SMM July 2 News:

Fed Chairman Kevin Warsh stated on Wednesday that US inflation upside risks have clearly cooled over the past four weeks, easing market concerns about aggressive rate hikes; he also indicated that no further forward guidance would be released on subsequent interest rate policy, refusing to disclose whether the US Fed needs to consider a rate hike at its next meeting; the US dollar weakened, and precious metals rebounded. As of around 16:09 on July 2, COMEX gold dropped 0.11% to $4,077.9/ounce; SHFE gold main contract rose 1.53% to 890.66 yuan/g; COMEX silver dropped 1.1% to $59.845/ounce; SHFE silver main contract rose 1.91% to 14,650 yuan/kg; silver T+D rose 2.95% to 14,551 yuan/kg.

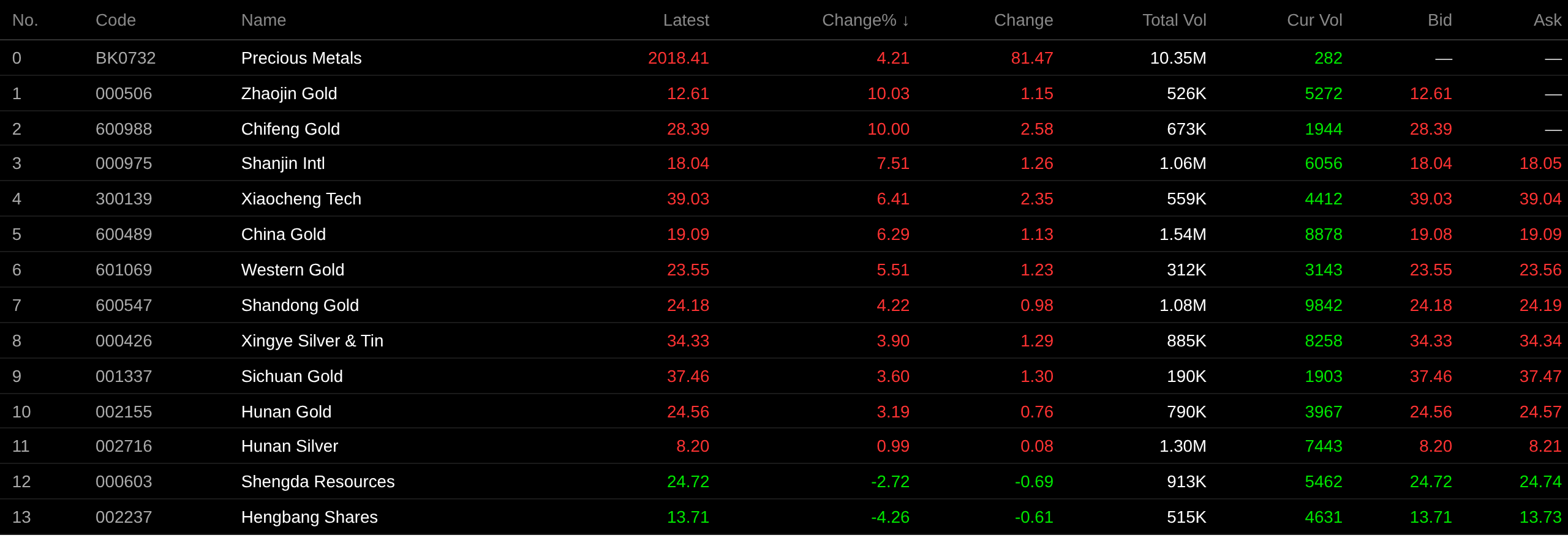

In the precious metals stock market, as of the close on July 2, the precious metals sector rose 4.21%, with individual stocks: Zhaojin Gold and Chifeng Gold hit their daily limit up, while Shanjin International, Xiaocheng Technology, Zhongjin Gold, and Western Gold led the gains.

