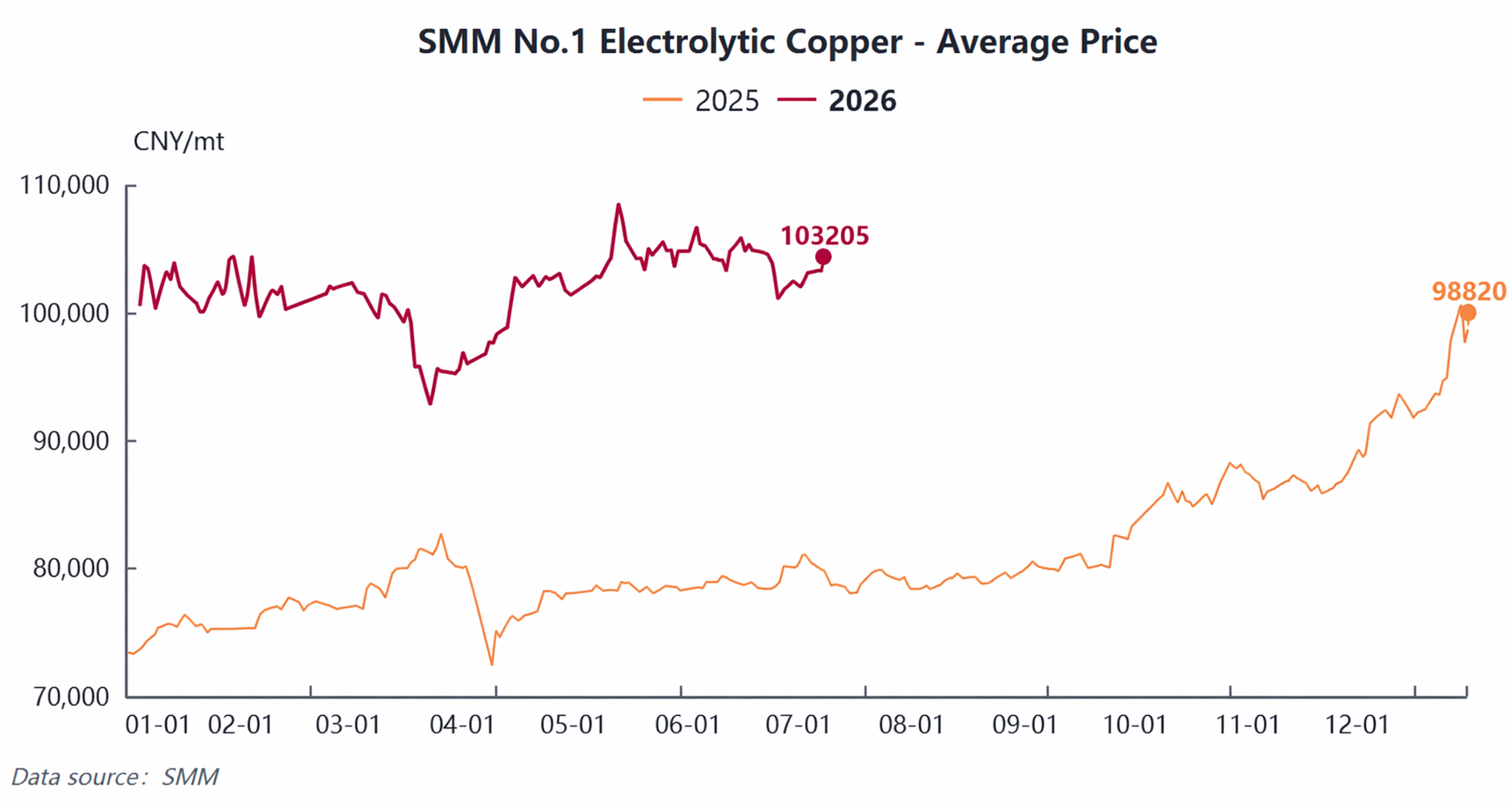

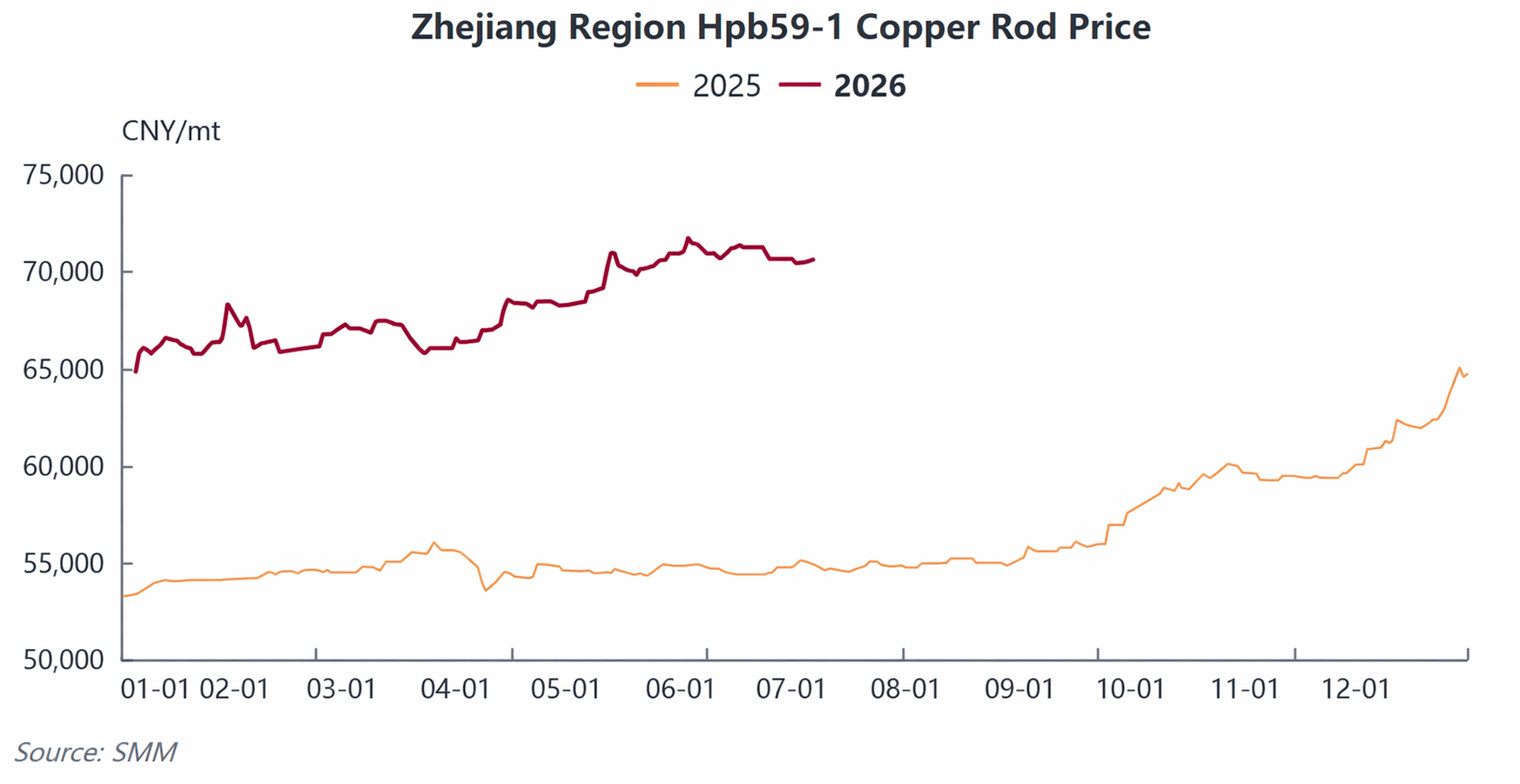

(III) Costs and Prices: Copper Prices Swung Wildly at Highs, Industry RC Continued to Decline

In H1 2026, copper cathode prices showed a pattern of "retreating after a rapid rise and consolidating at highs." Prices hit an annual peak in January and fell to a periodic low in March. In Q2, the price center stabilized above 100,000 yuan/mt, with the annual average price rising sharply YoY, directly lifting raw material costs for copper billet. As of end-June, the average spot price of Hpb59-1 brass billet in the Zhejiang region had climbed to a historical high of 70,650 yuan/mt.

Price transmission had significant blockages: traditional downstream brass demand was sluggish, with end-users possessing strong bargaining power, so raw material price increases could not be smoothly transferred downstream. The industry exhibited a typical pressured pattern of "rising prices with weak volume." From April to May, the overall profitability pressure on the industry climbed to its worst level in the past two to three years.

