Noticias de SMM del 4 de junio:

Mercado de metales:

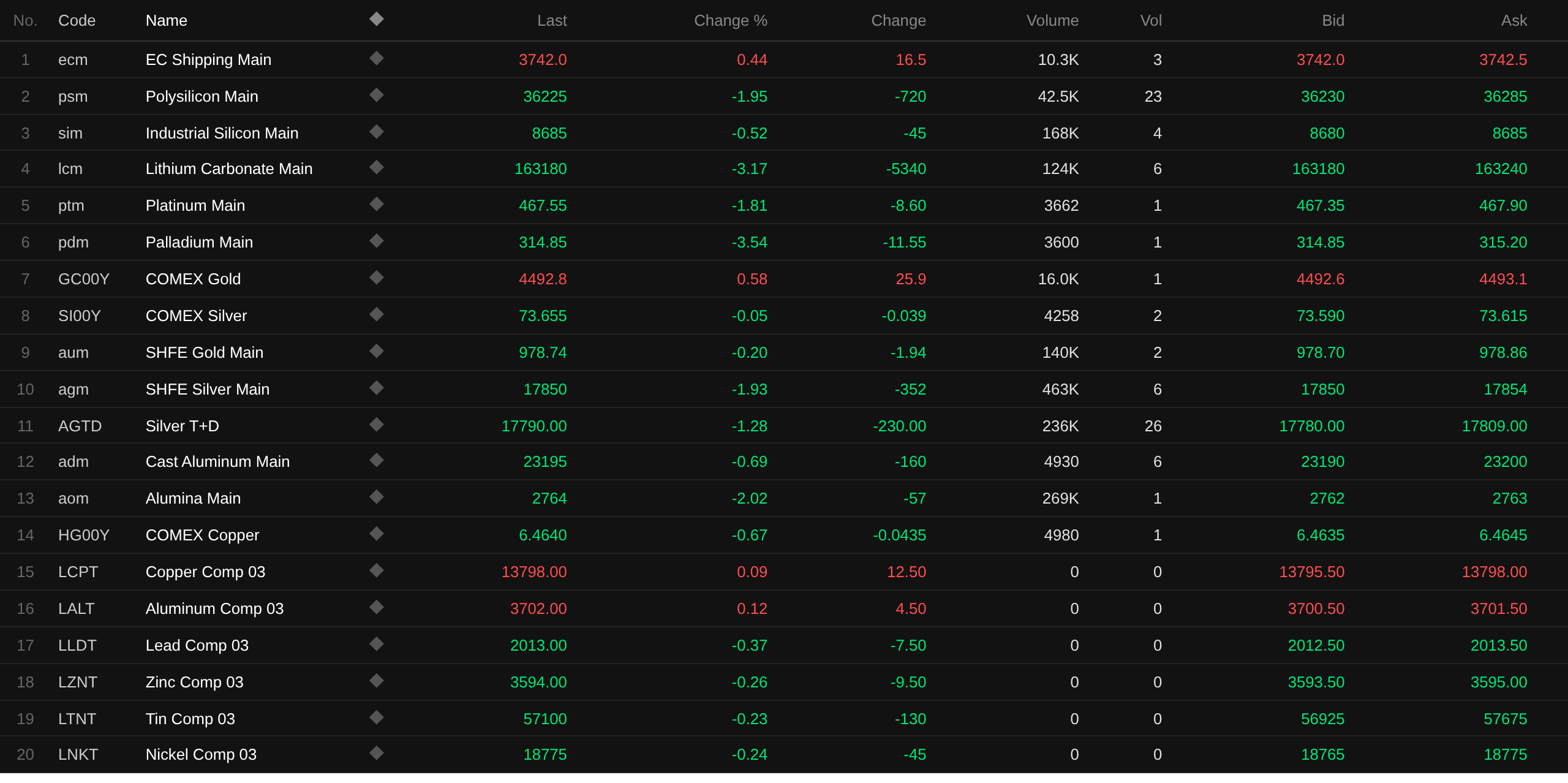

Al cierre del mediodía, los metales base del mercado doméstico cayeron en todos los ámbitos. El cobre SHFE, el aluminio SHFE, el plomo SHFE y el zinc SHFE cayeron más del 1%. El estaño SHFE cayó un 0,86%. El níquel SHFE cayó un 2,55%.

