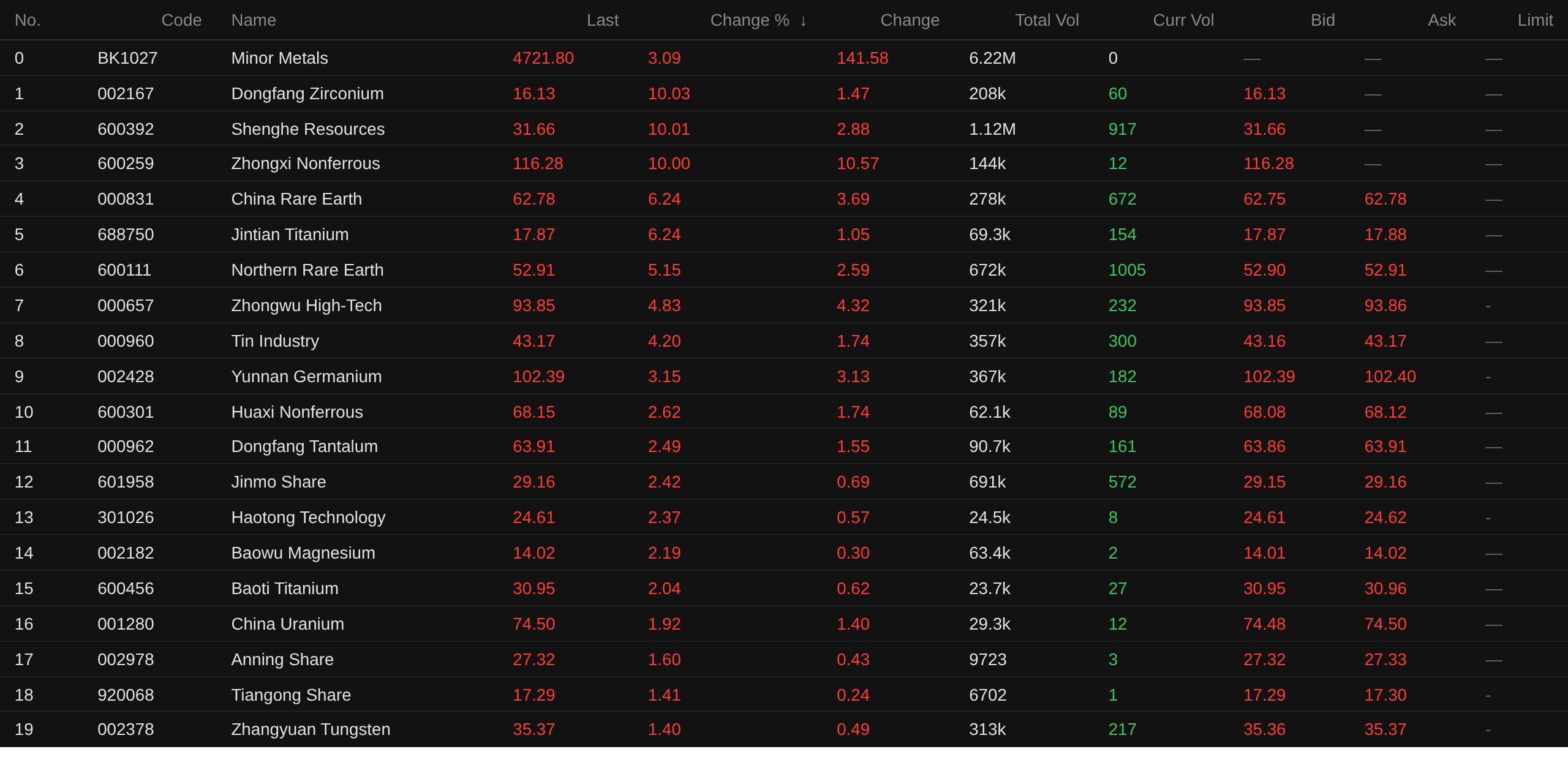

SMM, June 18:

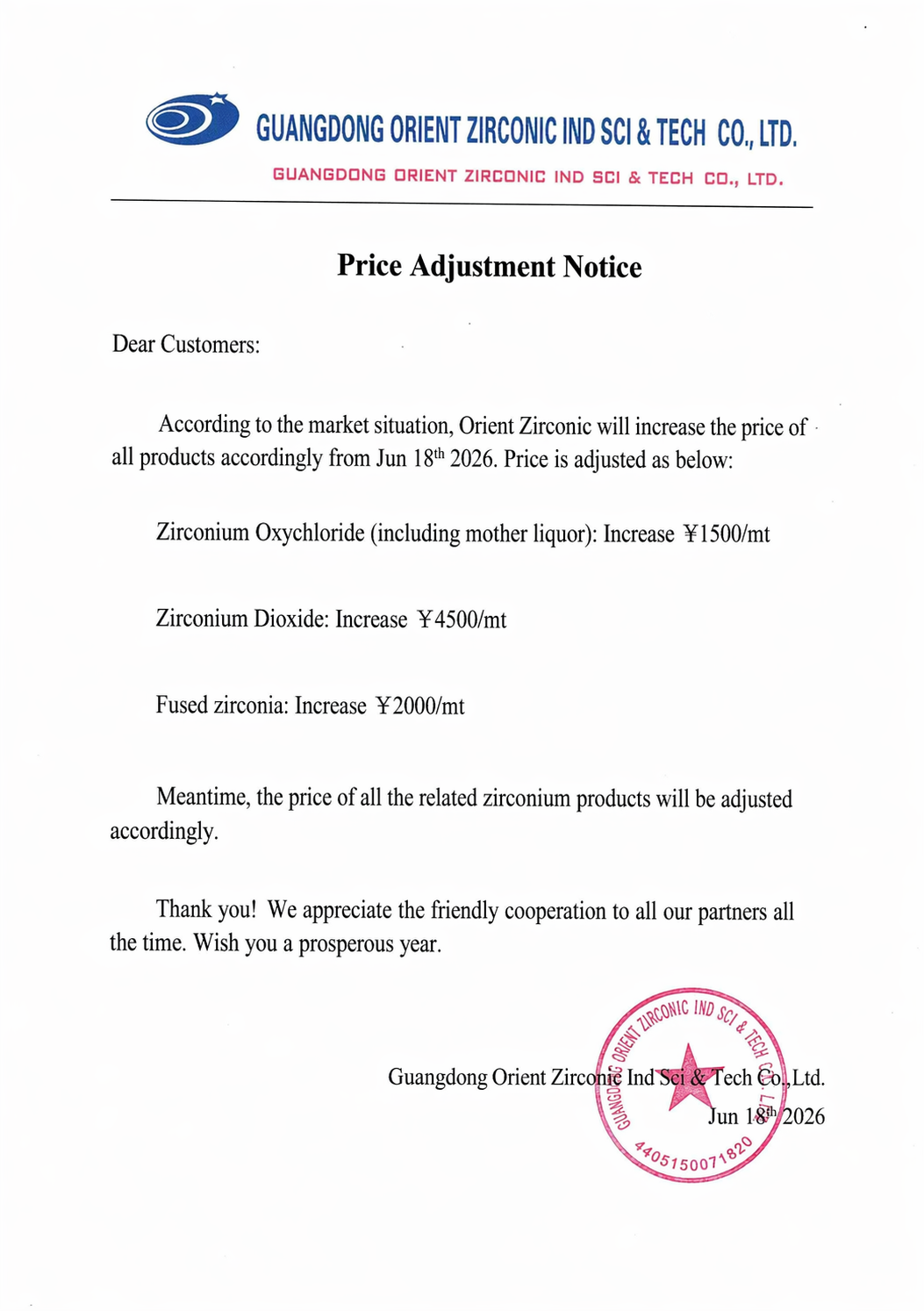

The Regulations for the Implementation of the Mineral Resources Law of the People's Republic of China, which took effect on June 15, listed 36 types of minerals, including rare earths, tungsten, lithium, cobalt, gallium, and germanium, as national-level strategic minerals, subjecting them to full-chain, high-intensity control. The prices of Pr-Nd oxide, dysprosium oxide, and terbium oxide saw their third consecutive daily increase on June 17; Orient Zirconium issued a price adjustment notice, raising the prices of its related zirconium products effective June 18, 2026; and the favor of some market funds all contributed to the opening strength of the minor metal sector. As of around 9:57 on June 18, the minor metal industry sector rose by 3.09%. In terms of individual stocks: Orient Zirconium, Shenghe Resources, and Zhongxi Nonferrous hit the daily limit; China Rare Earth, Jintian Titanium, China Northern Rare Earth, China Tungsten High-Tech, Tin Industry Co., and Yunnan Germanium led the gains.

