SMM Noticias del 15 de junio:

Mercado de metales:

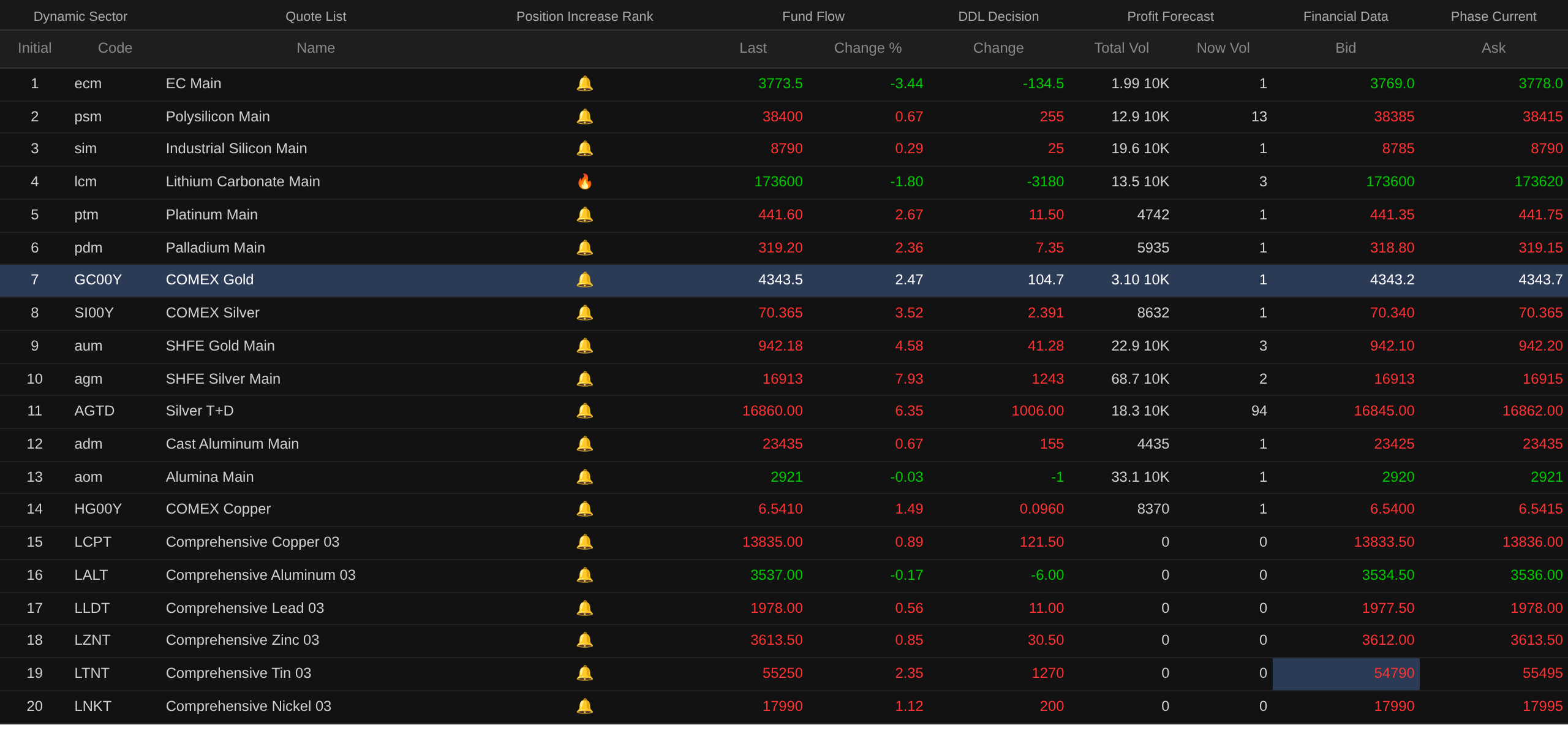

Al cierre de mediodía, los metales básicos nacionales subieron en todos los frentes. El cobre de la SHFE subió un 1,35%, el estaño de la SHFE subió un 4,35%. El níquel de la SHFE subió un 1,27%, el aluminio de la SHFE subió un 0,31%, el zinc de la SHFE subió un 2,37% y el plomo de la SHFE subió un 1,21%.

