SMM July 10:

I. Review of the Primary Aluminum Billet Market in H1 2026

In H1 2026, China’s primary aluminum billet market, caught between wild swings in aluminum prices and sluggish end-use demand recovery, underwent a turbulent journey from deep pressure to staged recovery. Ahead of Chinese New Year, record-high aluminum prices combined with early exits by downstream players caused processing fees to “flash crash” into negative territory in Q1, plunging the industry into an unusual deep discount quagmire. In Q2, as aluminum prices pulled back and short-term supply disruptions emerged frequently, processing fees rebounded strongly, briefly touching near three-year highs, and the profitability of aluminum billet enterprises improved markedly. However, although end-use demand showed signs of recovery, the persistent weakness in construction extrusions continued to constrain upside room. Whether the “dawn” under a weak supply-demand pattern can last still needs to be examined from various fundamental dimensions.

1. Supply-Demand Fundamentals

Supply Side: Initially Weak Then Rebounding, Production Contracted YoY

In H1 2026, China’s existing capacity of primary aluminum billets was approximately 32.2 million mt. The capacity scale continued to expand mildly, but the expansion pace in south-west China had noticeably slowed, with sporadic new project startups and progress toward full production lagging behind previous years. Meanwhile, some enterprises accelerated diversified product layouts. The output proportions of products such as aluminum rod, alloy ingot, and slab continued to increase, passively squeezing the share of aluminum billet production. Under the interplay of various factors, individual producers even remained in a state of long-term production line shutdown due to prolonged losses, insufficient funds, or strategic shifts.

In terms of operational performance, the average capacity utilization rate of the primary aluminum billet industry in H1 was around 51.9%, with monthly operating rates showing a pronounced “V-shaped” recovery trajectory.

Total production of primary aluminum billets in China in H1 was approximately 8.364 million mt, and the overall supply side went through three stages of evolution:

Phase 1 (January-February): A cliff-like decline. In January, aluminum prices surged all the way to a record high by month-end, forming a significant divergence from weak fundamentals. Downstream players were unwilling to chase prices for stockpiling ahead of Chinese New Year, and extrusion enterprises generally took early holidays, with aluminum billet enterprises bearing the brunt of order declines. Processing fees experienced a “flash crash,” with quotes in three regions sinking deep into negative territory. Under dual pressures from inventory and capital, the scope of production suspensions for maintenance and voluntary production cuts expanded. Output in provinces including Guangxi, Xinjiang, Inner Mongolia, Qinghai, Guizhou, and Henan dropped by over 10% MoM. During the Chinese New Year holiday in February, downstream operations halted completely while billet plants maintained a certain operating load. In the first week after the holiday, in-factory inventory approached 500,000 mt, surging nearly threefold from pre-holiday levels. Qinghai, Sichuan, and Henan saw MoM declines even exceeding 40%, and the February operating rate dropped to 41.4%, a near four-year low.

Phase two: Mild recovery that fell short of expectations, March-April.After the Lantern Festival, downstream operations resumed fully, raw material purchase willingness rebounded, combined with the PV and battery sectors entering a sprint period for export orders, the recovery of industrial billet orders provided some support on the supply side. However, the construction extrusion industry's sluggish trend remained unchanged, processing fees for 6063 construction billets continued to linger below the cost line, actual transactions relied on 'volume discounts', and the overall recovery in the March peak season fell short of expectations. In April, with the end of the export order sprint period, industrial billet orders pulled back, some mid-to-large aluminum billet enterprises implemented preemptive production cuts, and the operating rate edged down to 52.5%, remaining low compared to peak-season levels in previous years.

Phase three: A rebound that exceeded expectations, May-June.From late April, high aluminum prices pulled back coupled with short-term supply-side disruptions, processing fees in three regions rebounded strongly and rose significantly above the cost average, greatly boosting production willingness among aluminum billet enterprises. In May, the operating rate rebounded sharply by 4.3 percentage points MoM to 56.8%. In June, the positive trend continued, as accelerating decline in aluminum prices pushed processing fees to a near three-year high, delivering substantial processing margins, and the operating rate rose to 57.2%, turning positive YoY. Notably, in May, environmental protection checks were stationed in the Baise area of Guangxi, where local smelter production adjustments led to a reduction in liquid aluminum raw material supply for surrounding billet plants, some of which have not yet fully recovered. Producers in Yunnan and Guizhou also cut their aluminum billet output share due to temporary maintenance and adjustments in product mix ratios. Furthermore, as China's aluminum capacity standardization progressed, liquid aluminum supply tightened in south-west China, and some billet plants experienced passive production cuts amid high processing fees, partly limiting the supply-side release space.

Demand side: Weak recovery as the main theme, structural divergence intensifies.