High-precision copper billet used in new energy and AI applications saw stronger RC resilience due to technical barriers and stable rigid demand, making it the only sub-category with relatively stable profits in H1. Coupled with rising logistics, tax, and capital occupation costs, most small and medium-sized brass billet enterprises remained in a state of meager profit or even losses over the long term.

(IV) Supply and Demand: Demand Severely Polarized, Operating Rates Stayed Low

1. Supply Side: Operating Rate Weakened Month by Month, Enterprise Polarization Significant

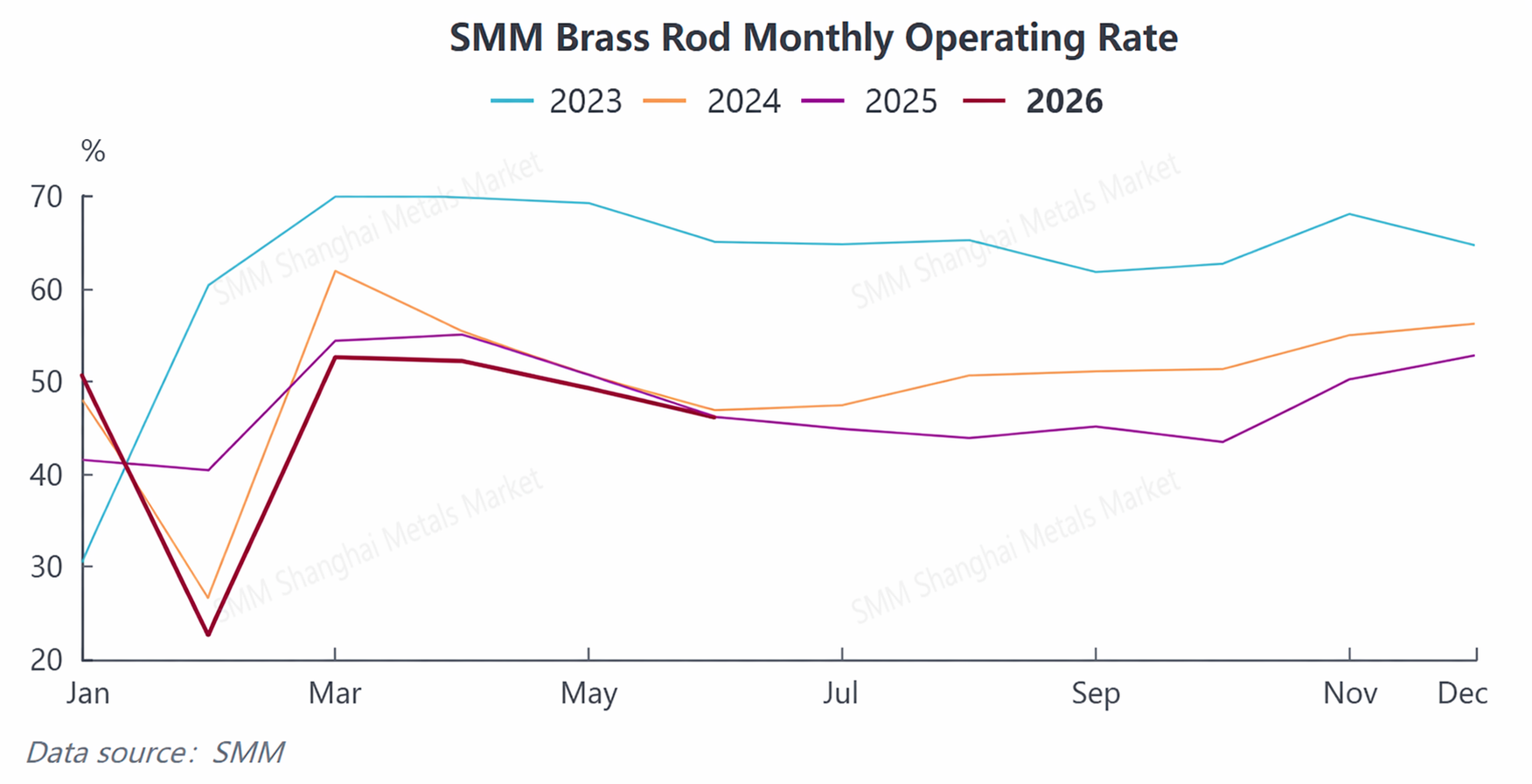

