SMM July 2 news:

Metal markets:

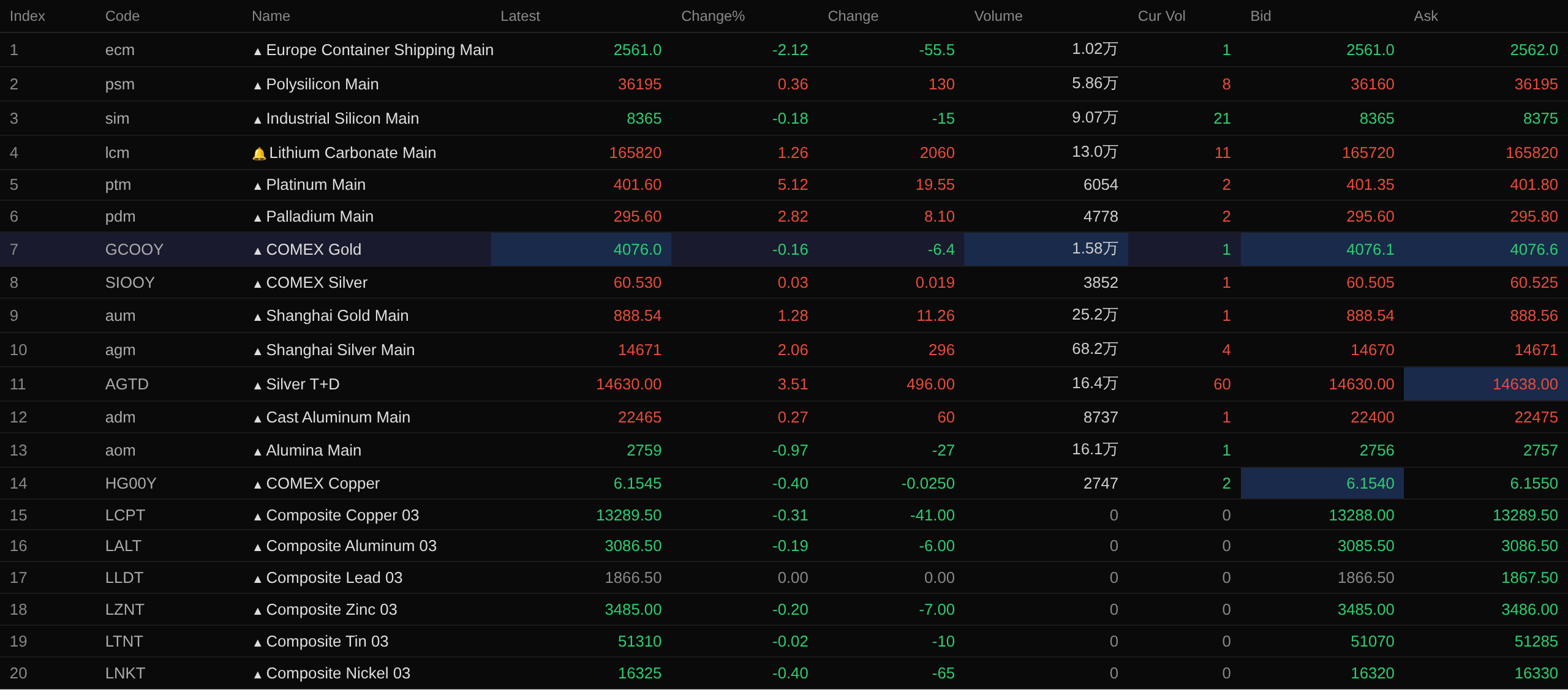

As of midday close, base metals on the domestic market mostly fell. SHFE copper and SHFE aluminum each fell within 0.2%. SHFE lead fell 0.72%. SHFE zinc fell 1.04%. SHFE tin rose 0.15%. SHFE nickel fell 0.41%.

In addition, the most-traded cast aluminum futures fell 0.97%, while the most-traded alumina futures rose 0.21%. Lithium carbonate most-traded futures extended gains from the previous three trading days, rising another 1.26%. Silicon metal most-traded futures fell 0.18%. Polysilicon most-traded futures rose 0.36%.

