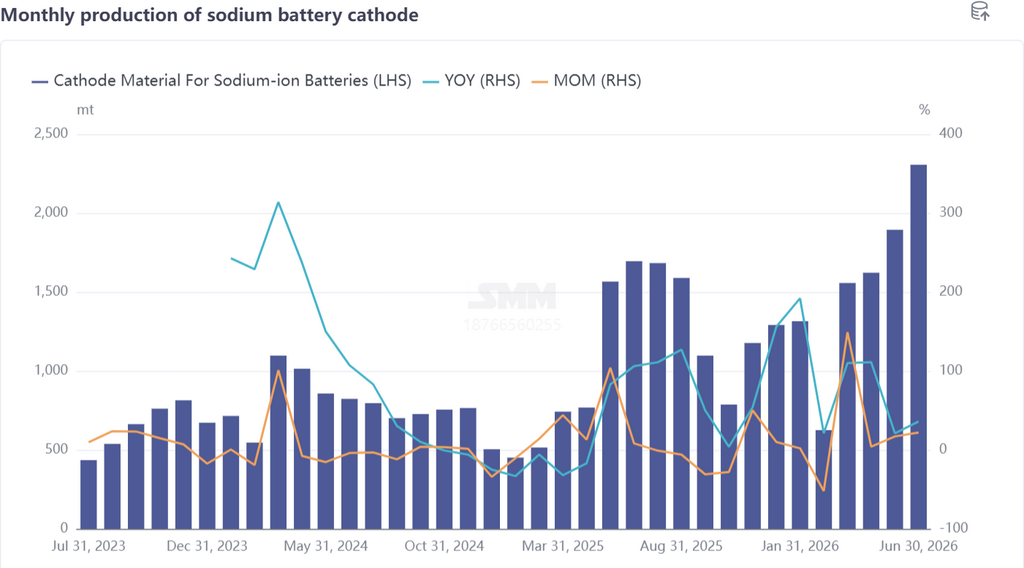

In June, the sodium-ion battery industry chain saw broad-based improvements. The cathode and anode segments continued to face undersupply, with clear seller’s market characteristics. The electrolyte and cell segments, which posted the most notable increases during this cycle, exhibited typical features of “volume growth amid persistent bottlenecks”—electrolyte capacity relied on conversion from lithium battery production, and core raw material shortages began to emerge, while the cell segment recorded nearly twofold YoY growth driven by dual boosts from energy storage and two-wheelers. The following focuses on electrolyte and cells to review June market dynamics and the H2 outlook.

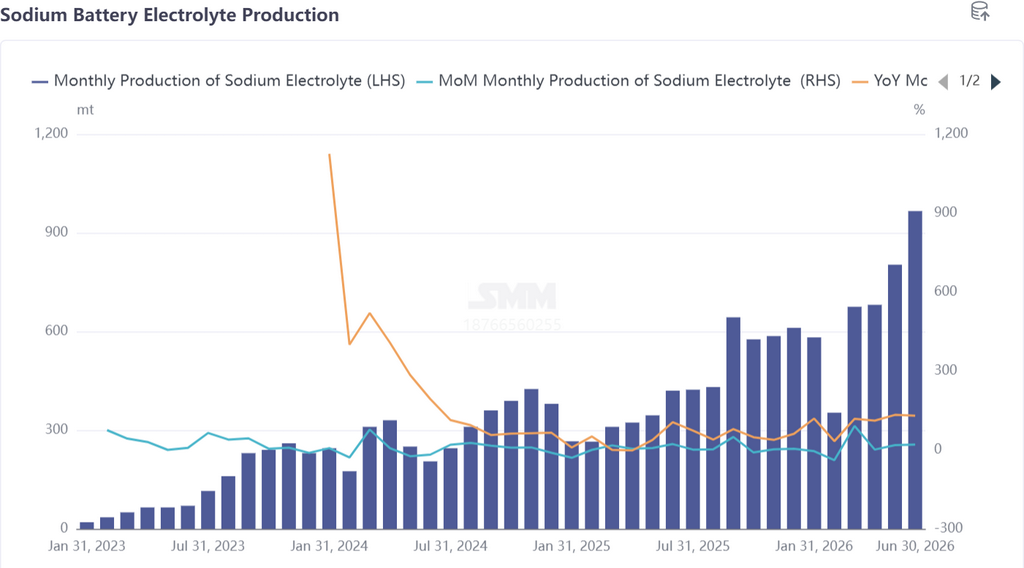

1. Sodium-Ion Battery Electrolyte: Notable Gains but Capacity Reliance; Raw Material Shortage Bottleneck Emerges

In June, sodium-ion battery electrolyte production surged 20% MoM and 130% YoY, a remarkable growth pace. However, it should be noted that current sodium-ion electrolyte capacity heavily depends on surplus capacity conversion from lithium battery electrolyte production, and actual output still struggles to fully match demand increases from the cell segment.

More critically, effective capacity for key upstream raw materials—NaPF6, NaFSI, NaODFB, etc.—remains scarce. The raw material capacity bottleneck acts as a rigid constraint on supply expansion in the electrolyte segment, making it difficult to achieve a rapid breakthrough in the short term.

From the competitive landscape perspective, the sodium-ion electrolyte market has relatively few players, and very few lithium battery electrolyte enterprises have proactively entered the sodium-ion track. The reason: some companies already deployed in sodium-ion electrolyte have tied their supply to downstream major manufacturers, while competitive pressures in the lithium battery electrolyte segment are already high. As a result, certain second-tier electrolyte enterprises tend to lead the charge into sodium-ion batteries to seize first-mover advantages.

Looking ahead to H2, if demand from downstream top-tier cell enterprises ramps up as expected, it will directly boost sodium-ion electrolyte shipments. In July, sodium-ion battery market demand is expected to continue increasing, which may prompt electrolyte companies to elevate their strategic focus on the sodium-ion battery segment. SMM expects July sodium-ion battery electrolyte production to grow 7% MoM and surge 143% YoY.

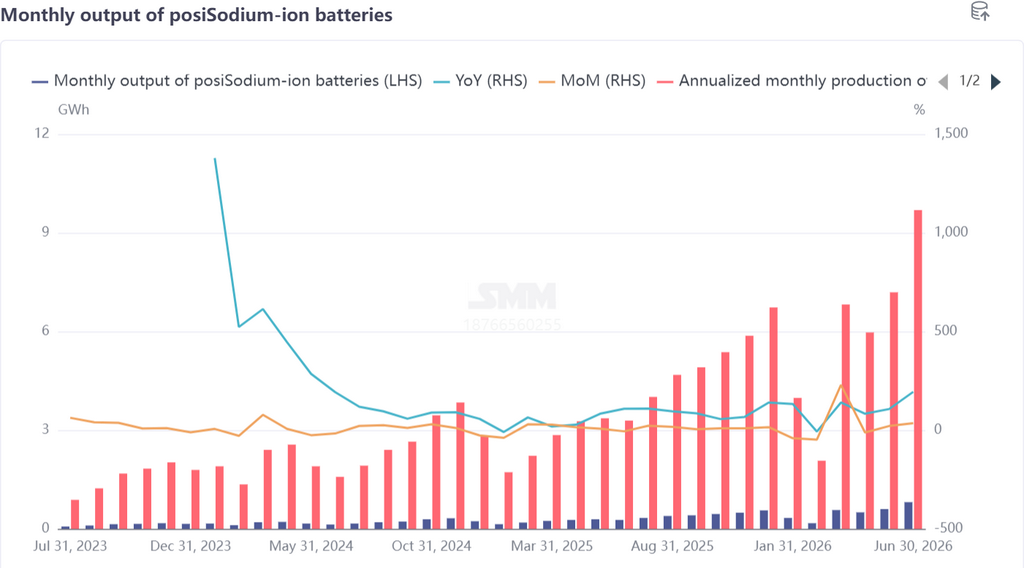

II. Battery Cells and End-Users: Building Growth Momentum, Energy Storage Volume Surge Expected

The undersupply in the electrolyte segment has not hindered the pace of volume growth in battery cells — strong downstream demand is becoming the core driver of the upturn across the entire industry chain.

In June, sodium-ion battery cell production rose 35% MoM and 194% YoY, the highest growth rate among the four major segments. The incremental growth was concentrated in the two-wheeler and ESS sectors, where the growth potential of the ESS sector is expected to become more pronounced in H2.

Currently, some battery cell manufacturers have begun preparing for H2 production plans, including building stable upstream supply systems and advancing capacity expansion. It is noteworthy that top-tier lithium battery players are gradually clarifying their H2 plans for sodium-ion batteries — sodium-ion batteries can meet the cost-performance requirements of specific application scenarios and also serve as a strategic approach to addressing lithium carbonate price fluctuations. Driven by these dual rationales, the investment by top-tier players in sodium-ion batteries is expected to increase.

In addition, toll processing of sodium-ion battery cells is quite common, which is currently an effective way to rationally utilize existing battery cell capacity and improve capacity utilization rates, while also alleviating the pressure of supply-demand mismatch to some extent.

Sodium-ion batteries are expected to see a notable volume increase in Q3, with clear volume growth signals driven by the dual engines of ESS and two-wheelers and accelerated planning by top-tier players. SMM expects July sodium-ion battery cell production to rise 23% MoM and 198% YoY.

III. Overview: Supply-Demand Mismatch Deepens, Industry Chain Enters Growth Window Period

In June, the sodium-ion battery industry chain showed high prosperity, with the undersupply pattern for anode and cathode materials persisting, while the electrolyte and battery cell segments exhibited a divergent trend marked by “volume growth amid bottlenecks.”

The electrolyte segment faces the hard constraint of scarce raw material capacity, and the limitations of relying on surplus lithium battery capacity conversion are gradually emerging; on the battery cell side, despite robust growth momentum, challenges remain in the stability of the upstream supply system. From the perspective of transmission mechanisms, the trend of large electrolyte manufacturers binding supply and the widespread adoption of toll processing models for battery cells both point to the industry chain transitioning from extensive volume release to refined supply-demand matching.

Looking ahead to H2, with the acceleration of energy storage project tenders, the implementation of large-scale procurement by top-tier lithium battery players, and the potential launch and delivery of sodium-ion battery car models, the sodium-ion battery industry chain is expected to enter a critical window for accelerated demand release. During this stage, enterprises with the capability to realize raw material capacity, stable quality control, and cost transmission advantages will be the first to break through in the reshaping competitive landscape.

![[Lithium Battery: Samsung SDI Plans Battery Lines For Solid-State, LFP, Sodium]](https://imgqn.smm.cn/usercenter/cTxNb20251217171727.jpg)

![[SMM Analysis] Sodium-ion Battery Market Experiences Robust Growth in June, July Outlook Remains Positive](https://imgqn.smm.cn/usercenter/jZvMC20251217171729.jpg)