According to the latest SMM data, the comprehensive operating rate of China's copper billet enterprises continued its downward trend in June, with a significant polarization pattern between large and small mills. The tightening supply of recycled brass raw materials and the traditional end-use demand entering a deep off-season formed a dual drag, while only orders for copper billets from the new energy and AI supporting sectors provided structural support. Finished product inventories at enterprises accumulated slightly. Based on feedback from sample enterprises, market expectations for the industry in July were generally pessimistic, with the triple headwinds of off-season pressure, raw material bottlenecks, and material substitution resonating. The operating rate is expected to decline further.

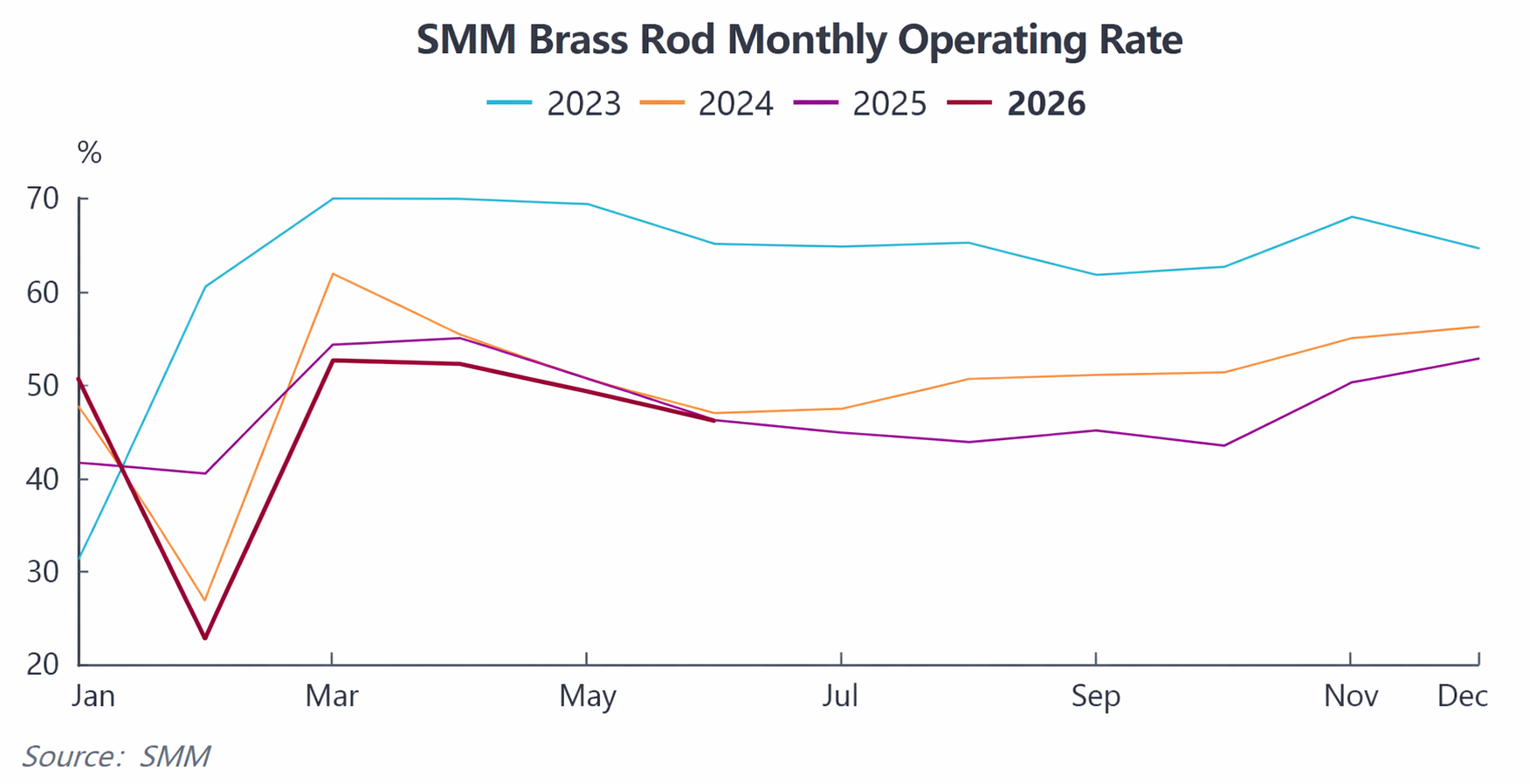

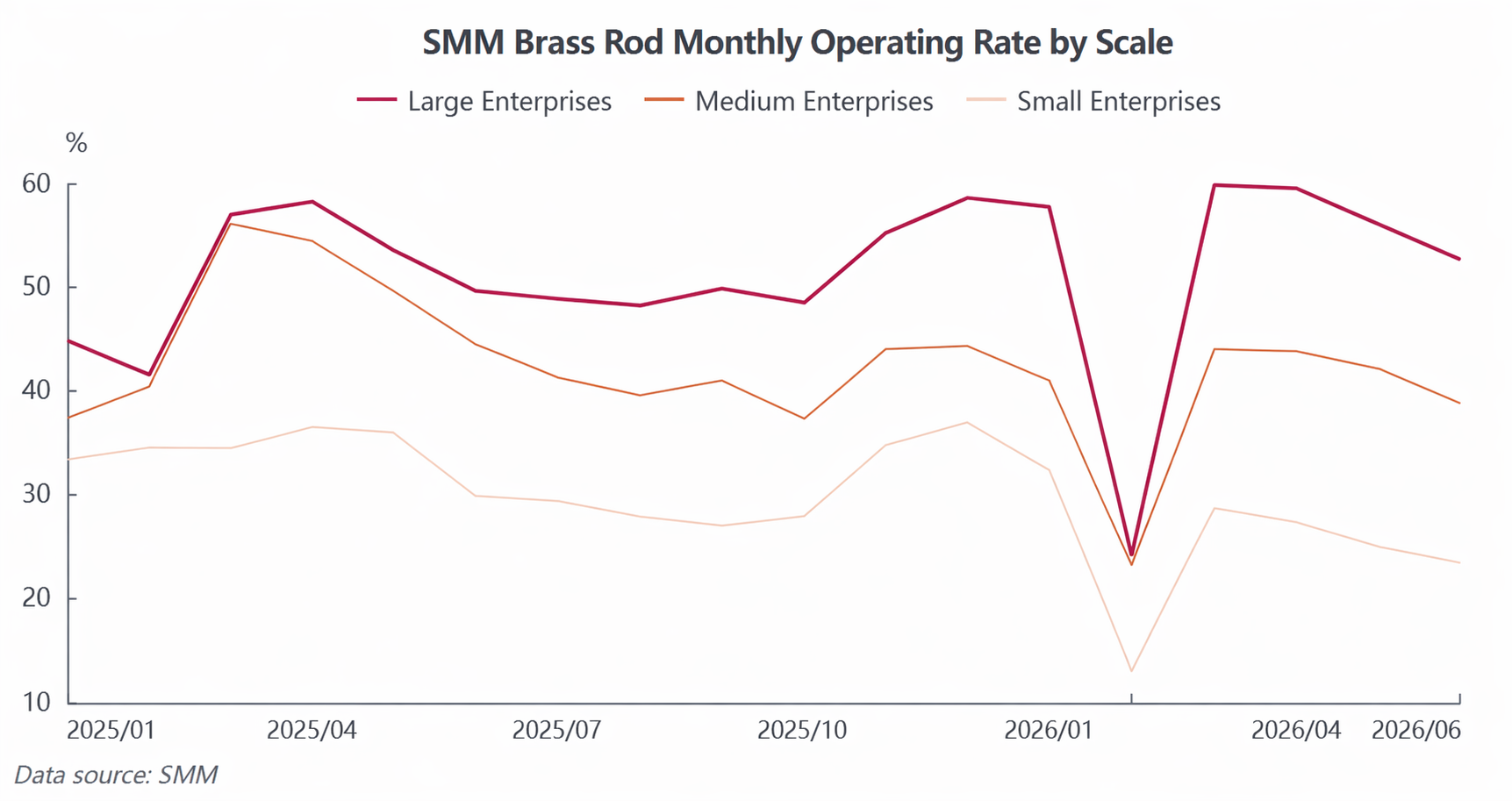

June industry operating data released, capacity polarization gap continues to widen: According to SMM statistics, the comprehensive operating rate of China's copper billet enterprises was 46.09% in June, down 3.18 percentage points MoM and pulling back slightly by 0.06 percentage point YoY, with overall production staying low. By enterprise scale, large leading enterprises leveraged stable raw material channels, ample capital reserves, and long-term quality client resources to show relatively stronger production resilience, with an operating rate of 52.6% in June; medium-sized enterprises were squeezed by both raw material and order pressures, restricting capacity release, with an operating rate of only 38.76%; small processing plants faced the most prominent pressure, with the operating rate falling to 23.44%, further intensifying the industry’s polarization.