Además, los futuros de aluminio de fundición más negociados cayeron un 0,69%, y los futuros de alúmina más negociados cayeron un 2,02%. Los futuros de carbonato de litio más negociados extendieron la caída de las tres sesiones anteriores, bajando otro 3,17%. Los futuros de silicio metálico más negociados cayeron un 0,52%. Los futuros de polisilicio más negociados cayeron un 1,95%.

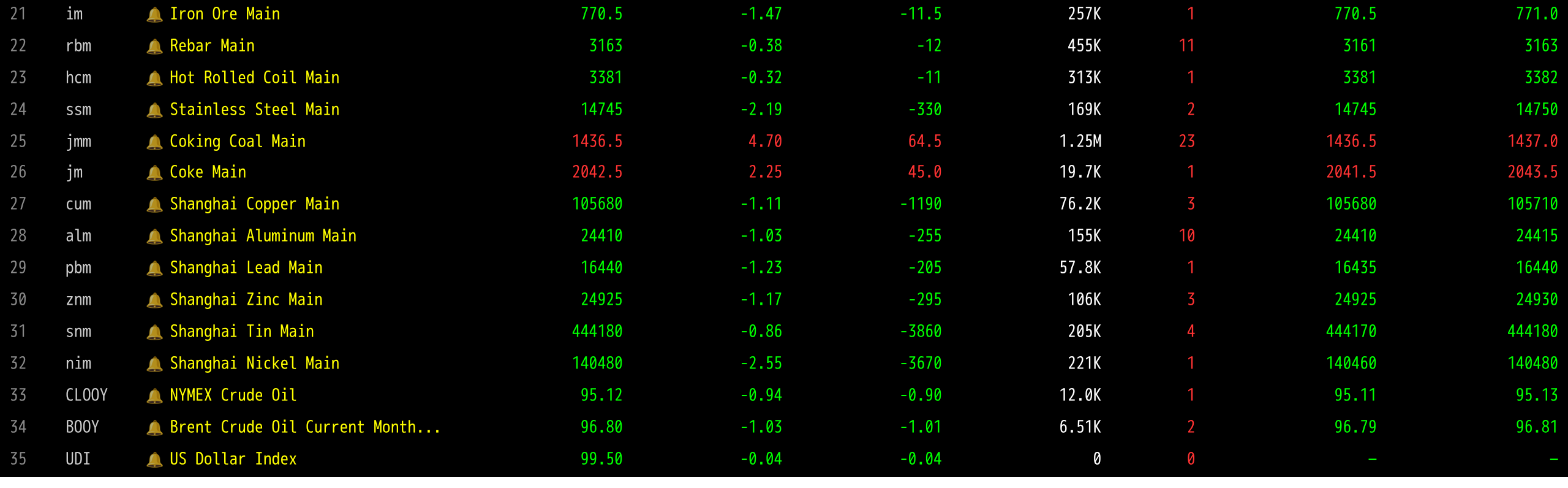

Los metales ferrosos cayeron en su mayoría. El mineral de hierro bajó un 1,47%, las barras de refuerzo cayeron un 0,38%, la bobina laminada en caliente cayó un 0,32% y el acero inoxidable cayó un 2,19%. Carbón de coque y coque: el contrato de carbón de coque más negociado subió un 4,7%, y el contrato de coque más negociado subió un 2,25%.

Metales base del mercado internacional: a las 11:45, los metales LME cayeron en general. El cobre LME cayó un 0,09%, el aluminio LME cayó un 0,12% y el plomo LME cayó un 0,37%. El zinc LME, el estaño LME y el níquel LME cayeron dentro del 0,3%.

Metales preciosos: a las 11:45, el oro COMEX subió un 0,58% y la plata COMEX cayó un 0,05%. Metales preciosos del mercado doméstico: los futuros de oro SHFE más negociados cayeron un 0,2%, y los futuros de plata SHFE más negociados cayeron un 1,93%.

Además, al cierre del mediodía, los futuros de platino más negociados cayeron un 1,81%, y los futuros de paladio más negociados cayeron un 3,54%.

Al cierre del mediodía, el contrato más negociado del índice de flete de contenedores de Europa subió un 0,44% hasta los 3.758 puntos.

A las 11:45 del 4 de junio, cotizaciones de futuros del mediodía para contratos seleccionados:

Mercado spot y fundamentos

Aluminio:El 4 de junio, el aluminio SMM A00 (Foshan) se cotizó a 24.130, con una baja de 190, con un descuento de 190 respecto al contrato del mes en curso, reduciéndose en 60 (unidad: yuan/t). Los futuros dejaron de subir y giraron a la baja hoy, mientras que los precios spot del sur de China resistieron la tendencia y se estabilizaron con sesgo alcista...