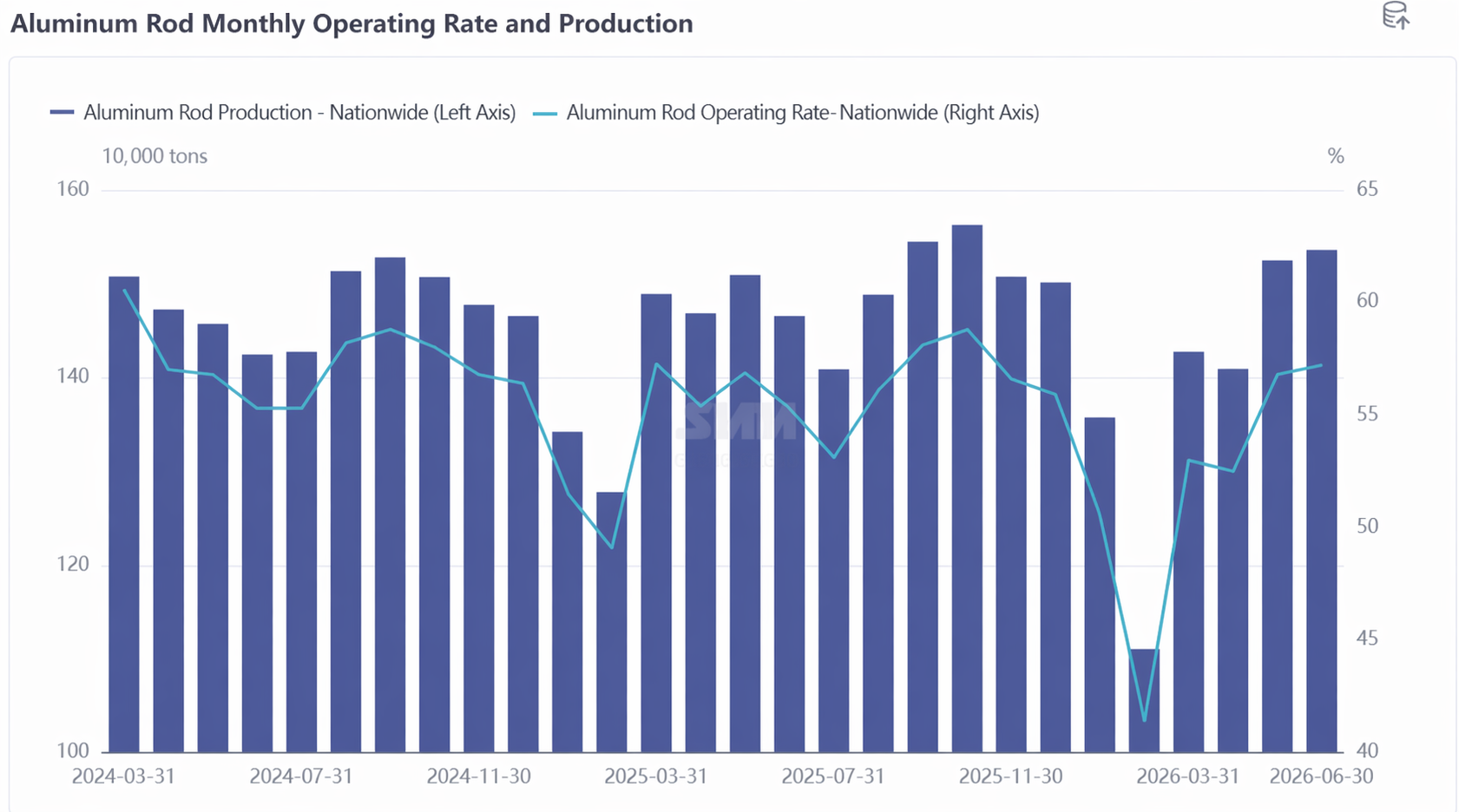

Aluminum extrusion, as the direct downstream of primary aluminum billets, showed overall mediocre performance in H1. Although industrial extrusion volumes have gradually overtaken construction extrusion volumes, generating some demand for industrial billets, the majority of billet plants remained focused on competing in the ordinary construction billet segment. Transitioning to industrial extrusion faces high barriers in terms of capital, technology, orders, and channels, and progress has been slow under the current stability-oriented approach.

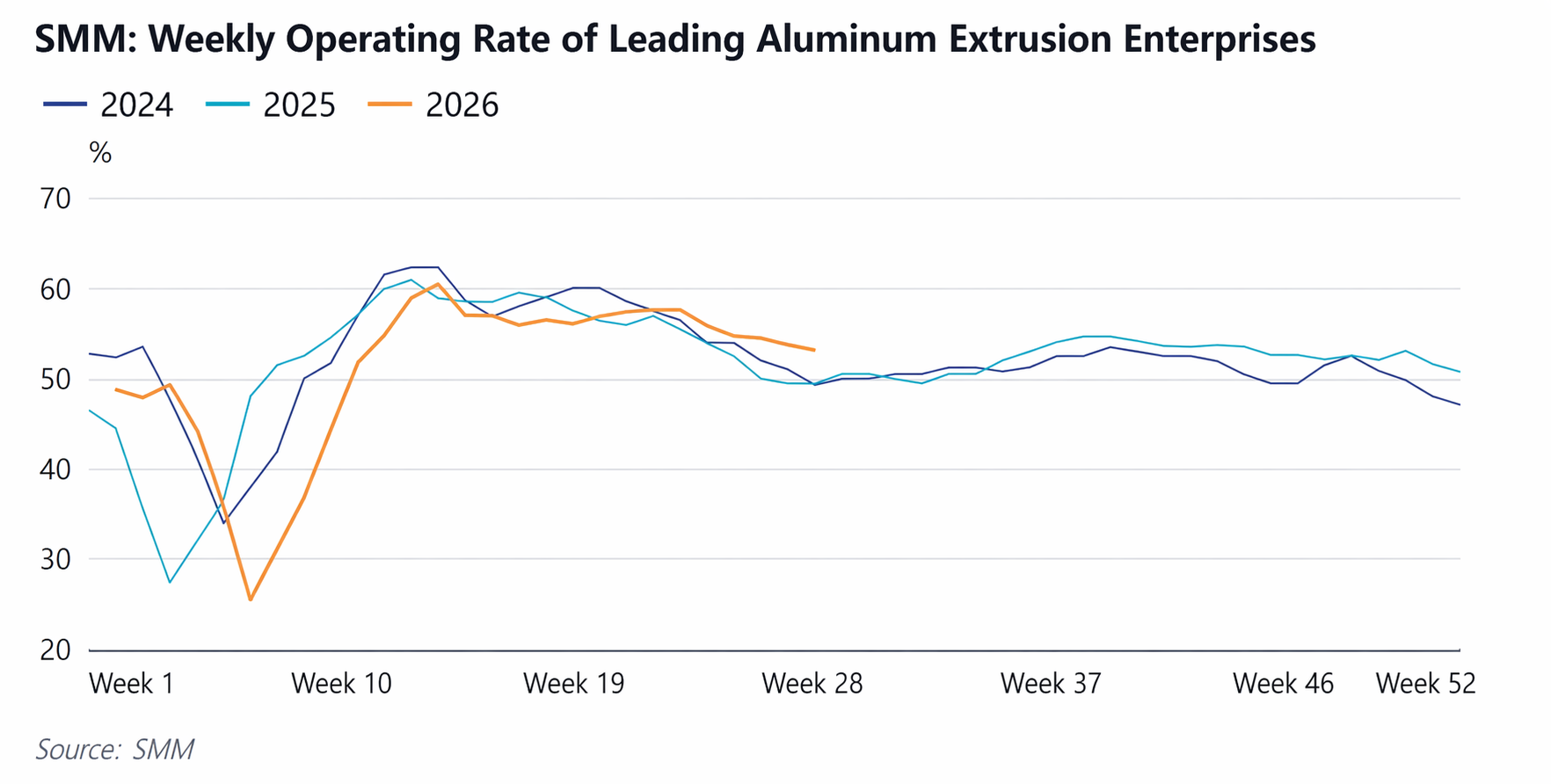

According to SMM data, the average monthly operating rate of sampled aluminum extrusion enterprises in China in H1 2026 declined compared to the previous two years, with the February operating rate dropping to a new low in recent years. The Chinese New Year severely disrupted enterprises' production pace, with an increasing proportion withdrawing from the market early before the holiday, shutting down during the holiday, and resuming production at a slower pace afterward. In addition, some extrusion plants adopted shift adjustments, rotating days off, or outright shutdowns during various holidays, further lowering the average operating rate.

The core constraints on the demand side were as follows: first, construction extrusion extended its weak demand pattern, with end-user orders lacking growth momentum, and involution intensifying in the construction extrusion billet segment; second, industrial extrusion orders were concentrated at large-scale plants, leaving small and medium-sized enterprises in a precarious operating environment, while some industrial extrusion products had long payment cycles, dampening enthusiasm for taking orders; third, wild swings in aluminum prices heightened the downstream wait-and-see sentiment, prompting enterprises to adopt an increasingly cautious raw material stockpiling strategy, generally purchasing just-in-time and as needed; fourth, when aluminum billet processing fees were elevated, enterprises with in-house casting capabilities tended to directly purchase aluminum ingots for remelting processing, exerting substitution pressure on aluminum billets; fifth, the overall supply of aluminum billets was ample—although certain brands and specifications were temporarily in short supply, supply was generally sufficient most of the time, leaving downstream with little motivation to stockpile. Overall, the industry's oversupply situation persisted throughout H1, with the demand recovery pace notably lagging behind the supply-side repair speed.

Nevertheless, the mild recovery on the demand side in Q2 was also worth noting. After entering May, the operating rate of China's aluminum extrusion sector gradually rebounded, continuing a mild MoM recovery. For construction extrusion, some enterprises organized production based on large-scale engineering project orders on hand, providing support for overall operations. Enterprises in Shandong reported that as temperatures steadily rose, the northern region entered a construction window, and end-use demand such as home decoration renovations and door/window replacements saw some volume expansion. For industrial extrusion, a temporary weakening of aluminum prices stimulated downstream purchasing willingness: PV frame enterprises in Hebei received some delivery orders in early June, and production scheduling increased, driving up operating rates. Although the real estate market recovery remained sluggish, large-scale engineering orders held volume advantages with long delivery cycles, and combined with seasonal consumption recovery, the marginal improvement in Q2 demand provided fundamental support for the processing fee rebound.

H1 Supply-Demand Balance Summary: In H1 2026, the primary aluminum billet market exhibited a phase characterized by "supply contracting faster than demand weakening." On the supply side, impacted by multiple factors including high aluminum price volatility, deeply negative processing fees, tightening liquid aluminum raw material supply, and substitution from diversified products, semi-annual production declined YoY. On the demand side, although seasonal recovery emerged, the slump in construction extrusion dragged down the overall pace of recovery. Amid this dual weakness, temporary supply-demand mismatches created conditions for the Q2 processing fee rebound, but a fundamental improvement in the market's underpinnings still requires time.

2. Inventory

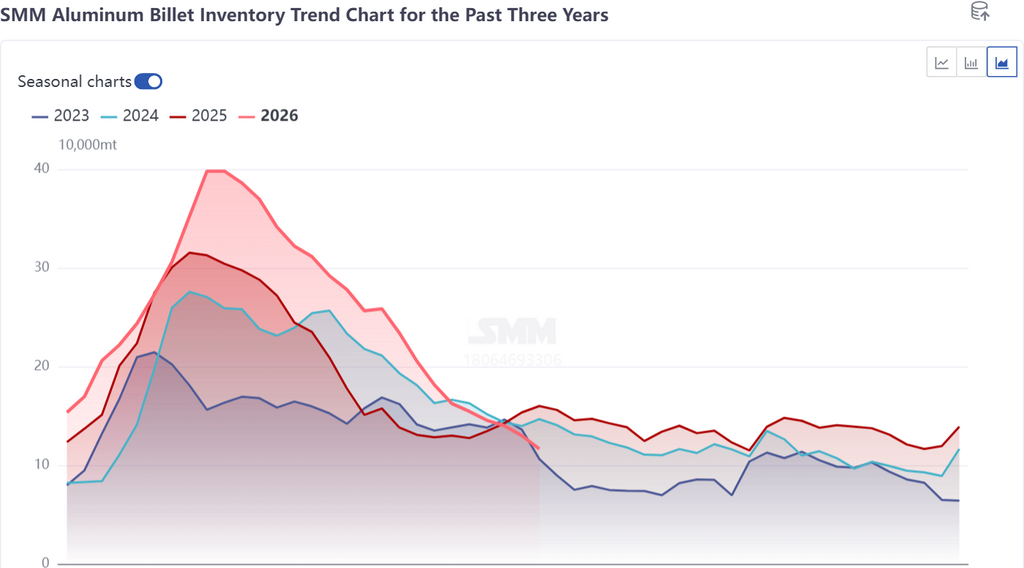

Social Inventory: Post-Chinese New Year Peak Hit a Multi-Year High, Destocking Speed Accelerated YoY

In H1 2026, China's aluminum billet social inventory generally followed a trajectory centered around the Chinese New Year holiday, first rising, then declining. During the holiday, downstream enterprises shut down en masse while billet plants maintained a certain level of production, causing shipments to continuously arrive at consumption areas but lacking momentum for off-take conversion. Social inventory rapidly climbed to a peak of approximately 398,000 mt, a near five-year high and significantly above levels seen in the same period of the previous two years. On one hand, many downstream enterprises showed signs of early market withdrawal as early as January, with spot trade sentiment cooling rapidly. On the other hand, the supply side maintained relatively high operating rates during the holiday, and the resulting supply-demand pace mismatch significantly amplified the extent of the inventory buildup.

After the holiday, as downstream operations resumed and falling aluminum prices spurred dip-buying sentiment, combined with factors such as a YoY production decline and reduced warehouse inflows to public warehouses, social inventory entered a rapid destocking channel. A turning point gradually formed in March, and destocking accelerated in April. By early June, it had fallen to around 160,000 mt, and by early July it further decreased to about 120,000 mt, landing at a low for the same period over the past three years. In terms of destocking magnitude, social inventory decreased by over 66% from its peak to the end of June in H1, significantly outperforming the same periods in 2025 (approximately 52%) and 2024 (approximately 47%). The improved destocking efficiency reflected the dual impact of supply-side contraction and marginal demand-side improvement.