Supply-side bottlenecks remain unresolved, with losses continuing to squeeze processing margins: Raw material shortages remain the core pain point constraining copper billet production. Currently, reverse invoicing controls for recycled resources have been continuously tightened, significantly shrinking the circulation of compliant scrap brass in China. The willingness to sell at the recycling end is low, narrowing the procurement channels for domestic secondary copper at processing plants; enterprises have instead increased their purchases of imported recycled brass, but overseas quotations have continued to rise, keeping import procurement costs high.

On the one hand, tight supply and purchasing premiums are driving up raw material costs; on the other, weak traditional end-user orders make it difficult to pass on processing charges, leaving most brass billet processing plants stuck in a “raw materials hard to buy, processing unprofitable” dilemma, with industry profit margins being continuously squeezed. Some small and medium-sized enterprises, facing losses from raw material costs, have proactively scaled back production schedules and controlled output to avoid risks, further dragging down the overall operating rate.

Demand-side off-season characteristics are prominent, with demand from old and new tracks showing a stark contrast: The seasonal weakening of demand has had a clear impact on the industry. June is the traditional off-season for downstream brass consumption in air conditioning, plumbing, valves, and ordinary hardware. Downstream end-user enterprises purchased as needed, with no concentrated stockpiling. The scale of new orders continued to shrink, and the overall trading atmosphere for brass billets turned sluggish.