Además, el contrato de futuros de aluminio de fundición más negociado subió un 0,67%, mientras que el contrato de alúmina más negociado bajó ligeramente. El contrato de carbonato de litio más negociado cayó un 1,8%, el de silicio metálico subió un 0,29% y el de polisilicio subió un 0,67%.

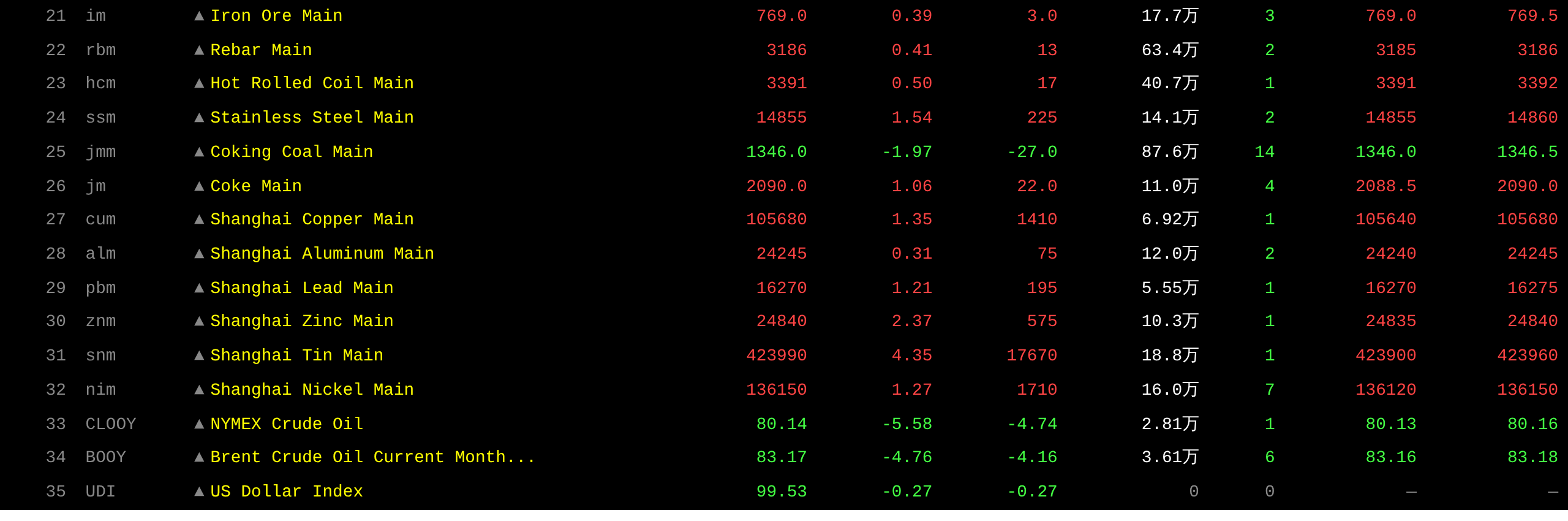

Los metales ferrosos subieron de forma generalizada, con el mineral de hierro un 0,39% al alza, el acero corrugado un 0,41%, la bobina laminada en caliente un 0,5% y el acero inoxidable un 1,54%. Carbón de coque y coque: El contrato de carbón de coque más negociado cayó un 1,97% y el de coque subió un 1,06%.

Metales básicos en el extranjero: A las 11:38, los metales de la LME casi todos subieron. El cobre de la LME subió un 0,89%, el aluminio de la LME cayó un 0,17%, el plomo de la LME subió un 0,56%, el zinc de la LME subió un 0,85%, el estaño de la LME subió un 2,35% y el níquel de la LME subió un 1,12%.

Metales preciosos: A las 11:38, el oro del COMEX subió un 2,47% y la plata del COMEX un 3,52%. Metales preciosos nacionales: El contrato de futuros de oro de la SHFE más negociado subió un 4,58% y el de plata de la SHFE subió un 7,93%.

Asimismo, al cierre de mediodía, el contrato de futuros de platino más negociado subió un 2,67% y el de paladio subió un 2,36%.