Frente macroeconómico

Nacional:

[MIIT: De enero a abril, la producción de valor añadido de la manufactura de información electrónica a escala de China aumentó un 14% interanual]De enero a abril, la producción de valor añadido de la manufactura de información electrónica a escala aumentó un 14% interanual, 8,4 y 1,4 puntos porcentuales por encima de las tasas de crecimiento de la industria general y la manufactura de alta tecnología en el mismo período, respectivamente. En abril, la producción de valor añadido de la manufactura de información electrónica a escala aumentó un 15,6% interanual. Entre los principales productos, la producción de teléfonos móviles alcanzó los 452 millones de unidades, un aumento del 0,3% interanual, de los cuales la producción de smartphones fue de 390 millones de unidades, un aumento del 6,5% interanual; la producción de equipos de microcomputadoras fue de 95,426 millones de unidades, una caída del 10% interanual; la producción de circuitos integrados fue de 176.970 millones de unidades, un aumento del 24,7% interanual. (Weibo del MIIT)

[La carga máxima de energía de State Grid Corporation of China superará los 1.300 millones de kW este verano, un aumento de ~6% interanual] Según State Grid Corporation of China, la carga máxima de energía de este verano en su área de operación se proyectaba que superaría los 1.300 millones de kW, un aumento de aproximadamente el 6% interanual. Para garantizar plenamente la operación segura de la red eléctrica y el suministro fiable de energía, State Grid Corporation of China aceleró la construcción de capacidad de aseguramiento del suministro, continuó mejorando la comercialización de energía basada en el mercado y promovió la utilización eficiente de energía limpia. Actualmente, 168 proyectos clave para el suministro eléctrico de verano estaban en construcción acelerada. (CCTV)

El PBOC anunció que, según la demanda de los operadores primarios en operaciones de mercado abierto, el volumen de la operación de recompra inversa a 7 días del 4 de junio fue cero. Hoy vencieron 101.300 millones de yuanes en recompras inversas.

Dólar estadounidense:

A las 11:45, el índice del dólar estadounidense cayó un 0,04% hasta 99,5. Según el "FedWatch" de CME: la probabilidad de que la Fed de EE. UU. mantenga las tasas sin cambios hasta junio fue del 98,4%, con una probabilidad del 1,6% de un recorte acumulado de 25 pb. La probabilidad de que la Fed de EE. UU. mantenga las tasas sin cambios hasta julio fue del 90,2%, con una probabilidad del 8,4% de un aumento acumulado de 25 pb y una probabilidad del 1,4% de un recorte acumulado de 25 pb.

Logan de la Fed de EE. UU. declaró que los funcionarios de la Fed podrían necesitar subir las tasas de interés más adelante este año para reducir la inflación al objetivo del 2%. Señaló que el mercado laboral estadounidense estaba "ampliamente en equilibrio", la inversión en inteligencia artificial estaba en auge y las condiciones financieras seguían siendo "acomodaticias". Sin embargo, añadió que la trayectoria actual de la inflación no parecía estar retrocediendo hacia el objetivo del 2% de la Fed. "Estas condiciones sugieren que la política monetaria actual no está restringiendo la economía", "Me preocupa cada vez más que lograr una restauración completa de la estabilidad de precios, equilibrando adecuadamente ambos lados del mandato dual de la Fed, pueda requerir subir las tasas de interés más adelante este año".

El Libro Beige de la Fed señaló que, en general, los precios subieron a un ritmo moderado a fuerte, y la mayoría de los distritos reportaron tasas de inflación más altas que en el informe anterior. Los distritos citaron los costos energéticos relacionados con el conflicto en Oriente Medio como un factor principal de las presiones inflacionarias, con impactos que se extendieron al transporte marítimo, embalaje, alimentos y fertilizantes. Los costos no laborales continuaron subiendo más rápido que los precios de venta, generando preocupaciones más amplias sobre la compresión de márgenes. La capacidad de trasladar costos más altos varió entre industrias, particularmente entre las empresas orientadas al consumidor. Algunas regiones señalaron que las empresas en múltiples áreas habían adoptado estrategias para hacer frente a la inflación, incluyendo optimización de la cadena de suministro, ajustes de productos, reducción de la oferta y absorción temporal de costos más altos para mantener la demanda de los clientes. (Jin10 Data APP)

Datos:

Los datos a publicarse hoy incluían los despidos empresariales Challenger de mayo en EE. UU., las solicitudes iniciales de subsidio por desempleo en EE. UU. para la semana que terminó el 30 de mayo, el Índice de Presión de la Cadena de Suministro Global de mayo en EE. UU., las ventas minoristas de abril de la eurozona (mensual), el IPC mensual de mayo de Suiza y la tasa de desempleo desestacionalizada de mayo de Suiza.