News

[Warsh: Inflation Eases Over Past Four Weeks, AI Is Reshaping Economy, Forward Guidance Loses Necessity]On July 1, at the ECB's annual central bank forum in Sintra, Portugal, Warsh again clearly stated that the US Fed would not provide forward guidance on the future interest rate path, hoping that policymakers can engage in thorough discussions based on the latest data at each meeting, rather than previewing the policy direction to the market in advance. He said that US inflation risks had eased over the past four weeks, and the supply expansion brought by AI could profoundly change how the economy operates, with the US at the center of this transformation, but whether AI ultimately leads to inflation or deflation should be judged by the central bank based on data.Warsh said the US Fed is “charting a new path” and will no longer hint at the direction of interest rates in advance as it did in the past. He said: “We will hold our next meeting in four weeks, and I hope we can have a real family-style debate then.” He reiterated that forward guidance is not the right policy in the current economic situation, and the US Fed will continue to base its decisions on the latest economic data in the future, rather than committing to a policy path in advance.This means that the US Fed will rely more on real-time economic data rather than sending policy signals to the market in advance.

Spot Market

Silver

In the spot market: On July 2, the reference average factory price of SMM 1# silver in the morning was 14,558 yuan/kg, up 3.35% from the previous trading day.

In the spot market, overall offers remained firm early in the month, but transaction follow-through was slightly weak, and consumption performance fell short of expectations. As silver prices rebounded slightly, downstream wait-and-see sentiment intensified. In Shanghai, morning offers were mainly at TD+5 to +15 yuan/kg. Some smelters quoted on the high side, but actual buying interest was weak, with most deals clustered around TD+10 yuan/kg. In other regions, low-priced cargoes had basically been cleared, while offers in Shenzhen were mostly around TD+5-10 yuan/kg. Today, the market quoted premiums for the SHFE most-traded contract 2608 at a discount of 30 to 20 yuan/kg. Overall, a slight cooling in rate-hike expectations provided some support for precious metals prices. At the start of the month, the spot direction remained unclear. Maintenance at copper plants last month caused a slight disruption on the supply side, and offers generally maintained a slight premium structure.

Views From Various Parties

Regarding the outlook for precious metals, some institutions’ views are as follows:

On July 1, the World Gold Council released the “2026 Mid-Year Outlook for the Global Gold Market.” Looking ahead to H2, gold’s valuation framework indicated that gold will continue to serve as a barometer of the global macro economy, with three main possible scenarios. From current levels, gold prices were broadly in line with market consensus: the market expected the US Fed to raise rates at least once in 2026, most likely in October; the Bank of England, the Bank of Japan, and the European Central Bank were all set to tighten policy; and US Q2 inflation was expected to peak, near $3.9. If there were no major changes in the above environment, gold prices may trade around $4,100/oz within the year, with a fluctuation range of about ±5. If geopolitical or economic conditions deteriorate, or if interest-rate expectations shift, gold is expected to regain its upward momentum; however, only sufficiently strong signals of a global economic slowdown would be likely to drive a breakout to the upside. On the downside, a stronger US dollar, rate hikes exceeding expectations, and a rebound in market risk appetite were the main headwinds for gold prices; if gold prices remain below $4,000/oz, it may trigger further selling. However, based on historical performance, if gold prices fall by more than 10% from current levels, it may trigger “buy-the-dip” demand from long-term investors in multiple regions.

State Street Investment Management said that, as the opportunity cost of holding gold and heightened volatility weighed on investor sentiment, bullish gold trades had been weak, and spot gold prices repeatedly tested the $4,000/oz support level. State Street believed that, although gold prices may be more volatile than in 2024-2025, the gold bull-cycle still has upside room, and the US Fed’s hawkish policy shift was expected not to change gold’s post-pandemic structural trend. State Street noted, “Since the US-Iran conflict, China’s retail gold imports have surged, and local premiums have risen in tandem, reflecting tightening fundamentals in China’s gold supply-demand balance.”State Street expects that over the next six to nine months gold prices could rise to the $4,750 to $5,500 per ounce range, with strong support in the $3,750 to $4,000 per ounce area. However, compared with the macro environment from January to February, the probability of gold prices reaching $5,500 to $6,250 per ounce is relatively small. (Zhitong Finance)

State Street Investment Management strategists noted in a report that gold prices could reach $5,000 per ounce by early 2027, as the gold bull cycle remains persistent. They believe that as U.S. government debt rises, gold's role as a currency hedge is expected to be supported, while actual demand for gold remains strong. Global gold fund holdings (as a share of global mutual fund and exchange-traded fund assets) currently remain below State Street's target allocation of 3% to 10% for most portfolios. Moreover, they added that a hawkish pivot by the Fed should not alter gold’s structural post-pandemic trend. State Street expects base bullion prices to rise to $4,750 to $5,500 per ounce in the next six to nine months. (Jinshi Data APP)

Analysts at Saxo Bank said, "The market has not yet attracted enough buying interest to establish that level as a support level." They also pointed out, "Even though energy prices have pulled back recently, investors still expect the Fed may further tighten monetary policy to combat an inflation rebound, and as a result, gold prices fell 14% in Q2, marking the worst quarterly performance since 2013." (Jinshi Data APP)

CICC's latest research report pointed out that gold may have already overpriced rate hike expectations. Fed rate hikes are still not the base case, and the gold market may have overly priced in rate hike expectations, leaving room for a pullback this year. CICC's macro team believes that employment and consumption pressures, along with the expanding financing needs of the U.S. AI economy, may make it difficult for the Fed to materially turn hawkish, and monetary policy may be "hawkish in words but dovish in action." Based on the implied interest rate expectations model from gold prices, it is estimated that the current gold price around $4,000 per ounce has fully priced in three to four rate hikes, exceeding the rate hike expectations priced in by the interest rate futures market. Looking ahead, after the decline in oil prices is further reflected in U.S. short-term inflation data, the gold market's pricing of rate hike expectations may be corrected, and futures market short-term funds may have opportunities to cover short positions. (Jinshi Data APP)

Li Xunlei, Deputy Director of the China Chief Economist Forum, pointed out that gold's long-term trend exhibits long bear markets and short bull markets. Since 1971, 30 years have been bear markets and 25 years have been bull markets, but each bull market has seen gains of over fivefold. A bull market typically lasts around 10 years. This gold bull run has now lasted nearly 10 years, with prices tripling during that time, so caution is warranted at this stage. (Jin10 Data App)

Deutsche Bank analyst Michael Hsueh said the bank has cut its Q3 gold price forecast by over 20% to $4,300/oz and lowered its Q4 forecast by 17% to $4,800/oz. "Potential investors who would normally provide support are notably absent," he said, pointing to weak demand for exchange-traded funds and reduced buying appetite in some countries. (Jin10 Data App)

Macquarie said profit-taking weighed on silver prices last month, and price action is once again driven by macro factors amid rising expectations for US Fed interest rate hikes. Similar to gold, silver prices are expected to move sideways for the rest of the year, then gradually decline into 2027, with inflationary pressures and the likelihood of further US Fed rate hikes limiting upside room. The higher inflation and bond yields, the greater the downward pressure. Silver, in particular, has been more susceptible to a pullback after outperforming gold, driven by bullish sentiment fueled by supply tightens, low inventory, and strong demand. Historically, silver pullbacks tend to be rapid. Macquarie expects silver to trade at $70/oz in Q4 this year and pull back to $65/oz by the end of 2027. (Jin10 Data APP)

Recommended reads:

![Platinum and Palladium Market Price Review and Expectations Brief Commentary (July 2, 2026) [SMM Weekly Platinum & Palladium Review]](https://imgqn.smm.cn/usercenter/OQqCm20251217171736.jpg)

![U.S. rate hike expectations pull back marginally, market focuses on tonight's nonfarm payrolls [SMM Precious Metals Macro Analysis]](https://imgqn.smm.cn/usercenter/yhuhG20251217171735.jpg)

![Silver V-Shaped Rebound with 2.9% Weekly Gain, Non-Farm Payrolls Data May Lead to Directional Breakthrough [SMM Silver Weekly Review]](https://imgqn.smm.cn/usercenter/fNuSg20251217171735.jpg)