SMM July 2 news:

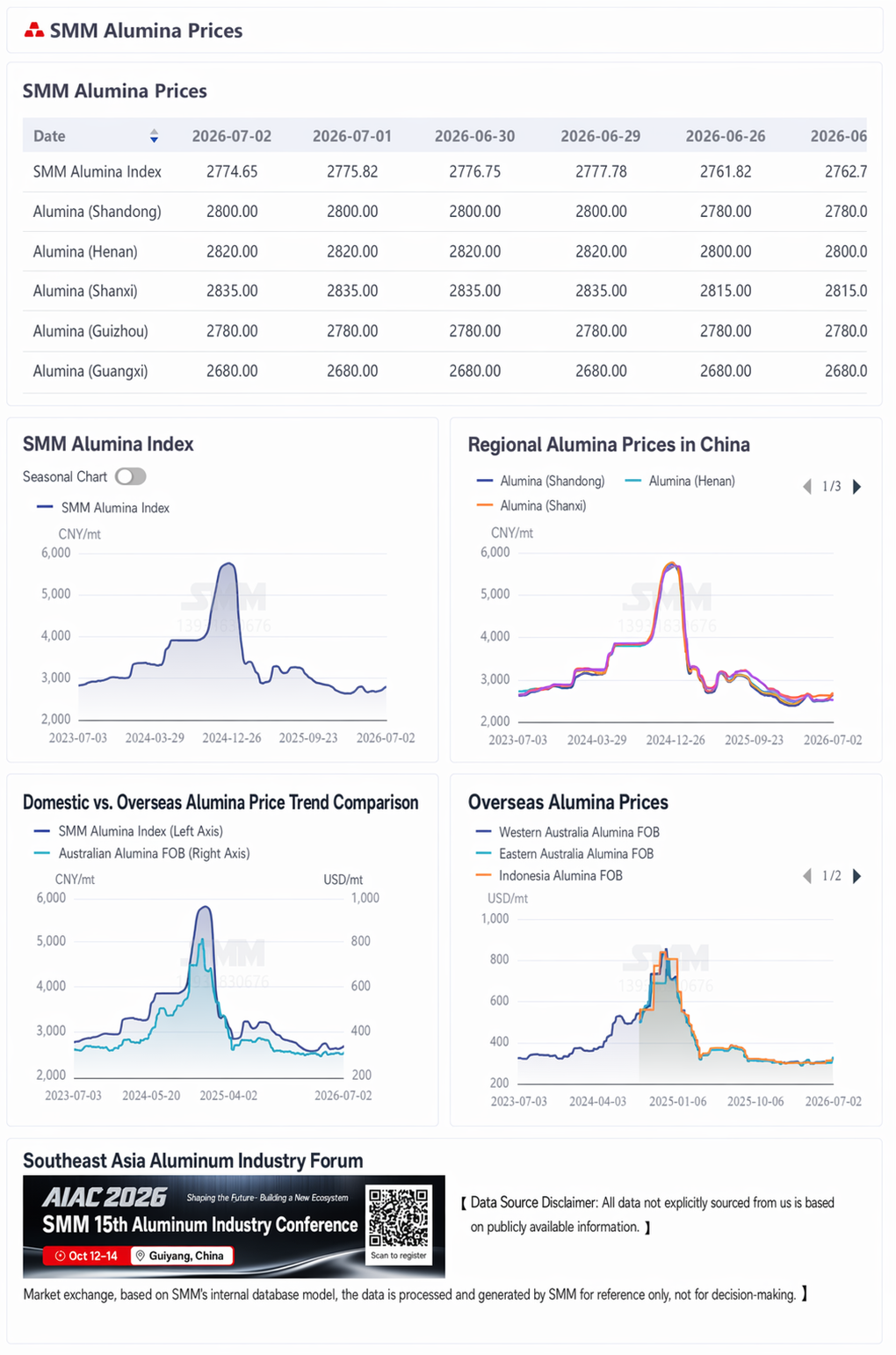

Price review: As of this Thursday, the SMM alumina index stood at 2,693.19 yuan/mt, up 11.9 yuan/mt WoW from last Thursday. Specifically, Shandong was quoted at 2,770–2,830 yuan/mt, up 20 yuan/mt from last Thursday; Henan, 2,790–2,850 yuan/mt, up 20 yuan/mt; Shanxi, 2,800–2,870 yuan/mt, up 20 yuan/mt; Guangxi, 2,630–2,730 yuan/mt, unchanged; and Guizhou, 2,760–2,800 yuan/mt, unchanged.

Markets outside China: As of July 2, 2026, FOB Western Australia spot alumina was $330/mt, with an ocean freight rate of $32.3/mt and a USD/CNY selling rate around 6.80. This translates to a delivered price at major Chinese ports of about 2,865.02 yuan/mt, exceeding the alumina index by 90.37 yuan/mt. This week, one overseas spot alumina deal was heard; details:

(1) On June 25, 2026, 30,000 mt of alumina were traded at $330/mt FOB Western Australia, for August shipment.

China market: According to SMM data, as of this Thursday, total built metallurgical-grade alumina capacity in China was 118.42 million mt/year, with operating capacity at 87.95 million mt/year. The national weekly alumina operating rate fell 0.23 percentage point WoW to 74.27%. Among them, Shandong’s weekly alumina operating rate rose 0.95 pp WoW to 89.31%; Shanxi’s rose 0.41 pp to 64.31%; Henan’s fell 3.5 pp WoW to 56.83%; Guangxi’s edged up 0.43 pp WoW to 76.13%; and Guizhou’s increased 3.13 pp WoW to 81%.

Spot market: Two deals were concluded this week. In Xinjiang, 10,000 mt of spot alumina were procured, with a delivered price of around 3,135 yuan/mt. In Gansu, spot alumina was procured at a delivered price of 3,000 yuan/mt.