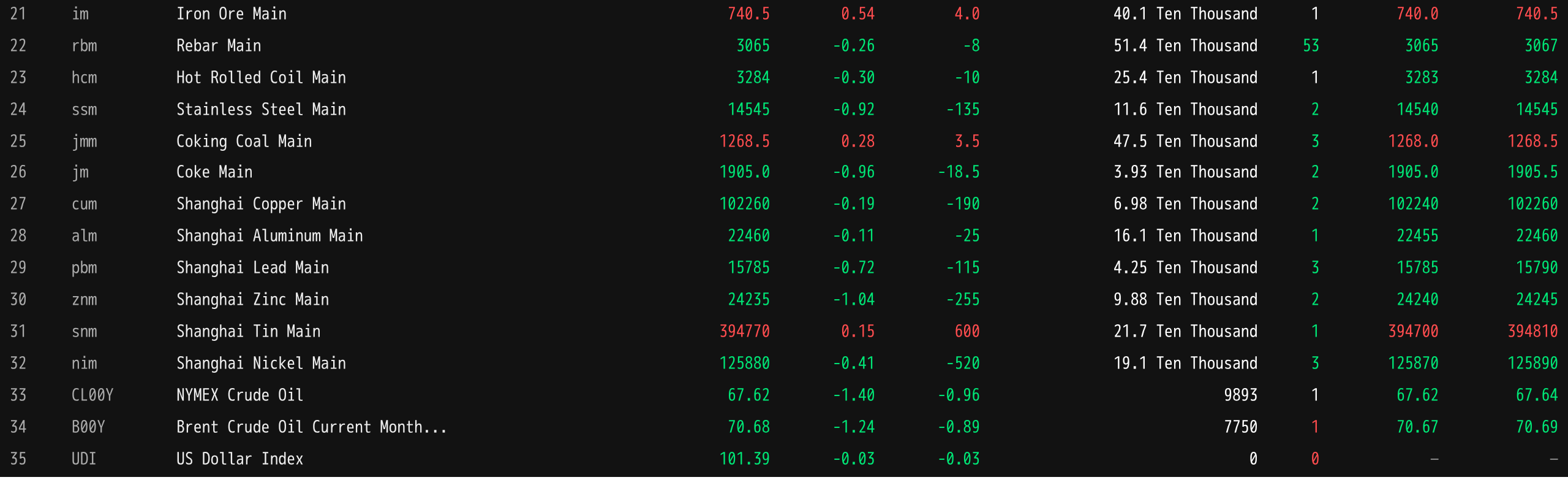

Ferrous metals mostly fell. Iron ore rose 0.54%. HRC and rebar fell within 0.5% each, and stainless steel fell 0.92%. Coking coal and coke: the most-traded coking coal contract rose 0.28%, and the most-traded coke contract fell 0.96%.

In overseas base metal markets, as of 11:39 am, LME metals nearly all fell. LME copper fell 0.31%, LME aluminum fell 0.19%, LME lead was flat at $1,866.5/mt. LME zinc fell 0.2%, LME tin edged lower, and LME nickel fell 0.4%.

In precious metals, as of 11:39 am, COMEX gold fell 0.16% and COMEX silver rose 0.03%. In domestic precious metals: SHFE gold rose 1.28%; the most-traded SHFE silver contract rose 2.06%.

In addition, as of midday close, the most-traded platinum futures rose 5.12%, and the most-traded palladium futures rose 2.82%.

As of midday close, the most-traded European route container freight futures fell 2.12% to 2,561 points.

As of 11:39 am on July 2, midday futures quotes for select contracts:

Spot and Fundamentals

Aluminum: In the morning session, the trading center of the SHFE aluminum 2606 contract was higher than that of the same period on the previous trading day. Warrant cargoes continued to flow out of the market, and circulating spot supply was generally ample. Downstream only saw sporadic restocking, and with bearish sentiment spreading in the futures market, end-user purchase willingness was overall weak. Mainstream transactions were at parity to a premium of 20 yuan/mt over the SHFE aluminum 2607 contract...

Macro Front

Domestic:

[The mandatory national standard "Safety Requirements for Combined Driving Assistance System of Intelligent and Connected Vehicles" was officially released] On June 27, the mandatory national standard "Safety Requirements for Combined Driving Assistance System of Intelligent and Connected Vehicles" (GB 47955—2026), organized, formulated and centralized by the Ministry of Industry and Information Technology, was approved and released by the State Administration for Market Regulation and the National Standardization Administration, and is scheduled to be officially implemented on January 1, 2027. 《Safety Requirements for Intelligent Connected Vehicles—Combined Driver Assistance Systems, grounded in the needs of industry development and regulatory oversight in China, takes into account technical feasibility, product compatibility, and practical implementability, and establishes a safety indicator framework with clear requirements, comprehensive dimensions, and alignment with national conditions. First, it fully considers different product forms and technical routes, proposing applicable safety requirements for three types of combined driver assistance system products: basic single-lane, basic multi-lane, and navigation driver assistance. Second, based on China’s road traffic characteristics, it sets out baseline requirements to ensure the safe operation of combined driver assistance systems across dimensions such as functional requirements, data recording, and vehicle manufacturer safety assurance. Third, recognizing the core positioning of these systems as "assistance" in driving, it puts forward requirements for user usage and operation in areas such as human-machine interaction, usage instructions, and user training, providing a foundational guarantee for proper coordination between users and systems. Fourth, in line with the practical needs of China’s industry management, it builds a multi-tiered evaluation approach encompassing field tests, road tests, and document inspections to comprehensively assess system safety capabilities.

The PBOC conducted ¥288.5 billion in 7-day reverse repos today, with an operation rate of 1.4%, unchanged from the previous level. Today, ¥370.5 billion in reverse repos matured.