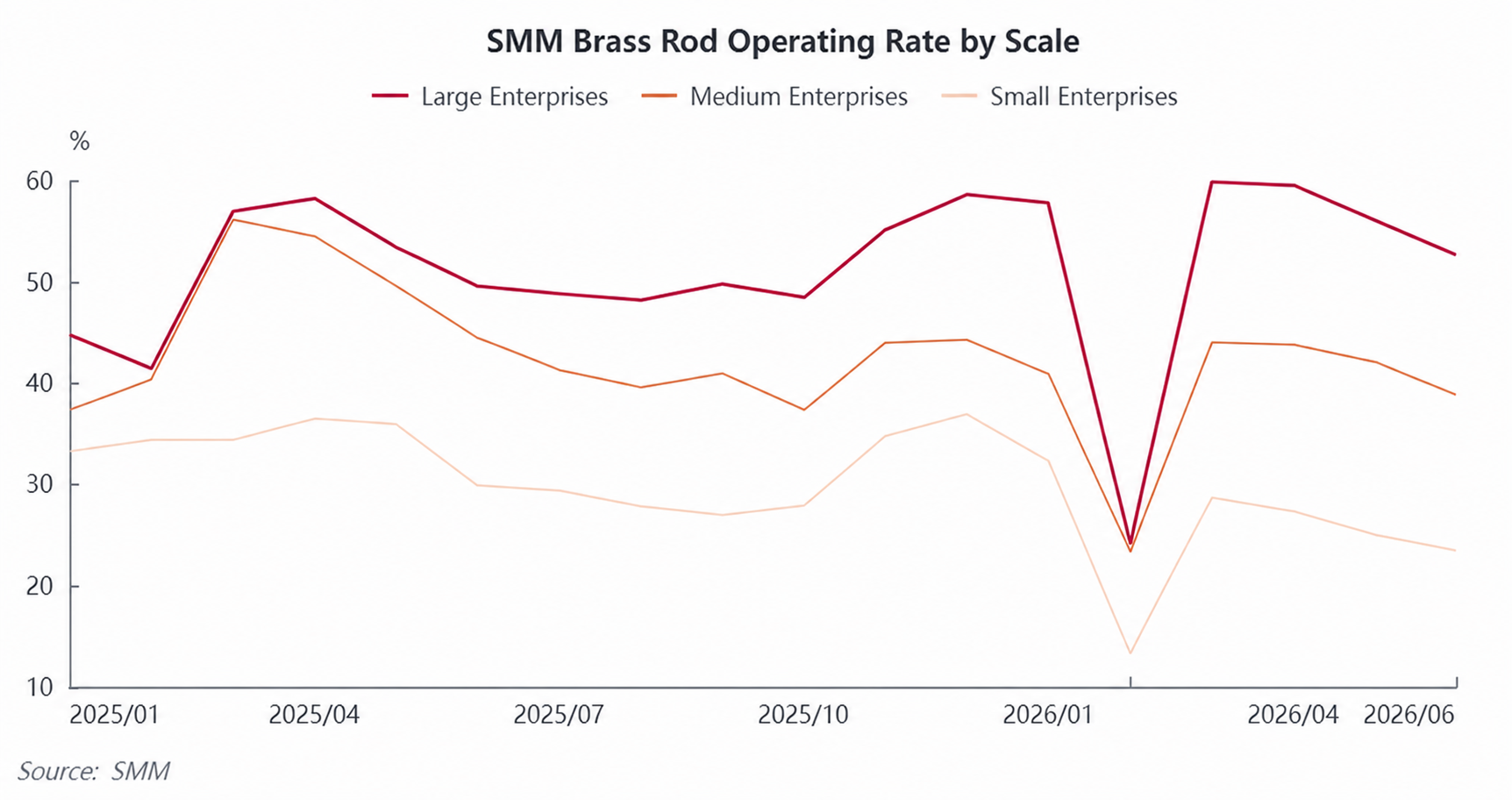

The overall copper billet operating rate drifted lower in H1, continuously falling back from 50.86% in January to 46.09% in June, with declines seen both YoY and MoM. The gap in capacity polarization continued to widen: large enterprises with stable raw material channels saw a 52.6% operating rate in June; medium-sized enterprises, squeezed by both raw materials and orders, operated at only 38.76%; small processing plants, facing raw material shortages and order scarcity, saw operating rates fall to 23.44%, intensifying industry polarization.

