SMM June 4 News:

Metals market:

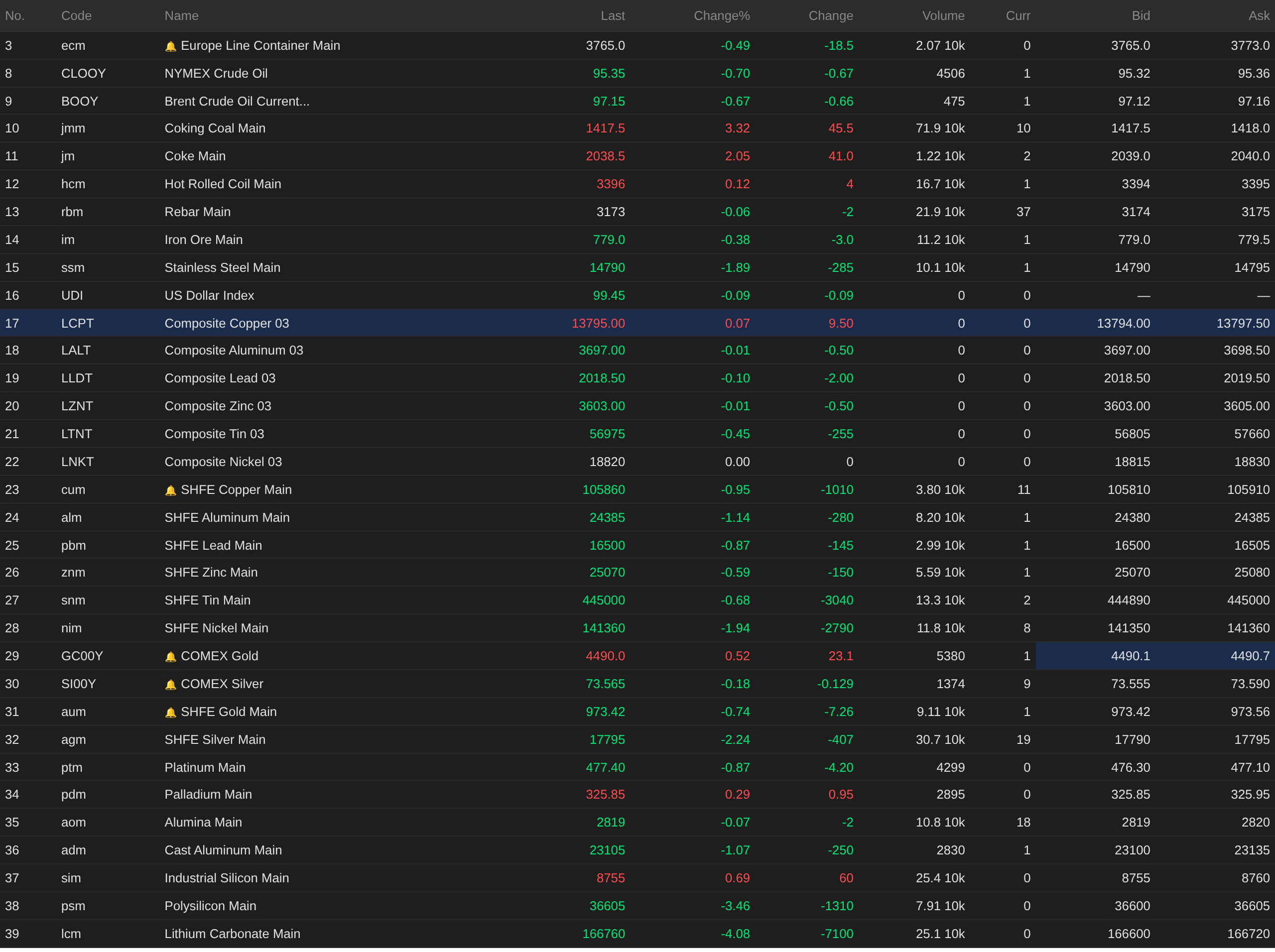

Overnight, base metals fell broadly across both domestic and overseas markets. LME nickel closed flat at $18,820/mt, LME copper rose 0.07%, while all other metals declined. SHFE aluminum and SHFE nickel both fell over 1%, with SHFE aluminum down 1.14% and SHFE nickel down 1.94%. Other metals fell less than 1%. Alumina main contract edged down 0.07%, and casting aluminum main contract fell 1.07%.

Overnight, ferrous metals showed mixed performance. Stainless steel led declines with a 1.89% drop. Iron ore and rebar both edged down, while hot-rolled coil rose 0.12%. For coking coal and coke, coking coal rose 3.32% and coke rose 2.05%.

Precious metals: Overnight, COMEX gold fell 1.27% and COMEX silver fell 3.41%. In China, SHFE gold fell 0.74% and SHFE silver fell 2.24%.

As of 6:45 on June 4, overnight closing prices:

Macro Front

China:

[PBOC Reverse Repo Scale Continuously Reduced to Zero; Policy Tone of "Maintaining Ample Market Liquidity" Remains Unchanged]In early June, the PBOC gradually reduced reverse repo operations. Today it was further reduced to zero. Notably, on August 7, 2024, the PBOC's 7-day reverse repo operation volume was also zero, under a similar backdrop, mainly due to financial institutions' lack of funding demand in this area. Data showed that while DR001 and DR007 declined at the beginning of the month, the 1-year commercial bank (AAA-rated) interbank certificate of deposit yield fell to 1.4275% on June 1, hitting a new low, and remained at this low level on June 2, which may have been a trigger for the PBOC's consecutive reduction of open market reverse repo scale to zero at the beginning of the month. Wang Qing, chief macro analyst at Oriental Jincheng, stated that this was likely mainly due to the absence of sustained significant increases in government bond issuance in the short term, mild credit extension, and declining financing demand from commercial banks toward the PBOC. Based on this trend, outright reverse repos of both tenors in June may continue to shrink. Wang Qing expected that the PBOC would continue to flexibly conduct open market operations based on changes in key market rates such as DR001, DR007, and interbank certificate of deposit yields, guiding market rates to operate steadily around the policy rate through coordinated volume and price adjustments. (Xinhua Finance) (Jin10 Data APP)

US dollar:

Overnight, the US dollar index rose 0.31% to 99.53, posting a three-day winning streak. The US Fed stated in its Beige Book economic report that the US labour market remained stable in recent weeks, but inflation continued to rise across most of the country due to the impact of the Middle East war on energy prices. Among the 12 regional Fed districts, 10 reported overall economic activity growing at a slight to mild pace. "Districts noted that energy costs related to the Middle East conflict were the primary factor driving up inflationary pressures, with spillover effects spreading to shipping, packaging, groceries, and fertilizers. Several districts noted consumer uncertainty and concerns about rising fuel prices impacting household spending." Rising costs had not yet dealt a significant blow to demand, but enterprises expressed concerns about deteriorating sentiment. "The business outlook for the next six months showed little change in expected growth, as persistently high uncertainty and signs of weak consumer spending weighed on market sentiment." In several districts, manufacturing hiring was the strongest, "supported by national defense-related activities and rising data center demand." Most districts continued to describe the labour market as a state of "low hiring, low firing." The report stated: "Hiring remained selective, primarily focused on critical positions or filling vacancies left by natural attrition." Note: The Federal Open Market Committee (FOMC) is about to hold its next monetary policy meeting on June 16-17, which will be the first rate decision since Fed Chairman Kevin Warsh was sworn in in May. (Wallstreetcn)

Dallas Fed President Lorie Logan (2026 FOMC voter) said officials may need to raise interest rates later this year to bring inflation back to the US Fed's 2% target. The US labour market "remains broadly balanced," financial conditions are "on the loose side," but inflation does not appear to be pulling back toward the US Fed's 2% target. "If inflation stays above target for too long, it could become entrenched," and she noted inflation appeared to be heading toward a mid-range level around 2.5% rather than fully returning to 2%. (Wallstreetcn)

According to CME "FedWatch": The probability of the US Fed maintaining rates unchanged through June was 98.4%, with a 1.6% probability of a cumulative 25 basis point interest rate cut. The probability of the US Fed maintaining rates unchanged through July was 90.2%, with an 8.4% probability of a cumulative 25 basis point rate hike, and a 1.4% probability of a cumulative 25 basis point interest rate cut. (Jin10 Data APP)

Macro:

Today will see the release of US May Challenger job cuts, US initial jobless claims for the week ending May 30, US May Global Supply Chain Pressure Index, Eurozone April retail sales MoM, Switzerland May CPI MoM, and Switzerland May seasonally adjusted unemployment rate.

In addition, at 2:00 the US Fed released the Beige Book on economic conditions, and 2026 FOMC voter and Dallas Fed President Logan delivered a speech. At 15:00, the Ministry of Commerce will hold its first regular press conference in June, and China's refined oil products will open a new round of price adjustment window. ECB President Lagarde will deliver a speech, 2027 FOMC voter and Richmond Fed President Barkin will participate in a fireside chat, and Bank of England Governor Bailey will speak at the Investment Association conference.

Crude oil:

Overnight, oil prices rose across both markets, with WTI up 2.6% and Brent up 1.45%, both posting a three-day winning streak, as Middle East tensions escalated again and the market continued to monitor the progress of negotiations between the US and Iran.

The US Energy Information Administration report showed that US crude oil inventory fell for the sixth consecutive week, while exports increased and refinery capacity neared saturation. For the week ending May 29, commercial crude oil inventory excluding strategic reserves decreased by 7.974 million barrels to 434 million barrels, approximately 3% below the five-year average for the same period. Strategic petroleum reserves decreased by 8 million barrels due to continued emergency release, falling to 357.1 million barrels. Gasoline inventory ended a 15-week downtrend, increasing by 3.4 million barrels to 215 million barrels, 5% below the five-year average for the same period. Daily gasoline demand decreased by 662,000 barrels to 8.6 million barrels. (Jin10 Data APP)

Analysts warned that US oil inventory had fallen to a one-year low, and once a sustained disruption occurs at the Strait of Hormuz, the market buffer would be extremely limited. Rabobank energy strategist Florence Schmit stated: Until agreements are reached on Iran's highly enriched uranium issue, the Strait of Hormuz, and the Lebanon situation, the likelihood of a credible peace deal materializing remains low, and uncertainty is the dominant theme in the current market. (Wallstreetcn)

![Metals Fell Broadly, Lithium Carbonate and Palladium Dropped Over 3%, SHFE Nickel, Stainless Steel, Alumina, and SHFE Silver Led Declines [SMM Midday Review]](https://imgqn.smm.cn/usercenter/PeWqW20251217171735.jpg)

![Declining Copper Prices Stimulated Consumption, Converging Price Spread Between Futures Contracts Supported Narrowing of Shanghai Spot Copper Discounts [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)

![Major Players Hold Prices Firm with Active Trading [SMM South China Spot Aluminum Daily Review]](https://imgqn.smm.cn/usercenter/kRRxA20251217171652.jpg)