Market News

Orient Zirconium raised the prices of its related zirconium products effective June 18, 2026

On June 18, Orient Zirconium issued a product price adjustment notice. The notice indicated that based on current market conditions, Orient Zirconium decided to raise the prices of its related zirconium products starting from June 18, 2026, with the price adjustments as follows: zirconium oxychloride products (including mother liquor materials) increased by 1,500 yuan/mt; zirconium dioxide products increased by 4,500 yuan/mt; fused zirconium products increased by 2,000 yuan/mt; at the same time, the prices of other zirconium series products from Orient Zirconium will be adjusted accordingly.

[Aidite: The company has already laid out a powder substitute plan and fully implemented it; the new material can replace the original imported powder] On June 17, Aidite stated on an interactive platform while answering investor questions that the company had received a notice from Japan's Tosoh regarding the suspension of zirconia powder supply. To ensure the stability of its own supply, the company had already laid out a powder substitute plan and fully implemented it; the new material can replace the original imported powder, and the entire new product line has passed rigorous customer verification. Currently, several core major clients have completed the switch and signed long-term orders at the recent dealer conference. The company will actively take a series of measures to avoid any adverse impact from the Japanese powder supply disruption. In the future, the company will seize the window of opportunity for high-quality material breakthroughs and, leveraging its technical and delivery advantages, continue to expand its market share.

Spot Market

Zirconium

According to the SMM price assessment, on June 18, the price of zirconium oxychloride (Zr(Hf)O2≥36%) was quoted at 17,500-18,000 yuan/mt, with an average of 17,750 yuan/mt, up 5.97% from the previous trading day.

The zirconium industry chain had long been under pressure, with sluggish traditional demand from ceramics and high industry inventories. Zircon sand and zirconium oxide prices persistently hovered at lows, trading was sluggish, and the market was at the bottom of the cycle. Since entering Q2 this year, driven by export controls on zirconium products to Japan, price hikes by overseas zirconium ore producers, and demand expectations for solid-state batteries, zirconium raw material prices stopped falling and stabilized, inventories destocked, and the industry moved out of the bottom range, embarking on a volatile recovery trend. Upstream zircon sand imports have tightened, overseas miners continue to raise prices, and cost support has been strengthening. Dongfang Zirconium Industry completed a round of price hikes in April and raised zirconium product prices again on June 18. For the zirconium market outlook, supported by tightening raw material supply, zirconium prices will hold up well in the short term. Going forward, attention should be paid to changes in raw material supply and downstream demand.

Rare Earth

In the rare earth market: Rare earth oxide prices were relatively stable overall, but downstream purchasing activity has decreased as the holiday approaches. Pr-Nd oxide and dysprosium oxide ended their three-day winning streak and both pulled back slightly on June 18, while terbium oxide prices held steady on June 18 after a previous three-day rise.

Expectations for production cuts in the scrap recycling sector and news-driven factors previously drove Pr-Nd prices, dysprosium oxide, and terbium oxide higher. However, after the afternoon session on June 17, shipments of Pr-Nd oxide from traders increased slightly, and the center of the actual trading range shifted lower. For medium-heavy rare earths, oxide suppliers held firm offer prices, but actual buying from metal enterprises was limited, and downstream magnetic material enterprises showed limited acceptance of high metal prices. Affected by the stalemate in market trading, rare earth prices are expected to move sideways in the short term.

Tin

Additionally, in the tin market: On June 18, the average price of SMM 1# tin fell 0.93% from the previous trading day. Driven by the US Fed keeping rates unchanged but signaling a hawkish bias, with half of policymakers expecting rate hikes this year, nonferrous metals fell overall and tin prices also pulled back.