Al cierre de mediodía, el contrato de futuros de transporte marítimo de contenedores de la ruta europea más negociado cayó un 3,44% hasta los 3.773,5 puntos.

A las 11:38 del 15 de junio, algunas cotizaciones al mediodía de los futuros:

Mercado spot y fundamentos

Zinc: Hoy, los precios de transacción mayoristas del zinc #0 se concentraron en 24.650-24.885 yuanes/tm, las transacciones mayoristas de Shuangyan se situaron en 24.740-24.945 yuanes/tm y las del zinc #1 en 24.580-24.815 yuanes/tm. En las primeras operaciones, las cotizaciones del mercado respecto al precio promedio de SMM mostraron primas de 10-30 yuanes/tm, sin cotizaciones todavía contra el precio de futuros...

Frente macro

Nacional:

[NDRC y otros departamentos: Lanzan campaña trienal de transformación para el ahorro energético y la reducción de carbono en industrias clave] La Comisión Nacional de Desarrollo y Reforma (NDRC) y otros departamentos han decidido organizar una campaña trienal de transformación para el ahorro energético y la reducción de carbono en industrias clave, incluyendo acero, aluminio, cemento, vidrio plano, refinación de petróleo, etileno, amoníaco sintético, metanol y energía de carbón. Se mencionó que las industrias clave tienen un consumo energético y emisiones de dióxido de carbono de gran escala y alta intensidad, lo que las convierte en la máxima prioridad para mejorar la eficiencia energética, reducir el consumo de carbón y disminuir las emisiones de carbono. A partir de 2026, nueve industrias clave —acero, aluminio, cemento, vidrio plano, refinación de petróleo, etileno, amoníaco sintético, metanol y energía de carbón— serán el foco de una iniciativa trienal para implementar de manera integral las renovaciones de ahorro energético y reducción de carbono. Esto tiene como objetivo impulsar a las empresas a elevar sus niveles de eficiencia energética y de carbono tanto como sea posible, conduciendo a una mejora notable en el desarrollo verde y bajo en carbono de estas industrias. A partir de 2028, el alcance de la implementación se ampliará aún más según las circunstancias prácticas, con industrias adicionales que se avanzarán de manera escalonada. Todas las regiones podrán proceder de manera ordenada según sea necesario y las condiciones locales.

[El repo inverso del PBOC inyecta un neto de 206.500 millones de yuanes hoy] El Banco Popular de China (PBOC) realizó una operación de repo inverso a 7 días por valor de 425.000 millones de yuanes en el mercado abierto a una tasa de interés del 1,40%, sin cambios respecto al día anterior. Hoy vencieron 218.500 millones de yuanes en repos inversos.

Dólar estadounidense:

A las 11:38, el índice del dólar cayó un 0,27% hasta 99,53. La disminución de las tensiones en Oriente Medio llevó al mercado a reducir las apuestas sobre subidas de tipos de la Fed. Los swaps de tasas de interés mostraron que los operadores ahora ven una probabilidad aproximada del 60% de que la Fed suba los tipos en 25 puntos básicos antes de diciembre, por debajo del 80% del viernes pasado. (Jinshi Data APP)

Además, según la herramienta “FedWatch” de la CME: la probabilidad de que la Fed mantenga las tasas de interés estables en junio es del 98,5%, con un 1,5% de probabilidad de un recorte acumulado de 25 puntos básicos. La probabilidad de mantener las tasas estables hasta julio es del 91,3%, con un 7,4% de probabilidad de una subida acumulada de 25 puntos básicos y un 1,4% de probabilidad de un recorte acumulado de 25 puntos básicos. (Jinshi Data APP)