US Dollar:

As of 11:39, the US dollar index fell 0.03% to 101.39. Fed Chairman Warsh said Wednesday that inflation expectations and inflation risks have both declined in recent weeks, while reiterating the Fed’s commitment to bringing inflation down to the 2% target. "In the first few weeks of this period, inflation expectations have pulled back, and inflation risks have also eased," Warsh said. "If households, the business community, or financial markets think the Fed is comfortable with inflation above 2%—well, they are likely to be disappointed: we will ensure price stability in the US."

Fed Chairman Warsh sidestepped questions on whether the Fed might raise rates at its July meeting. "I hope that when we meet in four weeks, we can have a robust 'internal family debate,'" he said. "When we close the doors and sit down together, we will have a vigorous debate. But beyond that, I have no further information to share." Warsh made the remarks at the ECB’s annual policy conference in Sintra, Portugal; this was his first public appearance since his inaugural press conference at the Fed last month. Since then, investors have begun to anticipate more rate hikes from the Fed, but the market currently sees the likelihood of a first hike this month at less than 50%.

According to CME "Fed Watch": The probability that the US Fed will keep rates unchanged in July is 71.7%, and the probability of a cumulative 25-basis-point rate hike is 28.3%. The probability that the Fed will keep rates unchanged by September is 36.1%, the probability of a cumulative 25-basis-point hike is 49.8%, and the probability of a cumulative 50-basis-point hike is 14.1%. (Jin10 Data APP)

On the data front: US manufacturing expanded for a sixth consecutive month in June, with the war-driven surge in input costs easing. Printing, electrical equipment, and textiles led the gains, while paper products, furniture, and wood products contracted. Market attention has now shifted to Thursday's US employment report. Julien Lafargue, chief market strategist at Barclays Private Bank and Wealth Management, noted that with Warsh prioritizing inflation, the June non-farm payrolls data is "unlikely to change rate expectations on its own." He added that hiring related to the FIFA World Cup is expected to distort the data. (Wall Street Insights)

Data front:

Today will see the release of the US June unemployment rate, US June seasonally adjusted non-farm payrolls, US initial jobless claims for the week ended June 27, US June average hourly earnings year-over-year, US June average hourly earnings month-over-month, US May factory orders month-over-month, Switzerland June CPI month-over-month, eurozone May unemployment rate, among other data. Additionally, watch for: the Ministry of Commerce's regular press conference for the first week of July, and 2027 FOMC voting member and San Francisco Fed President Daly’s participation in a conference on the Spanish economy.

Due to the US Independence Day holiday (July 3), the US June non-farm payrolls data will be released earlier on July 2 (Thursday) at 20:30 Beijing time. US stock markets will be closed on July 3 (Friday). Trading in precious metals, energy, foreign exchange, US Treasury, and equity index futures contracts on CME will end early at 01:00 Beijing time on July 4. Trading in Brent crude oil futures contracts on ICE will end early at 01:30 Beijing time on July 4. Investors are advised to take note. (Jin10 Data APP)

Crude oil:

As of 11:39, oil prices in both markets extended their decline from the previous two trading sessions, with WTI down 1.4% and Brent down 1.24%.

International crude oil prices pulled back due to progress in Middle East peace talks. (Wall Street Insights)

As supply through the Strait of Hormuz rebounded, OCBC Group Research lowered its quarterly crude oil forecasts through the end of Q2 2027. Two OCBC strategists noted in a research report: "With the signing of a memorandum of understanding between the US and Iran, shipping and crude oil supply through the Strait of Hormuz have rebounded."They also said, "Market expectations that crude oil supply would return to normal quickly pushed oil prices back to pre-conflict levels, rekindling oversupply rhetoric." OCBC cut its Brent crude price forecast for Q3 2026 from $85 to $75 per barrel, Q4 2026 from $80 to $75, Q1 2027 from $75 to $73, and Q2 2027 from $75 to $71. (Jin10 Data APP)

Increasing energy flows through the Strait of Hormuz prompted UBS to cut its 2026-2027 oil price forecast. UBS now expects Brent crude to average $84 per barrel this year, down $9 from its previous forecast. The bank also cut its 2027 oil price forecast from $85 to $75 per barrel. UBS said, "The decline in geopolitical risk and the rapid rebound in supply led to a larger price drop than we had expected." The bank expects oil prices to rebound slightly to $80 per barrel in H2 this year as floating storage in the Gulf region normalizes and demand recovers. UBS also believes risk premiums will be higher because the path to normalization may remain bumpy. UBS said, "The need to replenish inventories should continue to support prices through the end of 2027, but the required magnitude of stock rebuilding is smaller than the 1 billion barrels we previously expected." (Jin10 Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

►

►

![Inventory Continuous Destocking Pushes Shanghai Spot Copper Premium Center Higher [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/hsjMg20251217171712.jpg)

![Walsh Reaffirms Inflation Baseline, SHFE Tin Contracts Maintain Fluctuating Trend [SMM Tin Midday Commentary]](https://imgqn.smm.cn/usercenter/QgNfJ20251217171752.jpg)

![Guangdong Zinc: Zinc Prices Continue to Consolidate at Highs, Downstream Purchasing Enthusiasm Insufficient [SMM Midday Review]](https://imgqn.smm.cn/usercenter/kdRPs20251217171754.jpg)