Currently, on the fundamental side: (1) Supply side: In June, most smelters focused on maintaining stable production. (2) Demand side: Downstream purchases were cautious, buying according to orders. Spot market: Overall trading sentiment in the spot market was light. Although tin prices have pulled back, they remain at relatively high levels and the holiday is approaching. Additionally, as the electronics industry enters its traditional off-season, downstream enterprises such as solder makers are only purchasing on a "buy on dips for essential needs" basis.

Institutional Views

Guojin Securities’ research report on June 14 showed: Rare Earth: Dysprosium oxide may benefit from the boost by MLCC, with a significant rebound trend from price lows. From the start of the year, the price center has continued to rise. We believe this is likely related to supply-side documents released in 2024-2025, with ongoing supply-side reform in the industry. Exports fell 1% YoY for full-year 2025, while exports from early 2026 to date have increased significantly, indicating strong restocking demand outside China. The rare earth sector will continue to see dual improvements in valuation and performance, and 2026 is also a key year for resolving industry competition among key targets. On the resource side, attention is recommended for China Rare Earth (medium-heavy rare earth leader, biggest beneficiary of supply-side reform), Zhongxi Nonferrous (undervalued, high-growth South China rare earth leader), and China Northern Rare Earth (light rare earth leader, with significant cost advantages); other related targets include Bao Gang United Steel, JL MAG Rare-Earth, etc. Tin: It believes that invisible inventory of tin ingots is gradually drying up, so tin prices are expected to strengthen under the backfill of macro liquidity or spillover from tech markets. The supply-demand pattern for tin will improve in the long term. Tungsten: This period, tungsten prices continued their rebound trend. It believes that against the backdrop of increased strategic stockpiling outside China, tungsten may have higher priority; tungsten's supply-demand fundamentals have seen strong resonance. Molybdenum: The destocking of imported ore has been significant, and domestic molybdenum prices have stabilized and rebounded. Steel procurement volume remains robust, destocking along the industry chain is progressing, and the deadlock of molybdenum prices with "volume but no price" is gradually being broken, with the upward channel becoming clearer. Molybdenum is also a military metal, with persistently low inventory, and increased defense spending outside China may further boost molybdenum prices.

Huafu Securities’ research report on June 14 showed: Other Minor Metals: Industry leaders' long-term contract performance was impressive, and market sentiment in tungsten clearly stabilized. The tungsten market overall has walked out of a mild recovery, with the previous consolidation at lows being reversed somewhat. Industry leaders' long-term contract transactions were impressive, serving as a key driver for the upward movement in futures, and overall market sentiment clearly stabilized. However, the spot and scattered cargo atmosphere remained mediocre, with no widespread price-following adjustments upstream or downstream, and the rebound pace was gentle, with the market overall in a stage of steady recovery.

Open Source Securities' 2026 mid-year investment strategy for the metals industry showed: Copper: Supply side, most miners outside China still face declining grades and recovery rates, and disruptive factors persist (Ivanhoe’s KK copper mine, Codelco’s El Teniente copper mine). While Chinese enterprises are increasing output, the overall increase is limited. Under an optimistic scenario, global supply growth may be below 2% in 2026-2027. Demand side, H1 electricity demand in China and the US maintained high growth rates, which may contribute marginal increments to copper demand. Open Source Securities believes that the supply-demand structure contradiction for copper will further highlight in 2026, supporting the rise in copper price center. Lithium: On the supply side of the lithium industry, capital spending cuts and the gradual formation of supply discipline, coupled with frequent disruptions, have led to a marked decline in supply elasticity compared with the past. Meanwhile, sustained strong demand from the energy storage sector is improving the structure of lithium demand, while industry inventory pressure is easing marginally. Lithium prices are expected to see a phased recovery. Enterprises with advantages in resource security, low costs and integrated layout are likely to show stronger earnings recovery than the industry average. Lithium mines and lithium chemicals companies with high resource self-sufficiency and strong cost control deserve attention. Tungsten: As an advantaged strategic metal in China, tungsten mine supply is constrained by resource depletion, environmental protection and other factors. Together with the total mining volume control implemented by the state, tungsten mine production release is limited. On the demand side, emerging sectors are boosting tungsten demand, which is expected to support tungsten prices over the long term.

Recommended reading: