SMM, July 2:

PV aluminum extrusion: This week, leading PV frame enterprises maintained a full production schedule. In July, downstream module manufacturers face delivery targets, and module production schedules are expected to edge up MoM from June, boosting supporting demand for PV frames and driving a higher industry production schedule. Currently, some frame enterprises in east and north China have reported that they will maintain full-capacity operations in the near term. On the raw material front, aluminum prices continued to drift lower this week, but PV frame enterprises did not adjust their restocking pace in response; they continued to purchase as needed against orders, without any concentrated restocking actions. Overall, the operating rate of China's PV frame enterprises is likely to hold up well in the short term.

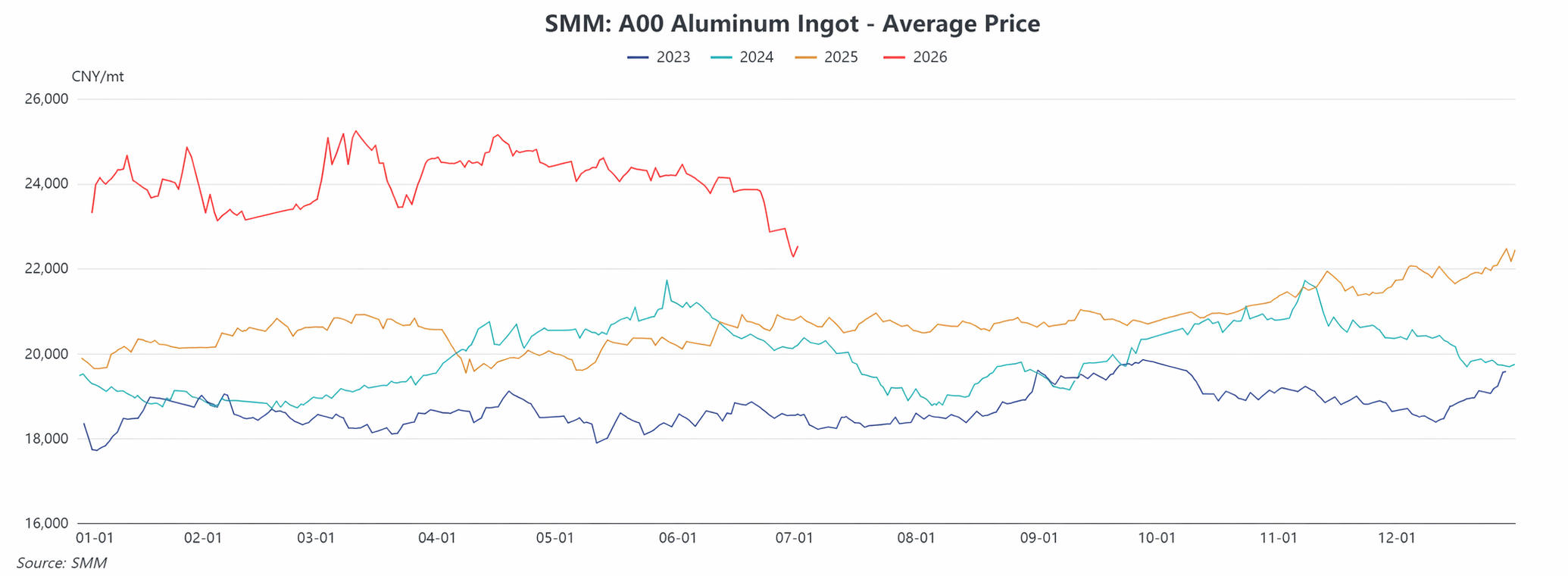

Raw material prices: During the period (Jun 29-Jul 2, 2026), the SMM A00 weekly average price was 22,560 yuan/mt, down 4.0% from the previous week. Overall, progress was made in indirect technical talks between the US and Iran, with discussions on fund repatriation and Strait of Hormuz security underway. Nuclear negotiations are about to commence, geopolitical risk premiums continue to converge, the dispute over Strait of Hormuz governance persists, and full resumption of transit through the Strait remains uncertain. A hawkish pivot by the US Fed boosted the US dollar index, tilting the global macro front toward a bearish stance and exerting downward pressure on aluminum prices. Domestically, the proportion of liquid aluminum continued to rise, and weekly aluminum ingot warehouse withdrawals hit a four-year high. The destocking pace accelerated once again, marking the biggest highlight recently, though absolute inventory levels remained in an elevated range. As geopolitical risk premiums continue to converge, compounded by expectations of new overseas project launches, macro headwinds dominated. LME aluminum faced considerable pressure in the short term, and SHFE aluminum followed suit under pressure in the absence of fresh positive macro catalysts. Aluminum prices are expected to remain in the doldrums. Next week, the most-traded SHFE aluminum contract is expected to trade within the 21,800-23,000 yuan/mt range, with LME aluminum trading in the $2,950-$3,150/mt range. Further attention is needed on: the actual pace of production resumptions at Middle Eastern aluminum enterprises after full Strait of Hormuz transit resumes; the US dollar's movement and its transmission to commodities after the hawkish Fed signals materialize; and whether domestic inventory destocking continues to accelerate.

![U.S. rate hike expectations pull back marginally, market focuses on tonight's nonfarm payrolls [SMM Precious Metals Macro Analysis]](https://imgqn.smm.cn/usercenter/yhuhG20251217171735.jpg)

![[SMM PV Flash] Total Installed Capacity of 3.8643 Million kW! Guizhou Issues Annual Construction Plans for 44 Wind Power and PV Projects](https://imgqn.smm.cn/usercenter/TygQH20251217171742.jpg)

![[SMM PV News] PV Energy Consumption and Efficiency National Standard Released, Strengthening the Green Development Bottom Line of the PV Industry](https://imgqn.smm.cn/usercenter/HKFoG20251217171742.jpg)