En el frente de datos: la confianza del consumidor estadounidense repuntó por primera vez en cuatro meses a principios de junio, ya que los menores precios de la gasolina ofrecieron cierto alivio a los estadounidenses que luchan contra una inflación galopante. Una encuesta publicada el viernes mostró que el índice preliminar de confianza del consumidor de la Universidad de Míchigan para junio subió a 48,9 desde el mínimo histórico de 44,8 de mayo. Los economistas esperaban una modesta recuperación hasta 46. Los consumidores anticipan que los precios subirán un 4,6% interanual en el próximo año, por debajo del 4,8% de mayo. También proyectaron que los costos subirían a una tasa anual promedio del 3,4% durante los próximos cinco a diez años, también por debajo del aumento esperado del mes anterior. Aunque los precios de la gasolina siguen siendo más altos que los niveles anteriores a la guerra de Ucrania, la caída de las últimas semanas ha reducido el pesimismo sobre las finanzas personales entre los estadounidenses. El informe mostró una mejora notable en el sentimiento entre los consumidores de menores ingresos, que suelen destinar una mayor parte de sus presupuestos a los costos de combustible. Sin embargo, en el contexto de la guerra de Irán y la consiguiente ola de inflación, el sentimiento económico general sigue en niveles históricamente deprimidos. La directora de la encuesta, Joanne Hsu, declaró: “Aunque ha habido cierto alivio, los precios de la gasolina siguen teniendo un impacto significativo en los consumidores. Como resultado, los niveles de precios actuales siguen siendo en gran medida inaceptables para los consumidores y han empañado su visión de la economía.” (Jin10 Data APP)

Datos:

Hoy se publicarán el índice de confianza del consumidor de Suiza de mayo, la balanza comercial desestacionalizada de la eurozona de abril, la producción industrial intermensual de la eurozona de abril, las ventas mayoristas intermensuales de Canadá de abril, el índice manufacturero Empire State de EE.UU. de junio, la producción industrial intermensual de EE.UU. de mayo, el índice del mercado de la vivienda NAHB de EE.UU. de junio y el consumo total de electricidad interanual de China de mayo (por determinar), entre otros datos. También se debe prestar atención a: el discurso de la presidenta del BCE, Christine Lagarde; la publicación por parte de la Administración Nacional de Energía de los datos de consumo total de electricidad alrededor del día 15 de cada mes; y la apertura de la cumbre del G7, que se extenderá hasta el 17 de junio.

Petróleo crudo:

A las 11:38, los precios del petróleo en ambos lados del Atlántico cayeron bruscamente, con el WTI un 5,58% abajo y el Brent un 4,76%. Se espera que se firme pronto un acuerdo de paz entre EE.UU. e Irán, aliviando las preocupaciones del mercado sobre el suministro de crudo y presionando los precios del petróleo a la baja.

Según la agencia Xinhua, el presidente de EE.UU., Trump, declaró en redes sociales el día 14 que con la firma del acuerdo entre EE.UU. e Irán el 19, el estrecho de Ormuz se reabrirá para operaciones de desminado. El viceministro de Exteriores de Irán también indicó que a partir de esta noche se anunciará un cese inmediato y permanente de las operaciones militares en múltiples frentes, incluido el Líbano.

Patrick DeHaan, jefe de análisis de petróleo de GasBuddy, dijo que el precio promedio nacional de la gasolina en EE.UU. cayó por debajo de los 4 dólares por galón el domingo por primera vez desde el 20 de abril. Espera que, en un escenario optimista, el precio promedio nacional podría caer por debajo de los 3,75 dólares por galón antes del 4 de julio, pero la temporada de huracanes podría ser una variable importante en la segunda mitad del verano. “Las próximas semanas son críticas: cualquier paso en falso importante podría afectar significativamente la trayectoria posterior del precio del petróleo.” (Wall Street CN)

Mercado spot a simple vista:

►

►

►

►

►

►

►

►

►

►

►

►

![El aluminio de la SHFE sube ligeramente y se mueve lateralmente; el rebote de la alúmina con volumen decreciente carece de fuerza [Comentario de SMM sobre el aluminio]](https://imgqn.smm.cn/usercenter/ceevU20251217171653.jpg)

![Los futuros se debilitan pero están limitados por la demanda débil, las primas luchan por subir [Análisis de mediodía del aluminio al contado de SMM]](https://imgqn.smm.cn/usercenter/RLjGN20251217171652.jpg)

![Los metales básicos suben en general, la plata en la SHFE se dispara más de un 3%, el carbonato de litio cae más de un 4%, el carbón coquizable, el coque y el mineral de hierro lideran el descenso [Comentario del mediodía de SMM]](https://imgqn.smm.cn/usercenter/fNuSg20251217171735.jpg)