As of this Thursday, alumina prices continued to rise, but the increase had markedly narrowed, with signs of weakness emerging in recent days and the overall spot transaction center shifting lower. Inventory: According to SMM, total alumina inventory in China edged up 1,000 mt MoM to 7.015 million mt, with the overall change relatively small. By component, raw material inventory at aluminum smelters fell 47,000 mt to 3.364 million mt, mainly because current high spot alumina prices prompted some smelters to actively reduce their in-factory high-priced inventory, leading to the decline. In-factory inventory at alumina refineries increased by a slight 2,000 mt to 1.231 million mt, as maintenance-related output reductions in Shanxi were offset by capacity additions in south China, limiting the overall change. At ports, as new vessels arrived successively, port inventory increased by 31,000 mt to 891,000 mt this week. Warrant inventory, affected by invoicing issues and the spread between futures and spot prices, saw weakening willingness to ship to delivery warehouse, decreasing by 9,000 mt to 263,000 mt. In-transit and station platform inventory increased by 23,000 mt to 1.267 million mt, mainly because warrants gradually matured and turned into spot cargo, together with continuous shipments from Guangxi, leading to accumulation of in-transit cargoes. Overall, the operating pattern of alumina is expected to change little next week. Some enterprises using domestic ore may schedule maintenance due to ore supply issues, but the impact on monthly production will be limited, and overall inventory will remain at current levels. Price side, as regional alumina mismatch gradually eases, the spot price center is expected to pull back, and the subsequent trend will be under pressure.

[Except for public information, all other data are processed by SMM based on public information, market communication, and SMM's internal database models, for reference only and do not constitute decision-making advice.]

![[SMM Analysis] The secondary aluminum market outside China remains in the doldrums, with supply-demand fundamentals driving a price pullback.](https://imgqn.smm.cn/usercenter/zlIyw20251217171654.jpg)