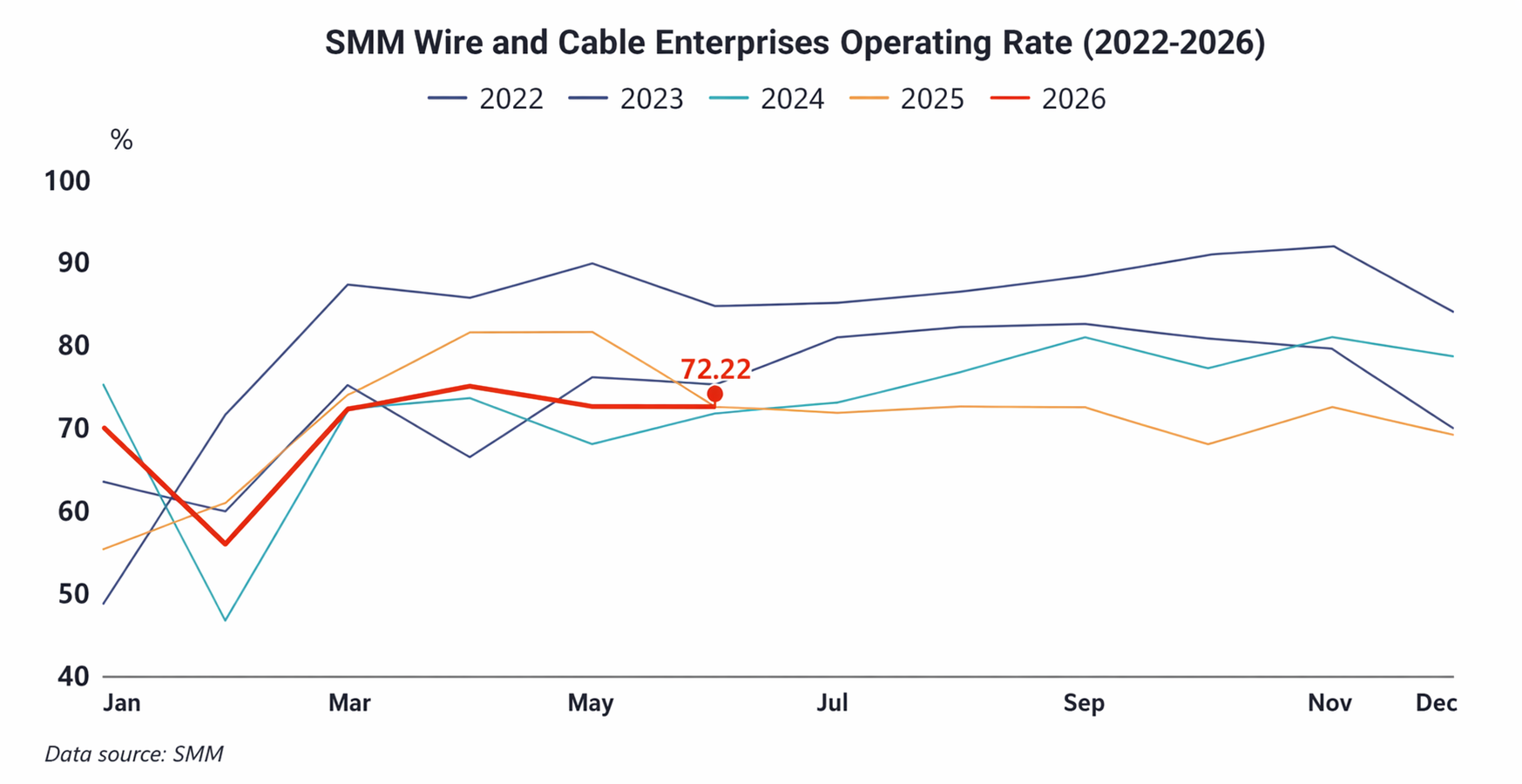

In June, the operating rate in the copper wire and cable industry was recorded at 72.22%, down 0.11 percentage points MoM and down 0.19 percentage points YoY. Among them, the operating rate for large enterprises was recorded at 77.62%, for medium-sized enterprises at 50.4%, and for small enterprises at 47.54%.