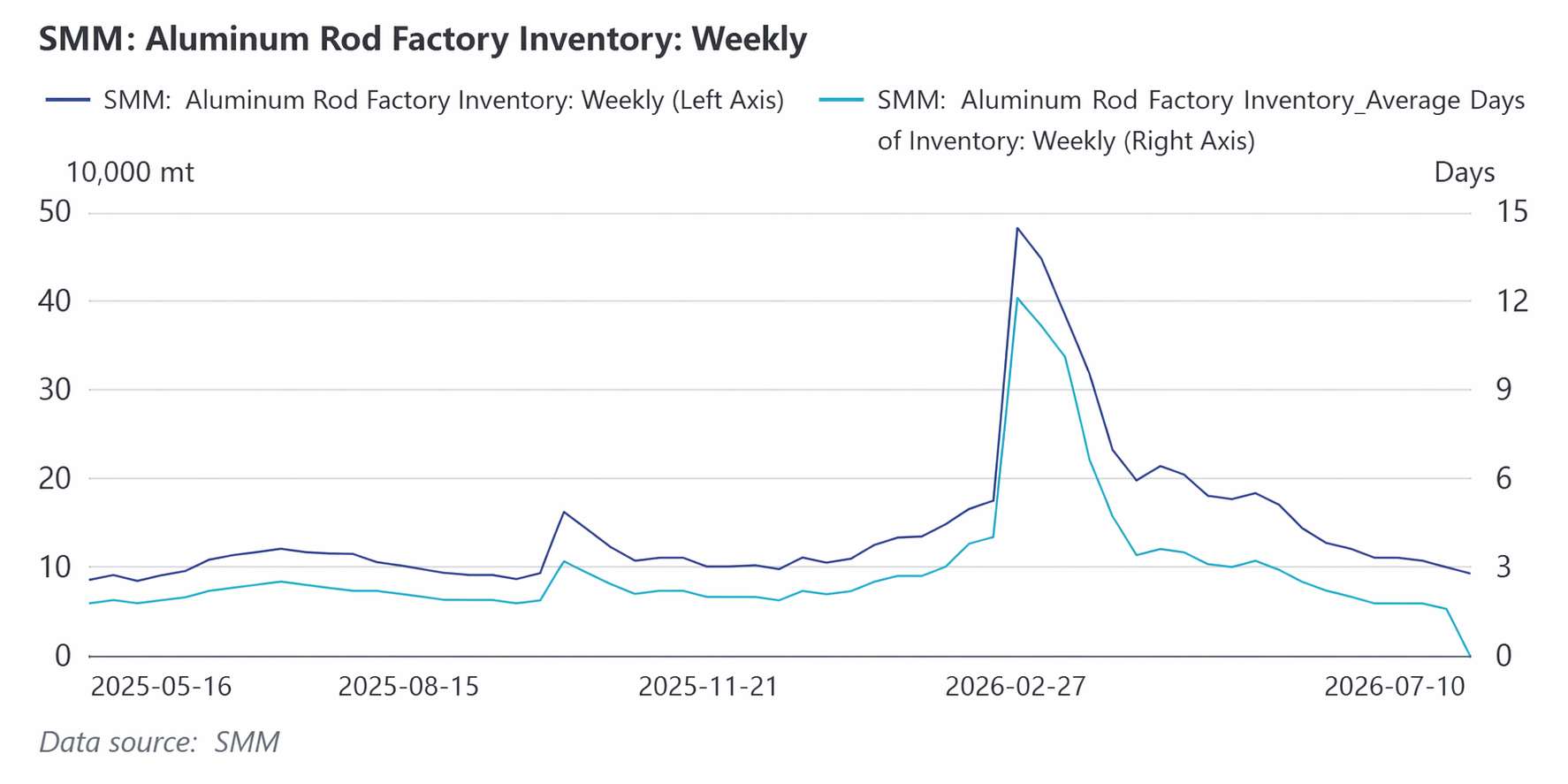

In-Factory Inventory: Peak Lower Than Previous Two Years, Destocking More Thorough

The fluctuation trajectory of in-factory inventory was similar to that of social inventory, also driven by the Chinese New Year holiday to first rise then fall. This year, the peak in-factory inventory was more contained compared to previous years. The main reasons were twofold: first, aluminum billet production momentum during the holiday was lower than the same period last year, with the proportion of cuts and shutdowns exceeding that of H1 2025; second, against a backdrop of high and fluctuating aluminum prices, producers were intent on accelerating sales to realize cash promptly, leading to a reduction in some regular stockpile volumes.

Looking at post-holiday destocking performance, in-factory inventory fell from its peak to around 100,000 mt by the end of June, a decrease of over 80%. This destocking magnitude also surpassed levels seen in the same period of the previous two years. By the end of June, in-factory inventory had largely returned to the levels seen at the start of the year, reflecting producers' strong willingness to sell and improved inventory turnover efficiency under a high processing fee environment. It is noteworthy that structural shortages of large and small billet specifications occurred during some parts of Q2, especially tight supply of small billets, which further accelerated the destocking of in-factory inventory.

Inventory Summary:The core characteristic of aluminum billet inventory trends in H1 was a high starting point coupled with rapid destocking. The high base after Chinese New Year once sparked market concerns, but supply-side contraction along with falling aluminum prices stimulated purchases, driving inventory destocking at a faster pace than in the previous two years. By end-June, both social inventory and in-factory inventory had fallen to relatively low levels for the same period in recent years, providing strong support for the processing fee rebound. However, whether the low inventory level can be sustained still depends on the strength of supply recovery in Q3 and actual demand performance in the off-season.

3. Processing Fees

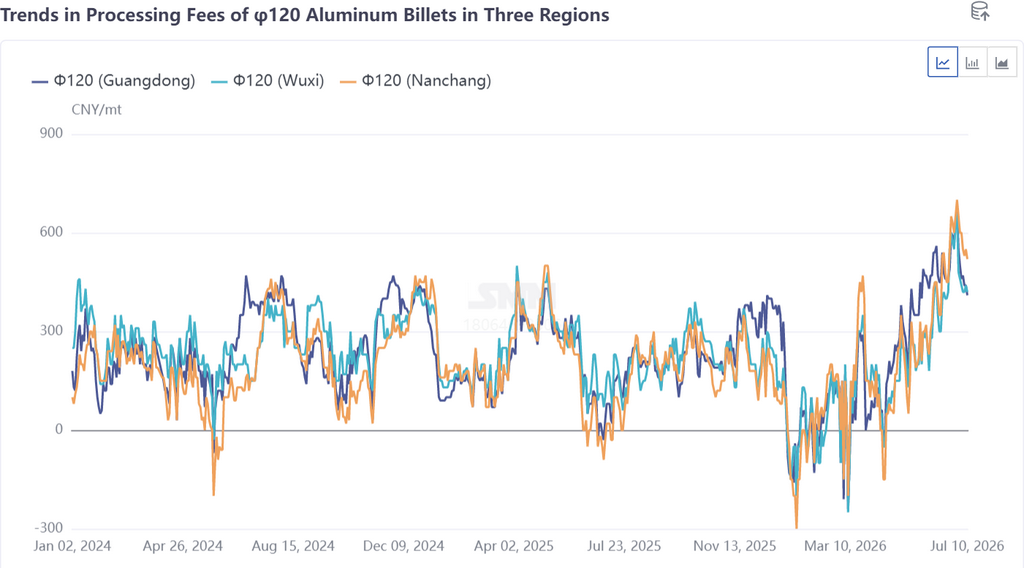

First Down Then Up, Fluctuation Range and Switching Frequency Both Surpass Prior Two Years

In H1 2026, China's 6063 aluminum billet processing fees exhibited a distinct "first down, then up" fluctuation trajectory, and whether in terms of the depth of declines, the height of rises, or the frequency of reversals, all exceeded the levels of the previous two years, leading to a marked increase in cautious sentiment among market participants.

Q1: Deep Discounts, the Darkest Hour for the Industry.In January, trading sentiment for aluminum billets gradually weakened, and processing fees experienced a "flash crash." In the three regions (Foshan, Wuxi, Nanchang), processing fees for φ120 aluminum billets largely plunged into negative territory, and the discount continued to widen driven by competitive pricing. By mid-March, when aluminum prices corrected, processing fees began to show signs of rising, but constrained by pressure from aluminum prices and weaker-than-expected consumption, they fell back again after a brief adjustment. For most of Q1, processing fees for mainstream 6063 construction billets remained below the cost line, leaving enterprises on the verge of losses with severe financial pressure.

Q2: Fluctuating Higher, Processing Fees Rebound Strongly.Late April became a critical turning point. Taking South China as an example, processing fees for φ120 aluminum billets in Guangdong, after hitting a Q2 low of -40 yuan/mt on April 16, surged rapidly to register a year-to-date high of 490 yuan/mt on May 28, accumulating a gain of more than 530 yuan/mt, with South China acting as the bellwether of this rebound. Subsequently, accelerating aluminum price declines in June pushed processing fees further to near three-year highs, with all three regions breaking through the 600 yuan/mt mark. Some specifications experienced structural shortages, and quotes for small billets rose amid tight supply.

The core drivers of this processing fee rebound can be summarized as three reinforcing factors:

First, the decline in aluminum prices and the Shanghai-Guangdong price spread. Since mid-to-late April, spot aluminum prices in the three major consumption regions fell sharply by more than 2,000 yuan/mt, which helped improve downstream purchasing sentiment. Meanwhile, the price spread between east and south China stayed high; as of end-May, the Shanghai-Guangdong price spread still reached as high as 150 yuan/mt, and the unwillingness of northern supply to flow to south China for sales created an imbalance in regional cargo flows, with the supply gap in south China being particularly prominent.

Second, supply-side disruptions. The push to standardize China’s aluminum capacity led to an undersupply of liquid aluminum in south-west China, forcing some billet plants to cut production despite high processing fees. At the same time, weak processing fees in Q1 squeezed enterprise profitability, and billet plants in some regions brought forward marginal production cuts such as production line maintenance, equipment upkeep, product switchovers, and raw material reductions. As of late May, some enterprises were still executing short-term production suspension and maintenance plans. Environmental protection checks in Baise, Guangxi further compressed the supply of liquid aluminum raw material for nearby billet plants. Multiple supply-side disruptions provided a direct thrust for processing fees to rise.

