SMM, July 7:

In the metals market:

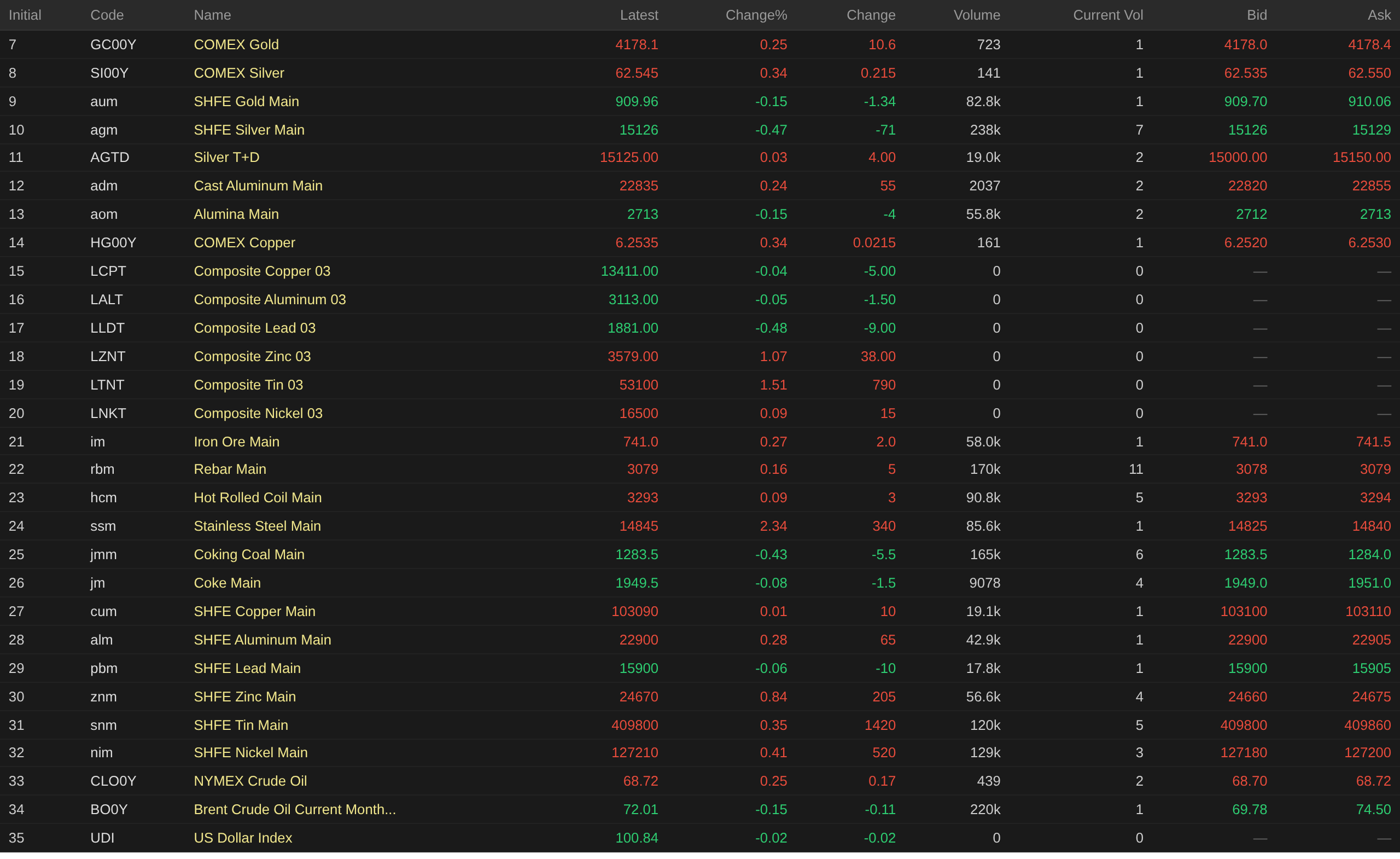

Overnight, domestic base metals mostly rose. SHFE copper edged up 0.01%, SHFE aluminum gained 0.28%, SHFE lead edged down 0.06%, SHFE zinc rose 0.84%, and SHFE tin added 0.35%. SHFE nickel increased 0.41%. Furthermore, the most-traded alumina futures fell 0.15%, while the most-traded foundry aluminum contract rose 0.24%.

Overnight, ferrous metals mostly rose. Stainless steel surged 2.34%, iron ore gained 0.27%, rebar edged up 0.16%, and hot-rolled coil added 0.09%. In the coking coal and coke segment, the most-traded coking coal contract fell 0.43%, while the most-traded coke contract lost 0.08%.

In the overseas market overnight, LME base metals showed mixed performance. LME copper and LME aluminum edged down, while LME lead fell 0.48%. LME zinc rose 1.07%, LME tin surged 1.51%, and LME nickel edged up 0.09%.

In the precious metals market overnight: COMEX gold rose 1.23%, and COMEX silver gained 2.33%. Overnight, the most-traded SHFE gold contract fell 0.15%, while the most-traded SHFE silver contract lost 0.47%.