Demand structure shows significant divergence: Traditional brass category orders continue to weaken, but high-purity copper billet demand provides a strong offset. Three electric systems for NEVs, large-power charging piles, PCS, as well as AI servers, GPU cooling modules, optical module precision pins and other parts continue to release stable rigid demand, driving copper billet enterprise orders to remain steady, becoming the only demand resilience sector in the industry.

However, sluggish procurement from traditional end-users drags down the overall shipment pace, copper billet enterprises' finished product inventories continue to accumulate, and inventory pressure gradually emerges, with the stockpiling turnover cycle in plants lengthening and production enthusiasm further dampened.

July market outlook: Multiple bearish factors resonate, and the operating rate is expected to decline again, based on frontline survey feedback from national sample copper billet enterprises, market expectations for July industry operation are generally pessimistic; improvement momentum is insufficient in the short term, and multiple negative factors will continue to ferment: raw material bottlenecks have no relief space in the short term, off-season pressure continues to intensify, and structural support is unlikely to boost the overall market.

On both the supply and demand sides, SMM expects the comprehensive operating rate of domestic copper billet to fall by 2.44 percentage points MoM to 43.65% in July, down 1.17 percentage points YoY, and the industry's low-level operation is expected to persist. In the short term, the copper billet industry still needs to wait for the recovery of the traditional peak consumption season and a substantial easing in the supply of recycled raw materials before seeing a simultaneous recovery in operating rates and profitability.

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![[SMM Analysis] May Indonesia Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)