Third, mild demand-side recovery. After May, the operating rate of China’s aluminum extrusion industry rebounded to around 57.6%, continuing a mild recovery on a MoM basis. Construction extrusion, some enterprises organized production based on large-scale engineering project orders in hand, coupled with rising temperatures in the north driving a release of end-use demand for home renovation and door and window replacement. Industrial extrusion, a periodical weakening in aluminum prices spurred downstream purchasing willingness, and increased delivery orders for PV frame enterprises in early June drove up production schedules. The marginal improvement on the demand side provided fundamental support for the processing fee rebound.

By region, the price spread for processing fees in the Foshan area was particularly prominent among the three regions, with the core momentum for its periodical surge being the pullback in aluminum prices and a quantitative reduction in regional supply. In the Nanchang area, processing fees rose significantly in May-June, as reduced arrivals of north-west sourced goods due to tight shipping capacity and rising freight costs resulted in low local social inventories that provided support. The Wuxi area followed the upward trend, with small billet quotations rising noticeably driven by tight supply, and some specifications of large billets also experiencing periodical shortages. But in terms of semi-annual average prices, although processing fees were pulled up in Q2 and were elevated on a YoY basis, dragged down by deep discounts in Q1, the semi-annual average prices in the three regions all fell below 200 yuan/mt, remaining significantly lower than the same period in 2025.

Costs and Profitability: YoY cost increase narrowed profitability space

Aluminum prices fluctuated at highs overall in H1, rising noticeably compared to the same period last year, and aluminum billet production costs rose accordingly. Although the absolute price of aluminum billets increased, the core variable for enterprise profitability—processing fees—was weighed down by widespread deep discounts in Q1, causing the semi-annual average price to be lower than the same period last year and significantly narrowing enterprise profitability space on a YoY basis. While the processing fee rebound in Q2 brought a periodical recovery in profits, considering concealed costs such as capital and transportation, the overall profitability level of the industry remained under pressure, and some enterprises were still in a loss-making state in H1. The wild swings in processing fees, from deep discounts to near three-year highs, caused enterprise profits to frequently switch between gains and losses, significantly increasing operational difficulty.

II. H2 2026 Outlook for the Primary Aluminum Billets Market

Looking ahead to H2, the primary aluminum billet market is expected to find a new equilibrium amidst ongoing adjustments in the supply-demand pattern. Supply-side, constrained by tightening liquid aluminum availability due to the standardization of aluminum capacity, substantial production increases will be limited; demand-side, despite pressure from the traditional off-season, there remain expectations for steady growth in industrial extrusion products and potential marginal contributions from exports. Processing fees have shown signs of weakening after fluctuating at highs, and their H2 trend will depend on the intensity of supply-demand contention and the direction of aluminum price fluctuations.

1. Supply-Demand Fundamentals

Supply-side: Tightening Liquid Aluminum Constrains Production Ramp-up, Limited New Capacity Additions

The core variable on the supply side in H2 will be the ongoing impact of aluminum capacity standardization on liquid aluminum supply. With notable achievements in capacity standardization in China and the increased procurement demand for liquid aluminum driven by improved profitability for certain processing products, domestic liquid aluminum supply is becoming increasingly tight, leaving limited room for substantial production increases in the aluminum billet market in Q3. Some enterprises that undertook maintenance or product switching due to weak processing fees in Q1 still face uncertainty in their recovery progress.

In terms of new projects, while a small number were initiated in H1, ramp-up to full production still requires time; a few new projects are planned for H2, but their actual progress warrants cautious observation. Whether some previously curtailed or idled enterprises can resume in H2 remains to be seen, as factors such as conversion to diversified product types, reduced liquid aluminum raw material supply, and funding pressures will continue to affect their production efficiency. According to SMM's annual balance sheet forecast, China's total primary aluminum billet production in 2026 is expected to be around 17.77 million mt , corresponding to roughly 9.40 million mt for H2, an increase from H1 but with the growth capped by liquid aluminum supply constraints and remaining mild. SMM expects the operating rate to steadily rise to around 58.1% in July, with the room for further production ramp-up in subsequent months depending on the actual release of liquid aluminum supply.

Demand-side: Weak Domestic Recovery as the Main Theme, Export Driving Force Weakening Marginally

The demand side will continue to face multiple challenges in H2. On the domestic front, the market is currently in the traditional off-season, with weak end-use demand. The weekly operating rate of aluminum extrusion continues to decline WoW, and the pace of domestic demand recovery remains slow. In construction extrusion, the real estate market recovery remains sluggish, and demand for building materials lacks a trend-driven upward momentum, with little prospect of substantial improvement in the near term. In industrial extrusion, although new energy sectors such as PV and batteries still provide resilience to demand for industrial billets, moderate processing profits do not necessarily translate into synchronous expansion in end-use consumption; whether warehouse withdrawals can be sustained still requires verification.

On the export front, the overseas aluminum supply deficit in June boosted orders for aluminum semis exports, effectively absorbing some liquid aluminum capacity; however, in July, with the narrowing of the price spread between Chinese and overseas markets, the export driving force may weaken marginally. Aluminum billet direct exports are still in the early stages of volume ramp-up and are unlikely to make a significant contribution at scale in the short term. Additionally, amid high processing fees, some downstream extrusion enterprises, under cost pressure, tend to directly purchase aluminum ingots for remelting, exerting some substitution pressure on aluminum billet demand.

Overall, the key focus areas for demand in H2 are: First, whether the steadiness of industrial extrusion orders can be sustained, particularly the boost from emerging sectors such as PV and NEVs on high-end industrial billets; second, whether the traditional September-October peak season will arrive as expected, providing a window of phased recovery for construction extrusions; and third, the elasticity of exports amid changes in the price spread between Chinese and overseas markets. Overall, demand in H2 is likely to continue a weak recovery trend, with a low probability of significant expansion.

H2 supply-demand balance summary: On the supply side, production increases are constrained by tight liquid aluminum availability, leaving limited room for growth. On the demand side, domestic demand is recovering weakly, and the driving force for exports is weakening marginally. Both sellers and buyers face certain constraints. Under the dual-weak supply-demand pattern, the market may remain in a tight balance. Phased supply-demand mismatches may still occur, but the probability of a significant imbalance has decreased compared to H1.

2. Processing fees

After fluctuating at highs, processing fees are gradually coming under pressure and may move lower amid consolidation.

The currently high processing fees are already showing signs of softening and trending down. The market has always struggled to accept the attempts to hold prices firm and push processing fees higher. Downstream acceptance of high processing fees is limited, and some extrusion enterprises have already switched to purchasing aluminum ingots for remelting as a substitute, creating a natural ceiling for aluminum billet processing fees.

From the perspective of supporting factors, the constraint from tight liquid aluminum supply on the supply side persists. The situation of passive production cuts at some billet plants in south-west China is unlikely to see fundamental improvement in the short term. The tight supply pattern still provides some floor support for processing fees. Meanwhile, both social inventory and in-factory inventory are at relatively low levels for the same period in recent years. In a low-inventory environment, suppliers still have some ability to hold prices firm.

From the perspective of suppressing factors, in H2, during the traditional off-season, domestic demand will be weak, extrusion operating rates will decline MoM, and end-user purchasing strength will be limited. Export momentum will weaken marginally as the price spread between Chinese and overseas markets narrows. Stimulated by high processing fees, aluminum billet enterprises are highly enthusiastic about production; once liquid aluminum supply eases, the release of output will exacerbate the supply-demand imbalance, putting downward pressure on processing fees. Furthermore, processing fee competition is intensifying, with the industry’s cut-throat competition deepening. Low-price volume-selling has become the norm, and purchasing generally follows the market, procuring at prevailing prices, further weakening the ability of processing fees to resist declines.

Overall, domestic aluminum billet processing fees in H2 have very limited upside potential for a further significant surge. The center is expected to gradually move lower amid consolidation, but driven by aluminum price volatility, processing fees will still face multiple uncertain factors. Adjustments on the supply-demand side are equally unignorable: if the tightening of liquid aluminum supply continues to deepen, processing fees may regain upside momentum amid periodic supply-demand mismatches; conversely, if liquid aluminum supply recovers and off-season demand weakens further, the downward slope of processing fees could steepen.

It is worth noting that the negative correlation between the pace of processing fee fluctuations and aluminum price trends was particularly pronounced in H1—declining aluminum prices often opened up upside room for processing fees, and vice versa. This logic is expected to persist in H2, with the direction of aluminum prices serving as a leading indicator for processing fee trends. Additionally, close attention must be paid to the progress of policies on aluminum capacity standardization, the actual pace of increase in China’s proportion of liquid aluminum, and the real strength of the “September-October peak season” consumption period. Changes in these factors will jointly determine the central tendency and fluctuation range of processing fees in H2.

H2 processing fee outlook summary: Processing fees at current high levels have already shown signs of weakening, and upside room in H2 will be limited; they are expected to gradually move lower amid consolidation. However, factors such as tightening liquid aluminum supply and a low-inventory environment will still provide periodic support, meaning the downward path of processing fees is unlikely to be a straight line, and the uncertainties amid fluctuations need to be treated with caution. Aluminum price trends, supply-demand adjustments, and policy progress will collectively shape the trajectory of processing fees. Industry participants still need to maintain confidence and should not be overly pessimistic.

Data source: SMM

![Humanoid Robot and High-Efficiency Motor Demand Expectations Catalyze, Motor Sector Strengthens, Jiangxi Special Electric Motor Hits Daily Limit [SMM Quick News]](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)