As of 6:57 on July 7, the overnight closing prices were:

Macro front

Domestic side:

[Foreign Ministry responds to popularity of Chinese heat-relief products among European consumers] In response to reports that Chinese-made heat-relief products such as air conditioners, fans, and multi-functional sun umbrellas have been gaining popularity among European consumers, Foreign Ministry Spokesperson Mao Ning said at a regular press conference on the 6th that products that meet demand and offer good quality at reasonable prices will naturally be welcomed. The trade structure between China and Europe is a natural result driven by market demand and based on complementary strengths. Facts have proven that in China-EU trade, consumers benefit from affordable goods and suppliers earn profits; it is not a matter of coercion but a two-way choice that brings shared benefits. (Xinhua News Agency)

US Dollar:

Overnight, the US dollar index fell 0.04% to 100.87. The ISM Services PMI for June fell to 54.0 from 54.5 in May, slightly below the market forecast of 54.2, staying above the 50 mark, indicating the services sector remained in expansion territory but the pace of growth slowed. Although business activity and new order growth cooled, the employment gauge improved significantly, while the prices paid index pulled back to a four-month low, reflecting easing cost pressures for businesses. However, firms remained cautious about their business outlook for the coming year, with many surveyed companies citing considerable uncertainty over the economic and geopolitical outlook. (Wall Street CN)

Fed Governor Waller stated that the US labour market has stabilized while inflation has re-accelerated, and the current inflation risks now outweigh employment risks, a complete reversal from policy considerations a year ago. He noted that last year he supported cutting interest rates due to weakness in the job market, but now the policy focus should shift back to containing inflation. Markets are now turning their attention to the June CPI release on July 14, the last key inflation data before the Fed's July 28-29 meeting. Although international oil prices have pulled back to around $70/barrel, Fed officials still expect inflation to remain significantly above the 2% target by year-end. Markets anticipate the Fed will hike rates by September at the latest, with a roughly 25% probability of a July rate hike, as several officials have signaled further policy tightening. (Jin10 Data APP)

According to the CME FedWatch Tool, the probability of the Fed keeping rates unchanged in July is 74.3%, while the probability of a 25-basis-point cumulative rate hike is 25.7%. For September, the chance of rates staying unchanged is 42.9%, with a 46.2% probability of a cumulative 25 bps hike and a 10.8% chance of a 50 bps hike. (Jin10 Data APP)

CFTC data showed that as of June 30, global traders' bullish bets on the US dollar had climbed to nearly $40 billion, the highest level since 2015, extending the dollar's monthly rally driven by interest rate expectations. Markets bet that the Fed may keep rates higher or even hike again, pushing the dollar to a gain of about 2% in June. Analysts believe that expectations of Fed monetary tightening and US economic resilience have jointly supported the dollar, but some institutions note that recent softening in employment data could limit further upside. (Jin10 Data APP)

On the macro front:

Today will see the release of German industrial production m/m for May (seasonally adjusted), the UK Halifax house price index m/m for June (seasonally adjusted), French trade balance for May, the weekly change in US ADP employment for the week ended June 20, US trade balance for May, and China's foreign exchange reserves for June, among others. In addition, attention should be paid to: Turkey hosting the NATO summit through July 8; the US Trade Representative's Office holding a public hearing to review proposals for additional tariffs on 60 global economies; and Samsung Electronics releasing its Q2 earnings guidance.

Crude Oil:

Overnight, both oil futures edged lower, with WTI down 0.13% and Brent down 0.15%. Saudi Arabia's significant cut in crude selling prices heightened oversupply concerns, weighing on international oil prices. This marked at least the largest official price reduction by Saudi Arabia in 26 years, and its first sale at a discount since the 2020 price war. This sparked worries about whether other Middle Eastern producers would be forced to follow suit with price cuts, as their official prices are expected to be announced in the coming days. OPEC+ also agreed to further raise the production target by 188,000 barrels per day starting in August.

Saudi Aramco slashed its August official selling price for Arab Light crude to Asia by $11/barrel, the largest cut since at least 2000. As surging global supply intensified competition for buyers, Saudi Arabia cut its August official selling prices for key crude grades to Asian customers, the biggest reduction in at least 26 years. According to a price list, Saudi Aramco lowered the price of Arab Light crude for Asia in August by $11/barrel, to a discount of $1.50/barrel against the regional benchmark, a deeper cut than the $8/barrel expected in a survey of institutions. Middle Eastern crude prices have already been declining. After resuming exports from the Persian Gulf port of Ras Tanura, Saudi Aramco once raised crude shipments to about 90% of pre-war levels. Before the war, Ras Tanura was the main loading port for Saudi crude exports. Due to the blockade of the Strait of Hormuz during the war, Saudi Aramco diverted most of its crude flows to the Red Sea port of Yanbu. Earlier, the OPEC+ group agreed to continue with a small production increase in August. Now, as shipping resumes through the Strait of Hormuz, Gulf producers such as Saudi Arabia, Iraq, and Kuwait will be able to utilize their higher quotas. (Jin10 Data APP)

Data from the US Department of Energy (DOE) showed that US Strategic Petroleum Reserve (SPR) crude inventories fell by about 6.2 million barrels last week to 319.5 million barrels, the lowest level since April 1983. This decline is part of the US plan to release a cumulative 172 million barrels of crude from the SPR previously committed. (Jin10 Data APP)

![Guangdong Zinc: Downstream Purchase Willingness Low, Spot Premiums Decline [SMM Midday Review]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)

![Metals Broadly Fell; Lithium Carbonate and SHFE Silver Dropped over 2%, SHFE Zinc and Stainless Steel Rose over 1%, and European Container Shipping Futures Fell for a Second Straight Day [SMM Midday Review]](https://imgqn.smm.cn/usercenter/QnbfL20251217171735.jpeg)

![End-User Just-in-Time Procurement Difficult to Recover, Tight Supply Pushes Up North China Discounts [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/DpfYZ20251217171714.jpeg)