》Click to View SMM Copper Spot Price Historical Trends

1. H1 Industry Review: Operating Rate Trending High then Low, with Structural Divergence as the Core Theme

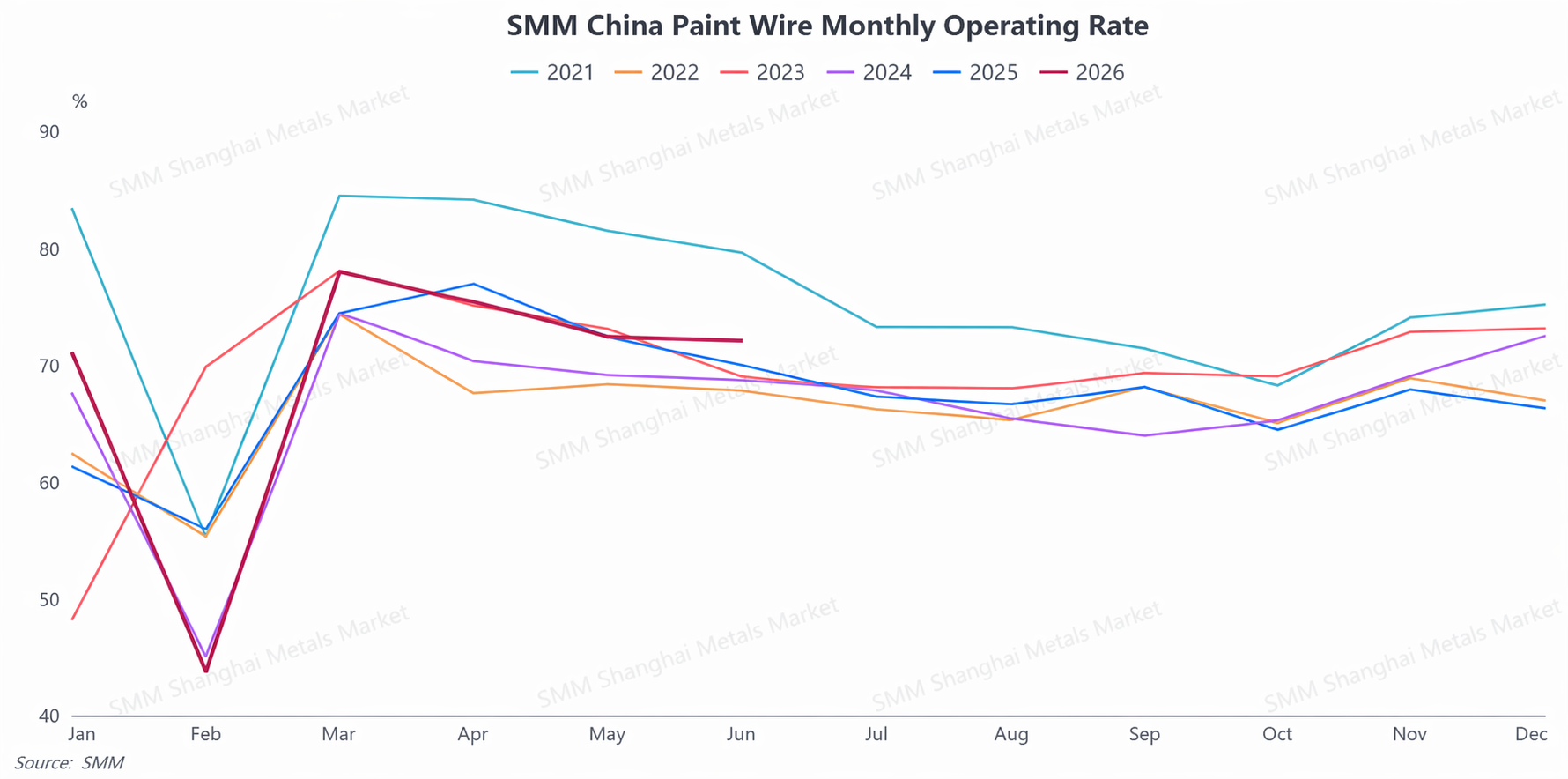

In H1 2026, China’s enamelled wire industry exhibited a phased pattern of “post-Chinese New Year rebound and surge, followed by a steady pullback in Q2,” with its operating characteristics sharply focused on structural divergence. At the beginning of the year, dragged down by both the Chinese New Year production halt and high copper prices, the industry’s overall operating load was low. In March, benefiting from a phased pullback in copper prices and the traditional peak consumption season, enterprises intensively resumed production, pushing the industry’s operating rate to its H1 peak. Entering Q2, the industry moved into its seasonal off-season, and coupled with intensifying divergence in end-use demand, the overall operating rate steadily pulled back. However, the overall H1 operating level still outperformed the same period last year, highlighting the industry’s overall resilience.

