According to the latest SMM data, the comprehensive operating rate of copper billet enterprises in China continued its downward trend in June, revealing a pronounced polarization between large and small producers. The industry faced a double whammy from tightening supply of recycled brass raw materials and traditional end-use demand entering a deep off-season. Only orders for pure copper billets used in NEV and AI applications provided structural support, while finished product inventories at producers accumulated slightly. Based on feedback from sample enterprises, market expectations for industry conditions in July are broadly pessimistic. A resonance of three bearish factors—off-season pressures, raw material bottlenecks, and material substitution—is expected to drive the operating rate lower again.

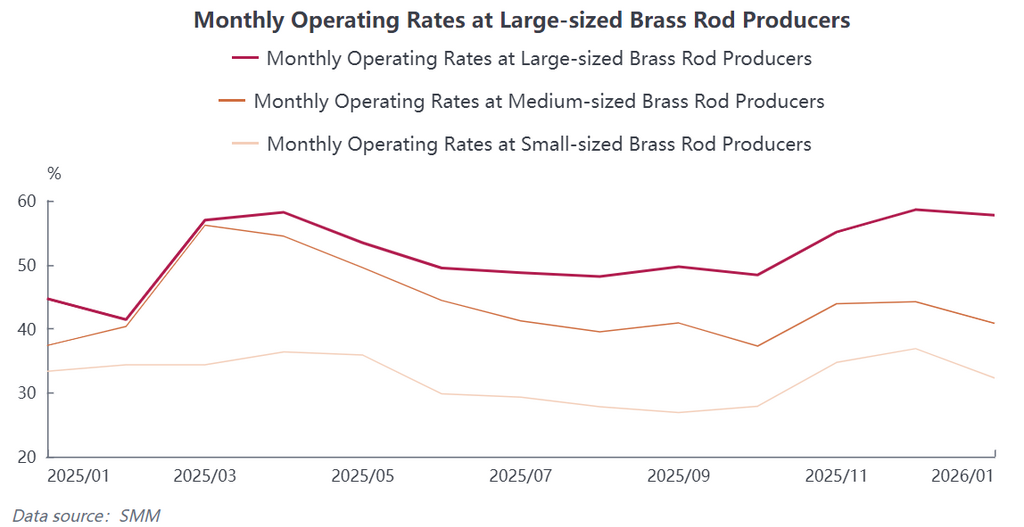

June industry operating data was released, with the capacity divergence among enterprises continuing to widen: SMM statistics show the comprehensive operating rate of China's copper billet enterprises was 46.09% in June, down 3.18 percentage points MoM and pulling back slightly by 0.06 percentage points YoY, keeping overall production at low levels. By enterprise size, large-scale leaders, buoyed by stable raw material sourcing channels, ample capital reserves, and long-term, high-quality client resources, demonstrated relatively stronger production resilience, managing a 52.6% operating rate. Medium-sized enterprises, squeezed from both the raw material and order sides, saw their capacity release constrained, with the rate at just 38.76%. Small-scale processing plants were the most notably under pressure, with their operating rate plunging to 23.44%, further intensifying the industry's polarization.

Raw material supply bottlenecks remain hard to solve, with losses continuing to compress processing margins: Raw material shortages are the core pain point limiting production in the copper billet industry. Currently, management of the reverse invoicing mechanism for secondary resources is being continuously tightened, causing domestic compliant circulation of scrap brass to shrink substantially. The recycling sector's willingness to sell is sluggish, and processing plants' procurement channels for domestic secondary copper are narrowing. Enterprises have been forced to increase purchases of imported secondary brass, but overseas suppliers' quotes are persistently rising, keeping import procurement costs high.

On one hand, cargo shortages and procurement premiums inflate raw material costs. On the other, weak traditional end-user orders make it difficult to pass on RC/TC, trapping most brass billet processing plants in the dilemma of "hard-to-buy raw materials and unprofitable processing." The industry's profit margins are being continuously squeezed. Some small and medium-sized enterprises, facing losses on raw materials, have taken the initiative to cut and control production to avert risk, further dragging down the overall operating level.

Seasonal demand-side weakness is pronounced, with demand performance a tale of two markets between old and new sectors: Seasonally weaker demand had a notable impact on the industry. June is the traditional off-season for brass downstream sectors like air conditioning, plumbing, valves, and ordinary hardware. Downstream end-users purchased as needed with no centralized stockpiling activity, causing new order volumes to keep shrinking and an overall sluggish transaction atmosphere for brass billets.

The demand structure showed significant divergence: While orders for traditional brass categories continued to weaken, demand for high-purity pure copper billets created a strong counterbalance. Stable, inelastic demand was being released from parts for NEVs' three electric systems (power battery, drive motor and electronic control system), large-power charging piles, Power Conversion Systems (PCS), as well as AI server cooling modules and precision pins for optical modules, sustaining steady orders for pure copper billet enterprises and making them the only resilient demand segment in the industry.

However, sluggish traditional end-user procurement weighed on the overall shipment pace, with finished product inventories at copper billet enterprises continuing to accumulate. Inventory pressure is becoming increasingly evident, the turnover cycle for held stocks is lengthening, and producers' willingness to produce has been further dampened.

July Market Outlook: A resonance of multiple bearish factors is expected to pull the operating rate down again. Based on frontline survey feedback from a nationwide sample of copper billet enterprises, market expectations for the industry's trajectory in July are broadly pessimistic. Driving forces for a short-term improvement remain insufficient, and multiple negative factors are set to keep simmering: There is no room for the raw material bottleneck to ease in the short term, traditional off-season pressures will continue to amplify, and structural support is unable to lift overall market conditions.

Weighing supply and demand dynamics, SMM expects China's comprehensive operating rate for copper billets to pull back 2.44 percentage points MoM to 43.65% in July, down 1.17 percentage points YoY, with the industry's low-level operating trend likely to persist. In the short term, the copper billet industry still needs to wait for a recovery in the traditional peak consumption season and a substantial loosening in recycled raw material supply before it can see a simultaneous repair of operating rates and profitability.

![[SMM Analysis] H1 2026 Review of the Copper Scrap Market Outside China: Copper Prices Surged, Tight Raw Material Supply Supported Firm Discounts](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![[SMM Analysis] May Indonesia Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)