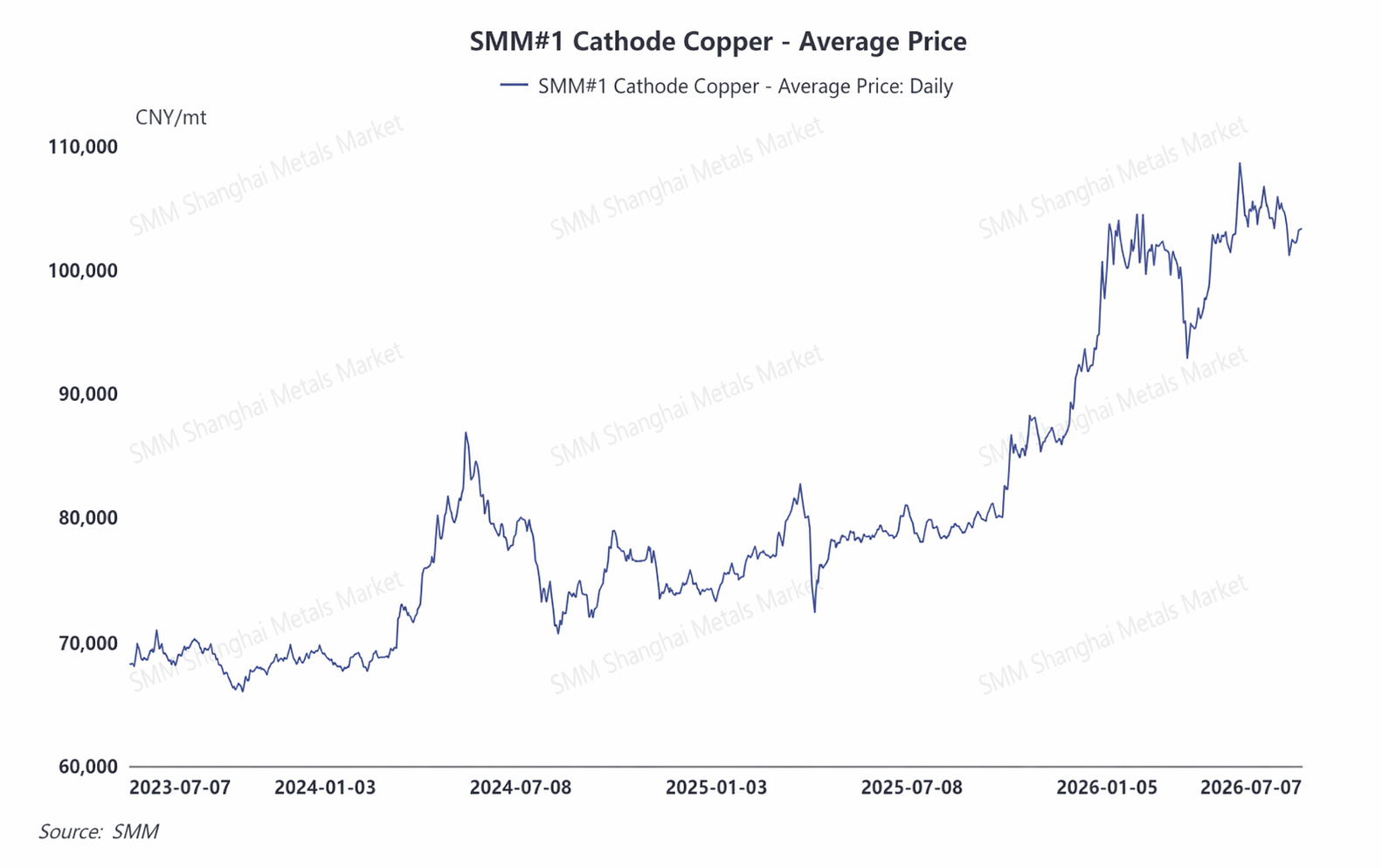

In June, copper prices overall exhibited wild swings. During the downward phase, end-user purchase willingness heated up, with concentrated copper lock-in stockpiling, briefly boosting order increases; but as copper prices rebounded and the industry entered the traditional consumption off-season, the overall new order scale contracted again. End-user demand by segment polarized, with orders for State Grid projects, offshore wind power, new energy support facilities, and AI computing power cables being well received, providing demand support; while demand in other downstream sectors such as real estate and civilian use remained mediocre with no clear improvement signals.

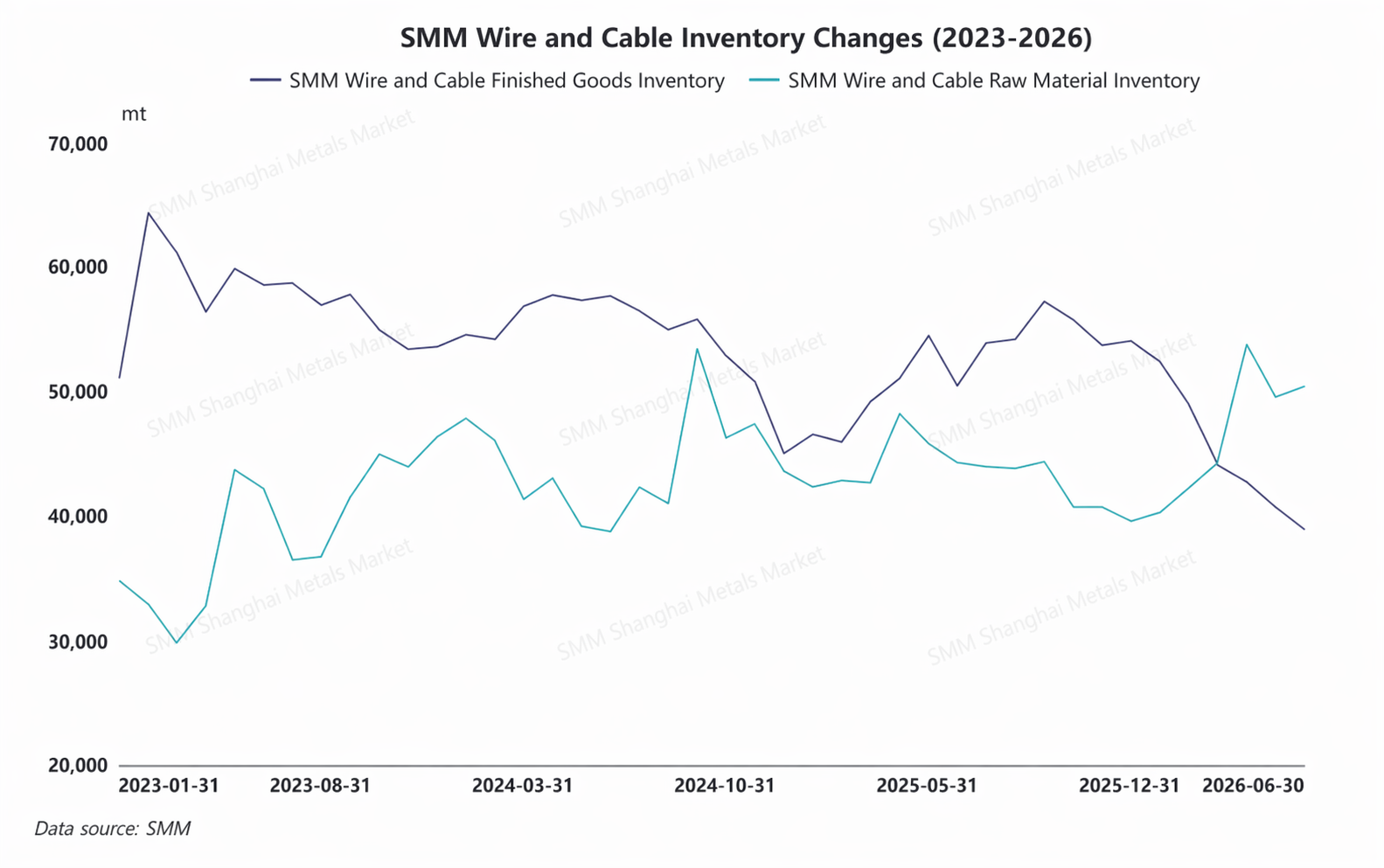

In June, days of raw material inventories for copper wire and cable decreased by 0.1 days MoM, while days of finished product inventories decreased by 0.42 days MoM. After adjusting for day differences, the actual absolute raw material inventory increased by 0.42% MoM, and finished product inventory decreased by 0.79%. During the copper price correction phase, enterprises cautiously engaged in essential stockpiling, driving growth in raw material inventory. However, with sluggish off-season market demand, the pace of end-user cargo pick-up slowed, and finished product warehouse withdrawal efficiency was low, so finished product inventories edged down.

The operating rate in July is expected to increase by 0.43 percentage points MoM to 72.45%, and up 0.61 percentage points YoY. New orders secured in June and earlier low-price copper lock-in orders will gradually enter the production schedule, providing effective support for the industry's operating rate. However, as July remains in the traditional demand off-season, with insufficient real market essentials demand, end-user new orders will likely weaken MoM. Constrained by multiple factors, the overall industry operating rate rebound will be limited.

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![[SMM Analysis] May Indonesia Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)