Wide fluctuations in copper prices were the core variable impacting production and order pace in the enamelled wire industry during H1, creating a typical see-saw linkage between copper prices and orders. In March, a phased decline in copper prices effectively alleviated downstream procurement cost pressure. End-user enterprises took advantage of the low prices to restock intensively, releasing previously accumulated backlog orders, which drove both the industry’s operating rate and new orders higher in tandem. In Q2, domestic copper prices consolidated at highs, significantly increasing raw material procurement costs for the industry. Downstream end-user enterprises’ wait-and-see sentiment intensified, with restocking willingness sharply contracting and the pace of order releases continuing to slow. Coupled with the seasonal off-season characteristics of Q2, high copper prices further amplified the pullback pressure on industry orders, becoming the core factor constraining the industry’s prosperity in Q2.

End-use demand displayed a stark polarization, with divergence between new and traditional sectors becoming prominent. Demand from high-end emerging sectors such as NEVs, power transformers, industrial motors, AI computing equipment, and two-wheeled NEVs remained rigid and robust, serving as the core ballast underpinning industry prosperity. After the Chinese New Year break, operating rates of top-tier players focusing on these sectors quickly rebounded to over 90%. Some sub-sectors even faced tight supply and undersupply situations, continuously supporting the industry’s overall operating floor. In the traditional home appliance sector, demand trends weakened significantly and volatility intensified. Among these, the air-conditioner end-use market exhibited a pattern of “peak season demand being prematurely exhausted and rapid cooling during the off-season”, which briefly drove up the industry’s operating rates in March, but entered the demand off-season ahead of schedule in Q2. Orders for enamelled wire used in home appliances fell over 20% YoY, forcing related enterprises to cut production and destock, becoming the main drag on overall industry prosperity.

2. Export Market Shines: Record High Volume and Breakthrough Growth in Emerging Markets

In H1, China’s exports of copper enamelled wire continued their strong momentum, with export resilience being continuously displayed and total volume hitting a record high for the same period. Data shows that in January-May, China's cumulative exports of copper enamelled wire reached 61,416 mt, up 7.13% YoY, with May exports alone amounting to 13,905 mt, hitting a record high for the same month in previous years. Demand from markets outside China has become a key growth driver for the industry.

In terms of export structure, traditional core markets maintained a solid base, with Vietnam, Japan, and Thailand remaining the top three destinations for China's enamelled wire exports, together accounting for 32% of total exports, indicating stable traditional demand outside China. The biggest highlight of H1 exports came from explosive growth in emerging markets. The Türkiye market emerged as a standout performer and became a core bright spot of industry growth: exports to Türkiye surged 645.6% YoY in January-February, maintained a high growth rate of 544.3% YoY in April, and, despite a pullback in May, were still up a significant 312.1% YoY. Türkiye has now jumped to become the fourth-largest export destination for China's enamelled wire. Meanwhile, demand continued to recover in markets outside China such as Mexico and the US, with export growth turning positive. Currently, China's enamelled wire exports cover more than 130 countries and regions globally, reflecting markedly effective global layout and ample overall export growth momentum.

III. H2 Market Outlook: Overall Stability, Continued Structural Divergence, and Unchanged Rigid Demand Support Trend

Based on comprehensive industry supply-demand dynamics, raw materials, and end-use demand trends, the enamelled wire industry is expected to continue its core pattern of overall stability and structural divergence in H2 2026, characterized by "pressure in traditional sectors during the off-season, rigid support from emerging sectors, and copper price-led fluctuations."

On the pressure side, the off-season effect in traditional sectors is becoming pronounced, with demand recovery remaining sluggish. The weakening trend in home appliance demand is difficult to reverse in the short term, while mature sectors like traditional industrial motors lack new sources of incremental rigid demand. Traditional orders across the industry are expected to face continued periodic pressure in H2. At the same time, high-level fluctuations in copper prices will continue to affect industry procurement, production, and restocking pace, serving as the main uncertainty factor driving market fluctuations. On the support side, three core sources of momentum will continue to underpin the industry’s prosperity baseline. First, sustained steady demand from the two core sectors of NEVs and power transformers, with prominent rigid demand characteristics, provides solid bottom-level support for industry production and orders. Second, accelerating construction of AI computing infrastructure continues to release demand for copper semis used in data centers and computing equipment, creating an entirely new incremental growth sector for the enamelled wire industry. Third, growth momentum in the export market continues, with the 7.13% YoY export growth in H1 laying a solid foundation for full-year export growth. Sustained volume growth in emerging markets like Türkiye and a steady rise in power infrastructure demand outside China will continue to drive export growth for enamelled wire.

Overall, the enamelled wire industry will operate smoothly in H2 2026, amid the dual balancing of traditional off-season pressure and the resilience of emerging sectors. NEVs, power transformers, AI computing capacity, and exports outside China will continue to serve as industry "stabilizers," while marginal fluctuations in copper prices and the recovery of end-use demand for home appliances will be the two key variables determining the industry's operating rate, enterprise profitability, and market trends in H2.

![2026 China's Copper Anode Market H1: Supply Contraction Reverses the Pattern [SMM Analysis]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![2026 China Copper Foil Industry Half-Year Summary and Outlook [SMM Analysis]](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)