Raw material constraints were the core supply-side constraint; coupled with losses forcing enterprises to control production, the overall industry capacity utilization rate remained in a historically low range in H1.

2. Demand Side: Traditional Sectors Weakened Deeply, Emerging Sectors Strengthened Independently

Traditional brass demand (air conditioning, plumbing, valves, general hardware) remained persistently weak in H1. The downturn in the post-property cycle, combined with an early off-season for home appliances, saw downstream users purchasing as needed without concentrated restocking. Meanwhile, the substitution penetration rate of stainless steel in air conditioning parts continued to rise, continuously diverting rigid demand from brass, and brass billet orders shrank month by month.

Data Source: SMM

Structural demand support was concentrated in the copper billet segment: the three electric systems (power battery, drive motor, and electronic control system) of NEVs, large-power charging piles, energy storage PCS, AI server GPU cooling, and precision pins for optical modules continuously released stable rigid demand. Orders for high-purity oxygen-free copper billet were full, partially offsetting the overall decline in industry demand. However, with copper billet capacity accounting for a limited share, this was not enough to boost the brass segment's recovery.

II. Market Outlook for Copper Billet Industry in H2 2026

In Q3, the industry is expected to be under pressure and hit bottom.The traditional off-season, coupled with high temperatures suppressing end-user procurement and the ongoing impact of stainless steel substitution, is expected to weigh on brass demand. SMM expects the overall copper billet operating rate to continue falling to 43.65% in July, hitting an annual low. Policy-side reverse invoicing supervision is unlikely to ease, capping the compliant supply of domestic scrap brass. Combined with continuously tightening controls on overseas scrap copper exports, the pattern of high premiums on imported secondary brass is expected to persist. The raw material bottleneck is set to run through the off-season. Brass billet is anticipated to be dragged down by the triple headwinds of the off-season, substitution, and low RCs, with profitability under sustained pressure in Q3. Only the continued commissioning of NEV and AI computing infrastructure projects is likely to bring rigid demand orders for copper billet, forming the sole demand support.

In Q4, prosperity is expected to recover on a QoQ basis.As home appliances and plumbing enter their traditional stockpiling peak season, brass billet orders are expected to rebound MoM. Combined with year-end push for annual targets in PV, energy storage, and NEVs, demand for copper billet is expected to further strengthen, with industry operating rates and transactions both recovering. However, copper cathode prices are highly likely to continue consolidating at highs, with the raw material cost center stay high, putting cost pressure on processing enterprises throughout the year.

In the medium and long term, the traditional brass demand center is expected to decline year by year, while AI computing, new energy, and energy storage constitute the core growth drivers of the copper billet industry. Small and medium-sized outdated capacity is expected to continuously exit the market, while top-tier players are simultaneously laying out high-end copper billet capacity. The three major thresholds of raw materials, orders, and compliance continue to widen the gap between enterprises, making the industry's transformation towards scale, compliance, and high-end manufacturing an irreversible trend.

In summary: In H1 2026, the core contradictions in the copper billet industry were supply shortages caused by tightening recycled raw material policies, weakening traditional end-use demand, and the squeezing of processing profits by high copper prices. The industry relied on new energy and AI copper billet for structural support, maintaining a generally weak operating environment. In H2, the market is expected to show a pattern of initial weakness followed by later strength: in Q3, the triple negative resonance of the off-season, raw materials, and substitution is expected to keep operating rates and profitability under sustained pressure; in Q4, the combination of the traditional end-user peak season and continuously increasing volumes from emerging sectors is expected to repair industry prosperity on a QoQ basis. In the medium and long term, the reverse invoicing policy is reshaping the secondary copper circulation system, accelerating market clearing. High-precision copper billet for new energy and AI computing infrastructure is expected to become the core future growth line for the copper billet industry.

![2026 China's Copper Anode Market H1: Supply Contraction Reverses the Pattern [SMM Analysis]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![2026 China Copper Foil Industry Half-Year Summary and Outlook [SMM Analysis]](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)