Además, a las 2:00 la Fed de EE. UU. publicó el Libro Beige sobre las condiciones económicas, y la votante del FOMC 2026 y presidenta de la Fed de Dallas, Logan, pronunció un discurso. A las 15:00, el Ministerio de Comercio celebró la primera conferencia de prensa regular de junio, y los productos refinados de petróleo de China entraron en una nueva ventana de ajuste de precios. La presidenta del BCE, Lagarde, pronunció un discurso, el votante del FOMC 2027 y presidente de la Fed de Richmond, Barkin, participó en una charla informal, y el gobernador del Banco de Inglaterra, Bailey, habló en la conferencia de la Investment Association.

Petróleo crudo:

A las 11:45, los precios del petróleo en ambos mercados cayeron, con el WTI bajando un 0,94% y el Brent un 1,03%. Según CCTV News, el 3 de junio hora local, el presidente de EE. UU., Trump, declaró que las negociaciones con Irán estaban progresando muy bien y que una nueva ronda de conversaciones podría celebrarse este fin de semana. Una vez firmado el acuerdo, el Estrecho de Ormuz se reabrirá inmediatamente. (Jin10 Data APP) Las expectativas de un fin de los conflictos en Oriente Medio presionaron los precios del petróleo.

El analista de Investinglive, Eamonn Sheridan, declaró que los informes indicaban que Israel y Líbano habían alcanzado un acuerdo marco de alto el fuego bajo la guía de EE. UU., con ambas partes programadas para reanudar las conversaciones completas durante la semana del 22 de junio, condicionado a la retirada completa de Hezbolá del sur del Líbano. La prima de riesgo geopolítico en el mercado petrolero asimilará este titular y lo tratará en gran medida como un factor ya descontado. (Jin10 Data APP)

El conflicto entre EE. UU. e Irán está empujando al mercado petrolero global hacia un punto de inflexión. El inventario de petróleo crudo y productos derivados de EE. UU. ha caído a su nivel más bajo en más de dos décadas, mientras que las exportaciones de petróleo crudo de EE. UU. alcanzaron un récord en mayo, agotando rápidamente las reservas nacionales. Los analistas advirtieron que si el Estrecho de Ormuz permanece cerrado, los precios del petróleo podrían dispararse significativamente en semanas. Según datos publicados por la Administración de Información Energética de EE. UU. (EIA) el miércoles, para la semana que terminó el 29 de mayo, el inventario total de petróleo crudo y productos derivados de EE. UU. disminuyó en 10,6 millones de barriles respecto a la semana anterior hasta 1.570 millones de barriles, el nivel más bajo desde 2004. El inventario comercial de petróleo crudo (excluyendo la Reserva Estratégica de Petróleo) cayó en 8 millones de barriles en una sola semana hasta 433,7 millones de barriles, marcando la sexta caída semanal consecutiva, superando con creces las expectativas previas de los analistas de 3,3 millones de barriles. (Wall Street Journal)

Panorama del mercado spot:

►

►

►

►

►

►

►

►

►

►

![Los metales cayeron en general, el carbonato de litio bajó más de un 5%, el estaño de la Bolsa de Metales de Londres (LME), el níquel de la Bolsa de Futuros de Shanghái (SHFE), el cobre de la LME y el polisilicio lideraron las caídas; la plata de la SHFE cayó por sexto día consecutivo [Comentario de mediodía de SMM]](https://imgqn.smm.cn/usercenter/VCNvX20251217171735.jpeg)

![La presión vendedora de fin de mes se alivia, sube el centro de las primas del cobre al contado en Shanghái [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/AhHUS20251217171713.jpg)

![Los futuros del aluminio caen por días consecutivos, el ambiente de negociación se mantiene flojo [Comentario del mediodía sobre aluminio al contado de SMM]](https://imgqn.smm.cn/usercenter/XLWyP20251217171654.jpg)